First time homebuyer programs in PA (Pennsylvania) exist for one reason: to make homeownership possible when upfront costs feel out of reach. Across the state, and at the county and city levels, there are programs designed to help with down payments, closing costs, and early affordability through grants, forgivable loans, and low-interest assistance for first-time homebuyers.

These aren’t just handouts or “free money.” They’re smart, structured tools meant to support buyers who are serious about owning a home and staying financially stable long term. If you know how to navigate these options, they can be the difference between waiting years to buy and getting the keys to your first home much sooner. So, let’s explore them!

Table of Contents

Statewide Assistance through the Pennsylvania Housing Finance Agency (PHFA)

The Pennsylvania Housing Finance Agency (PHFA) is the engine behind most statewide homeownership programs. PHFA partners with approved lenders across Pennsylvania to offer 30-year fixed-rate mortgages with competitive pricing and lower fees than many conventional options.

These are the foundation of first-time homebuyer programs in PA. Instead of navigating dozens of disconnected offers, buyers can work through a participating lender to access PHFA-backed loans designed to prioritize stability, affordability, and long-term success, not risky shortcuts.

Primary PHFA Loan Programs

PHFA offers several core mortgage options that first-time buyers in Pennsylvania can use to make homeownership more affordable. Each program is designed to solve a specific barrier, whether that’s down payment costs, mortgage insurance, or property condition.

1. Keystone Home Loan

This is PHFA’s flagship program for first-time homebuyers, discharged veterans, and buyers purchasing in federally designated “target areas.” It comes with competitive fixed rates but does require borrowers to meet household income and purchase price limits, which vary by county.

2. HFA Preferred (Lo MI)

Private Mortgage Insurance (PMI) is one of the biggest hurdles for buyers with small down payments. This program offers reduced-cost mortgage insurance for eligible borrowers who meet income limits and contribute at least $1,000 of their own funds toward the purchase.

3. Keystone Government Loan (K-Gov)

K-Gov supports FHA, VA, and USDA loans and offers more flexibility than many other PHFA options. There are no income or purchase price limits, but borrowers with credit scores of 680 or below must complete an approved homebuyer education course.

4. Keystone Flex

This program is built for buyers who need flexibility. In addition to standard purchases, it allows a Purchase and Improvement option, letting borrowers roll up to $30,000 in necessary repairs or renovations into one mortgage.

Together, these PHFA programs form a powerful toolkit for first-time buyers in Pennsylvania, especially those who need help bridging the gap between affordability and ownership.

