Getting a mortgage after a bankruptcy or foreclosure might feel out of reach, but it’s not. One major financial setback does not permanently cancel your homeownership goals. The reality is far more practical: with the right timing, proper documentation, and a smart rebuilding strategy, you can qualify again.

In this guide, I’ll walk you through:

- What bankruptcy and foreclosure actually mean from a lender’s perspective

- How long do you typically need to wait before applying again

- Which loan programs may still be available to you

- What documentation will underwriters expect

- How to rebuild in a way that strengthens your next application

Let’s start by getting clear on the terminology.

Table of Contents

Understanding The Different Financial Events That Affect Homeownership

When we talk about how to get a mortgage after bankruptcy, we’re not just discussing bankruptcy alone. Several major financial events can impact your ability to buy a home again. Each has different guidelines and waiting periods.

Understanding the differences helps you know where you stand.

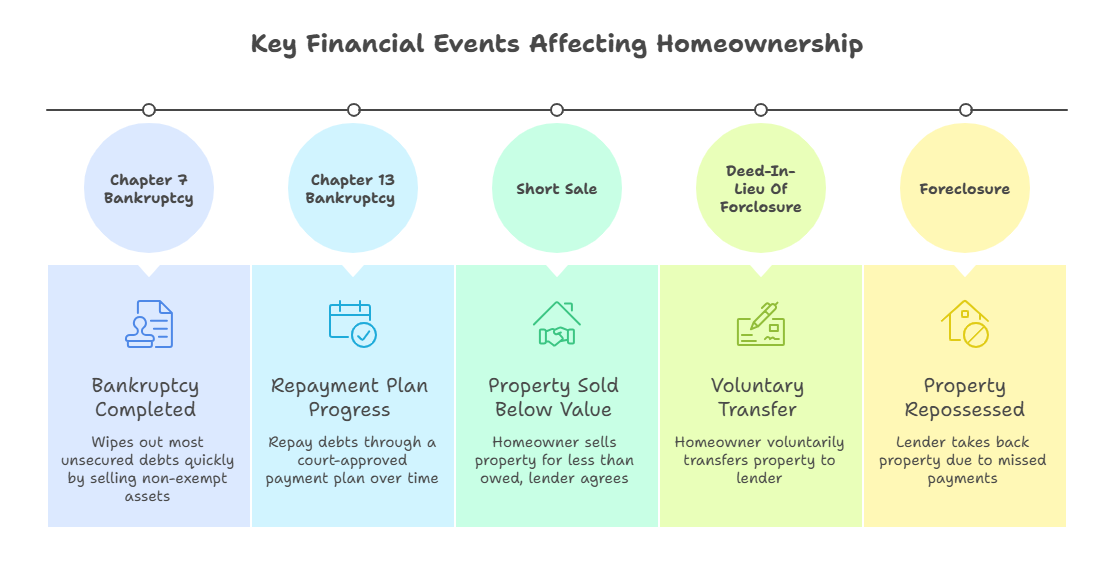

Chapter 7 Bankruptcy (Liquidation Bankruptcy)

Chapter 7 bankruptcy eliminates most unsecured debts, such as credit cards and medical bills. Some assets may be sold to repay creditors, and the process typically lasts a few months. Once discharged, you are no longer legally responsible for those eligible debts.

For mortgage purposes, lenders focus heavily on the discharge date, not the filing date. The discharge marks the point where you officially completed the bankruptcy process and began rebuilding.

Many borrowers who want to get a mortgage after bankruptcy start fresh financially under Chapter 7, but must wait a specific period before qualifying again.

Chapter 13 Bankruptcy (Wage Earner’s Plan)

Chapter 13 is different. Instead of wiping out debts immediately, you enter a court-approved repayment plan lasting 3 to 5 years. You repay part or all of your debt over time while keeping your assets.

In many cases, borrowers can qualify for a mortgage before completing the full repayment plan, often after 12 months of consistent, on-time payments with court approval.

Chapter 13 is often viewed more favorably than Chapter 7 because it shows structured repayment and financial discipline.

Foreclosure

Foreclosure happens when a lender takes back a property after missed mortgage payments. The home is repossessed and sold to recover losses.

Foreclosure is considered a major derogatory credit event. However, it does not permanently block your ability to buy again. Waiting periods apply, but many borrowers successfully get a mortgage after bankruptcy or foreclosure once they reestablish stability.

Short Sale

A short sale occurs when a homeowner sells the property for less than what is owed, and the lender agrees to accept that amount to avoid foreclosure.

Short sales are typically viewed more favorably than foreclosures. The waiting period is often shorter, especially if payments were current before the sale.

Deed-In-Lieu Of Foreclosure

A deed-in-lieu allows a homeowner to voluntarily transfer ownership back to the lender instead of going through foreclosure. It is generally less damaging than foreclosure, but is still considered a significant credit event.

Can You Get A Mortgage After Bankruptcy Or Foreclosure?

Yes, you can get a mortgage after a bankruptcy, foreclosure, short sale, or deed-in-lieu, but not immediately. Every major loan program has a required waiting period before you’re eligible again.

When a significant financial event shows up on your record, lenders see it as evidence of past hardship. Because a mortgage is a long-term commitment, they need time to confirm that your situation has stabilized. That waiting period isn’t a punishment; it’s an opportunity to rebuild and prove consistency.

During that time, lenders want to see:

- Stable, verifiable income

- On-time payment history

- Manageable debt levels

- No new major credit issues

- Signs of savings and financial discipline

Here’s the most important mindset shift: you’re not permanently denied, you’re temporarily paused.

Once the required timeframe passes, underwriting shifts its focus to who you are financially today. If you’ve rebuilt the right way, approval becomes very realistic.

Now, let’s break down the typical waiting periods and what you should expect moving forward.

Waiting Periods: How Long Until You Can Apply Again

A. Bankruptcy Waiting Periods

The waiting period you’ll face depends on the type of bankruptcy and the loan program you plan to use.

| Loan Type | Chapter 7 Bankruptcy | Chapter 13 Bankruptcy |

| FHA Loan | Usually, 2 years from the discharge date. | You may qualify with 12 months of on-time payments into your plan, plus court approval. |

| Fannie Mae | Typically, 4 years from the discharge date. | Often, 2 years from the discharge date if discharged, or 4 years if dismissed. |

| VA Loan | Often, 2 years from the discharge date. | May qualify after 12 months of plan payments from the filing date with court/trustee approval. |

Important: The clock usually starts at the discharge date, not the filing date.

Extenuating circumstances, such as documented job loss or medical emergencies, may shorten waiting periods in some cases.

B. Foreclosure, Short Sale, Deed-in-Lieu Waiting Periods

| Loan Type | Foreclosure Waiting Period | Short Sale / Deed-in-Lieu Waiting Period |

| FHA | About 3 years from the date the foreclosure was completed. | Also ~3 years, though if you were current on payments before sale the wait may be less. |

| Fanni Mae | Normally 7 years, but may be reduced to 3–4 years with extenuating circumstances. | Often 4 years from short sale date if no foreclosure. |

| VA | Often as short as 2 years after foreclosure for qualified borrowers. | Often 2 years from the completion date |

Key point: Staying current on your housing payments, repairing credit, stabilizing finances, and documenting hardship help shorten the timeline.

Documents You’ll Need to Prepare

If you want to successfully get a mortgage after bankruptcy, documentation is critical. Lenders want proof of stability and improvement.

A. Documentation for Bankruptcy

You’ll generally need:

- Copy of the bankruptcy discharge order (Chapter 7) or payment plan documents (Chapter 13)

- Letter of explanation: stating what caused the bankruptcy and how your financial situation has improved

- Documentation of re-established credit (e.g., secured credit cards, timely payments)

- Up-to-date credit report showing no new major delinquency

- Employment verification and income documentation showing stability

- Recent pay stubs and tax returns

- Bank statements showing good savings or assets

B. Documentation for Foreclosure / Short Sale

Prepare to show:

- Public record documenting completion date of foreclosure or deed-in-lieu (or HUD-1 settlement for short sale)

- Explanation of what happened (job loss, illness, market decline, etc.)