PHFA Down Payment and Closing Cost Assistance

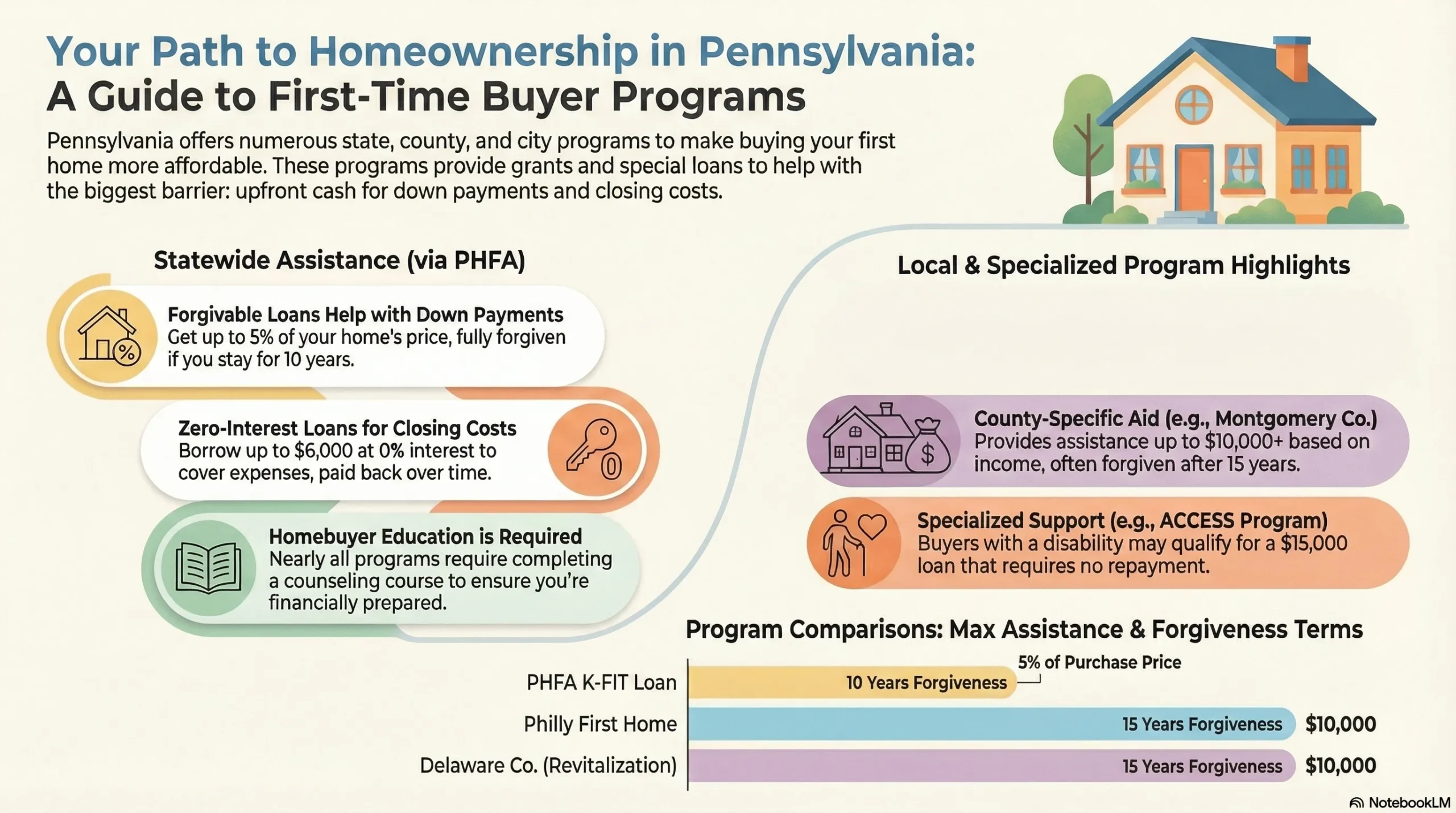

To make these affordable mortgages even more accessible, PHFA layers in additional assistance, often forgivabl,e that directly tackles the biggest challenge for first-time buyers: upfront cash. This is where many first time homebuyer programs in PA truly make a difference.

1. Keystone Forgivable in Ten Years (K-FIT)

This is one of PHFA’s most powerful tools. K-FIT provides a second mortgage equal to up to 5% of the purchase price or appraised value (whichever is lower), with no maximum dollar cap. The loan is forgiven gradually at 10% per year, meaning if you stay in the home for ten years, the entire balance is wiped out.

2. Keystone Advantage Assistance Loan

This option offers a second mortgage of up to 4% of the purchase price or $6,000, whichever is less. It carries zero interest, but unlike K-FIT, it must be repaid over a ten-year period through manageable monthly payments.

3. PHFA Grant

Buyers using the HFA Preferred (Lo MI) loan may qualify for a $500 grant that does not need to be repaid. The funds are applied directly toward closing costs, providing a small but helpful boost at the settlement table.

4. HOMEstead Program

The HOMEstead program offers between $1,000 and $10,000 in assistance as a no-interest second mortgage. This loan is fully forgiven after five years. Availability is limited by county, and properties built before 1978 are often excluded due to lead-based paint regulations.

When combined with PHFA’s primary loan programs, these assistance options can dramatically reduce the cash you need upfront and bring homeownership within reach much sooner than many buyers expect.

City and County-Specific Programs in Pennsylvania

Beyond statewide efforts, many local municipalities offer robust first time homebuyer programs tailored to their specific economic landscapes and revitalization goals.

Philadelphia: Philly First Home Program

Administered by the City of Philadelphia, this powerful program offers a homebuyer assistance grant of up to $10,000 or 6% of the purchase price (whichever is less).

-

Eligibility: Must be a first-time buyer (or not have owned a home in three years) and purchase a single-family home or duplex in Philadelphia. Condominiums are ineligible.

-

Terms: The grant is structured as an interest-free loan that is fully forgiven after 15 years. If the owner sells or refinances before the 15th anniversary, the grant must be repaid on a prorated basis.

-

Education: A City-funded, 8-hour housing counseling program must be completed before signing an agreement of sale.

Montgomery County: First Time Homebuyers Program

Montgomery County provides tiered assistance for low, moderate, and median-income households.

-

Funding: Base assistance up to 10% of the estimated affordable sales price, not to exceed $10,000. Low-income households (below 80% or 60% of Area Median Income) may qualify for additional funds, potentially totaling up to $40,000.

-

Requirements: Applicants must have at least $3,000 of their own liquid assets and reside or work full-time in the county.