- Proof that you have been current on any post-event housing or rental payments

- Evidence of savings/reserves, consistent bank statement activity

- Credit report showing no major derogatory items since event

Strategies to Rebuild and Improve Your Chances

If your goal is to get a mortgage after bankruptcy or foreclosure, rebuilding is not about rushing; it’s about creating stability that lenders can clearly see. Mortgage approval after a major credit event is less about perfection and more about consistency.

Here’s what truly strengthens your chances:

1. Stabilize Your Income

Lenders want to see predictable, documented income. In most cases, they look for a two-year history of consistent employment, preferably in the same line of work.

If you changed careers after your bankruptcy or foreclosure, that’s okay, but stability matters. Avoid frequent job changes right before applying. If you are self-employed, make sure your tax returns reflect steady income and proper documentation.

Income stability shows lenders the hardship was temporary, not ongoing.

2. Rebuild Credit The Right Way

To get a mortgage after bankruptcy, you don’t need a perfect credit score; you need a clean recent history.

Focus on:

- Making every payment on time

- Keeping credit card balances low (ideally under 30% utilization, lower if possible)

- Avoiding new collections or late payments

- Not opening unnecessary new accounts

Secured credit cards or small installment loans can help rebuild, but only if managed responsibly. Slow, steady improvement is more powerful than quick, risky changes.

If you need structured guidance, Credit Repair for Homebuyers focuses specifically on preparing credit for mortgage approval, not just raising a score.

3. Build Savings And Reserves

Savings demonstrate responsibility and preparedness. Even modest reserves can make a difference in how your file is viewed.

Try to build:

- An emergency fund

- Down payment savings

- Closing cost reserves

- 1–3 months of projected mortgage payments (if possible)

Strong bank statements with consistent deposits and responsible spending patterns show lenders you are ready for homeownership again.

4. Keep Your Debt-To-Income Ratio Under Control

After bankruptcy or foreclosure, controlling debt is necessary. Avoid taking on new car loans, personal loans, or high credit card balances before applying.

Lenders calculate your debt-to-income (DTI) ratio to determine affordability. Lowering debt improves your approval odds significantly.

Even small improvements like paying down balances or eliminating small debts can strengthen your file.

5. Document The Hardship Clearly

If your bankruptcy or foreclosure was caused by circumstances beyond your control, such as job loss, medical issues, divorce, or economic downturn, document it clearly.

A simple, factual letter of explanation should include:

- What happened

- When it happened

- Why it was outside your control

- What has changed since then

Avoid emotional storytelling. Focus on resolution and improvement. Lenders want reassurance that the issue was situational and is unlikely to repeat.

6. Stay Completely Current Moving Forward

The most important rule if you want to get a mortgage after bankruptcy is this:

Do not create new negative activity.

Even one late payment after a bankruptcy or foreclosure can reset progress and delay your timeline. Stay current on rent, utilities, credit cards, and loans.

Recent behavior carries more weight than older mistakes.

7. Work With The Right Guidance

Not all lenders interpret guidelines the same way. Some are more experienced with post-bankruptcy borrowers than others.

Before applying, consider going through a structured preparation process like Mortgage Readiness. Instead of applying and hoping for approval, you prepare strategically before submitting an application.

Preparation reduces denials. Denials create setbacks. Planning avoids both.

Final Takeaway

Bankruptcy and foreclosure are setbacks, not permanent endings. The waiting period is temporary. What matters most is what you do after the event.

When you combine:

- Stable income

- Clean payment history

- Controlled debt

- Proper documentation

- Strategic preparation

You dramatically improve your chances of approval.

If you’re serious about getting back into the housing market, don’t guess your way through the process.

Sign up today and take the first confident step toward buying again.

0 Comments