-

Repayment: The zero-interest loan must be repaid only if the home is sold, transferred, or no longer used as a primary residence within 15 years.

Delaware County: Homeownership First Program

This program assists buyers with up to $10,000 for down payments and closing costs, with favorable terms in target neighborhoods.

-

Revitalization Areas: In specific designated “Revitalization Areas” (such as Darby or Lansdowne), the loan is 100% forgiven if the homeowner stays for at least five years.

-

General Terms: For homes outside these areas, the loan is interest-free but must be repaid in full upon sale or transfer.

-

Upper Darby Township: Upper Darby is exempt from this program and instead offers its own local homebuyer assistance, providing up to $20,000 to qualified buyers. This program is federally funded, so strict guidelines apply. Buyers must contribute a minimum of $1,000 toward the purchase. The total purchase price (including closing costs) cannot exceed $304,000 for existing homes or $365,000 for new construction.

Western Pennsylvania: Pittsburgh and Beyond

-

Pittsburgh Urban Redevelopment Authority (URA): Offers substantial assistance of up to $90,000 for income-eligible first-time buyers through its OwnPGH Homeownership program, one of the most generous local first time homebuyer programs in PA.

-

NeighborWorks LIFT Program: This program focuses on several western counties (including Allegheny, Erie, and Washington). It offers a $15,000 grant for first-time homebuyers. Funds can be used for down payment, closing costs, interest rate buy-downs, or paying off up to $5,000 in eligible installment debt. Buyers also receive free post-purchase support, including a one-year home warranty, a free will, housing counseling, and up to $1,500 in emergency reserves. To qualify, household income must be $71,920 or less, buyers must work with an approved NeighborhoodLIFT lender, and complete 8 hours of homebuyer education through AHCOPA or RiseUp.

Specialized Programs for Diverse Needs

There are also first time homebuyer programs in PA designed for specific demographics or professional groups, ensuring broader access to homeownership.

1. ACCESS Downpayment and Closing Cost Assistance

Designed for buyers living with a disability or residing with someone who has a disability. It provides a no-interest loan of up to $15,000 that does not require repayment as long as the home remains the primary residence.

2. Employer Assisted Housing (EAH)

This innovative initiative partners with specific employers to match funds provided by the employer to help employees buy homes near their workplace. PHFA can match employer contributions up to $8,000.

A HUD-sponsored program for teachers, firefighters, law enforcement, and EMTs. It offers a 50% discount on the list price of HUD-owned homes in certain revitalization areas if the buyer commits to living there for 36 months.

First Front Door (FFD) offers down payment and closing cost assistance to eligible first-time homebuyers through participating FHLBank Pittsburgh lenders. Buyers who contribute at least $1,500 can receive up to $15,000 in grant assistance. The First Front Door Keys to Equity program expands access for minority and first-generation first-time buyers. With a minimum $1,000 buyer contribution, eligible households can receive up to $20,000 in grant funds.

Mandatory Requirements and Preparation

Most first-time homebuyer programs in PA aren’t just about qualifying on paper. They’re designed to set you up for long-term success, which means preparation is required, not optional.

1. Homebuyer Education:

Nearly all major programs, especially PHFA options and Philly First Home, require you to complete an approved homebuyer counseling course. These classes walk you through budgeting, credit basics, the mortgage process, and what it really takes to maintain a home after closing. It’s not busywork; it’s practical, useful information.

2. Credit Score Requirements:

While there are programs for different credit profiles, many PHFA loans look for a minimum FICO score of around 660–680. If your score is below that range, improving it ahead of time can dramatically expand your options and lower your costs.

3. Income and Price Limits:

Because these programs are publicly funded, they come with income caps tied to Area Median Income (AMI) and limits on how much the home can cost. Staying within those limits is non-negotiable.

4. Cash and Asset Rules:

Some programs require you to bring a small amount of your own money to the table, often a few thousand dollars, while also placing a cap on total liquid assets. The goal is to make sure assistance goes to buyers who truly need the help, not those sitting on large cash reserves.

These programs reward buyers who plan ahead, stay organized, and take the process seriously. Early preparation for buying a home in Pennsylvania is the key to success.

Conclusion

First time homebuyer programs in PA are often the missing link between renting and owning. Think of them as a support system that helps you gain balance and confidence before taking on full homeownership on your own. From PHFA’s forgivable assistance to city-level grants like those offered in Philadelphia, these programs do more than help you buy a house; they help you stay in it long term.

Ready to take the first step? Sign up today and start preparing for homeownership with confidence.

0 Comments