Next steps after mortgage pre-approval in PA are just as important as getting approved in the first place, and this is where many homebuyers unknowingly make mistakes.

Getting pre-approved feels like a huge win (and it is), but pre-approval is not the finish line. You still need to stay mortgage-ready until the day you close. What does that actually mean?

Let’s walk through it step by step so you know exactly what to do and what not to do after pre-approval in Pennsylvania.

Table of Contents

Phase 1: Assembling Your Professional Team

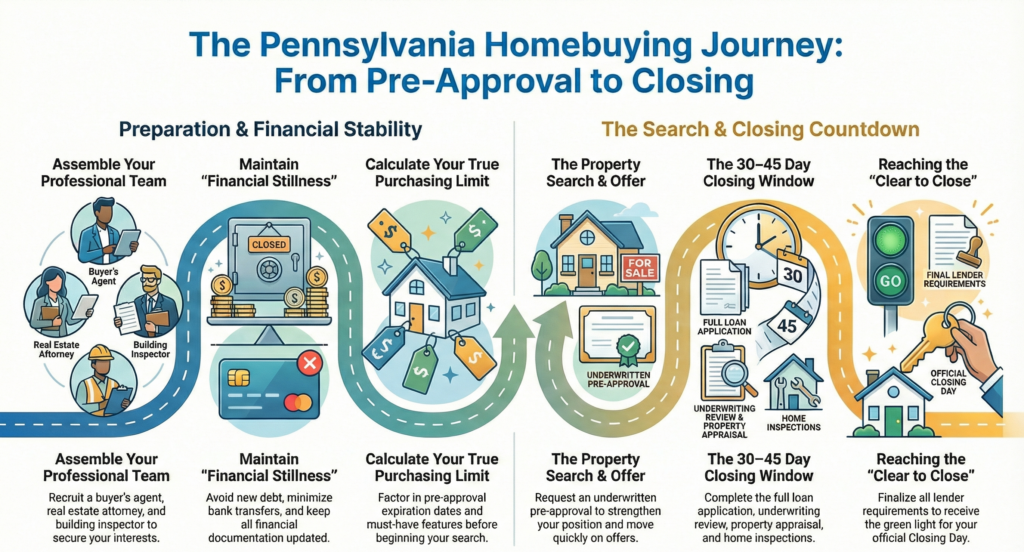

Before you start touring homes, the next steps after mortgage pre-approval in PA involve putting the right team in place. This allows you to move quickly and competitively when the right property appears.

Pick a Real Estate Agent (Buyer’s Agent)

Don’t wait to hire a buyer’s agent. A strong agent makes the entire process smoother, from finding homes to getting under contract and closing on time.

Your agent should:

- Set up MLS searches based on PA-specific criteria (single-family vs. condo, school districts, taxes)

- Filter by your approved price range and comfort level

- Send daily alerts for new listings and price reductions

In competitive Pennsylvania markets, speed matters.

Consider a Buyer’s Advocate

If you’re short on time or struggling to find inventory, a buyer’s advocate can help locate off-market or pre-market properties-homes that sell before ever hitting Zillow or Realtor.com.

They may:

- Call listing agents directly

- Network with local agents

- Negotiate terms on your behalf

This can be a major advantage in tight PA housing markets.

Secure a Conveyancer or Real Estate Attorney

In Pennsylvania, having a real estate attorney or conveyancer ready can be helpful. They review the Agreement of Sale before you sign, making sure the contract protects you.

They look for:

- Unfavorable clauses

- Missing contingencies

- Financing or inspection language that benefits the seller

This step helps prevent surprises later.

Find a Building & Pest Inspector

Line up a licensed inspector early so you’re not scrambling once your offer is accepted.

Even with new construction in PA, inspections matter. Issues like:

- Structural defects

- Moisture intrusion

- Termite damage

are often not covered by insurance, and quality can vary widely.

Get Insurance Quotes Ready

Home insurance can vary significantly, even within the same neighborhood.

Insurance costs can change based on:

- Property age

- Roof condition

- Flood zones

- Detached structures

Example: In some regions, two houses at the same price can have annual insurance costs ranging from $1,500 to $10,000 depending on age, flood zones, or features like a pool or old roof. Having 1–2 insurers ready speeds up underwriting.

Phase 2: Defining Your Search & Financial Limits

Your pre-approval shows the maximum loan amount, not necessarily what you should spend.

Calculate Your True Purchasing Limit

Work with your lender or Mortgage Ready Specialist to determine:

- Purchase price

- Down payment

- Closing costs

- Property taxes

- HOA fees (if applicable)

Your true buying power is what fits comfortably into your life, not just what the bank allows.

Understand Your Pre-Approval Expiry

Most pre-approvals in PA last 60–90 days.

You should aim to:

- Go under contract 2–3 weeks before expiration

- Allow time for appraisal and final underwriting

Letting a pre-approval expire can mean re-verification of income, credit, and assets.

Narrow Down Your Must-Haves

To avoid burnout, define your non-negotiables:

- Target neighborhoods or school districts

- Minimum bedrooms/bathrooms

- Yard size

- Commute time

In Pennsylvania, school districts and property taxes often drive decisions, having clarity saves time.

Phase 3: Maintaining Financial Stillness

One of the most overlooked next steps after mortgage pre-approval in PA is doing nothing financially.

Lenders expect your profile to remain exactly the same as when you were approved.

No New Debt

Do not:

- Open new credit cards

- Finance furniture

- Take out personal or auto loans

Even “0% for 12 months” offers can derail approval.

Minimize Transfers

Avoid moving money between accounts. Each transfer creates documentation requests that can delay underwriting.

Keep Documentation Updated

Have a digital folder ready with:

- Most recent two months of bank statements

- Recent pay stubs

- Two years of tax returns

Lenders often re-request documents before closing.

Disclose Changes Immediately

If anything changes, tell your lender right away, including:

- Job changes or raises

- Large withdrawals

- Medical or emergency expenses

Surprises late in the process cause delays or worse.

Phase 4: The Property Search & Offer Process

Stay in Frequent Contact with Your Lender

Check in weekly while house hunting.

When you find a property, ask your lender to run the numbers for that specific address.

Example:

A $300,000 condo with a $700 HOA may be harder to qualify for than a $300,000 single-family home in PA.

Request an Underwritten Pre-Approval

This means an actual underwriter has reviewed your file, not just automated systems.

It:

- Strengthens your offer

- Shows sellers your financing is solid

- Can win bids in competitive markets

Be Ready to Move Quickly

In desirable Pennsylvania neighborhoods, homes move fast. Being prepared helps you act with confidence, not pressure.

Phase 5: From Accepted Offer to Closing (30–45 Days)

Full Loan Application

Once under contract, you finalize:

- Loan type (Conventional, FHA, VA, etc.)

- Property-specific details

Underwriting Review

The underwriter evaluates the Three C’s:

- Credit – payment history

- Capacity – debt-to-income ratio

- Collateral – the property

Appraisal & Inspection

The lender orders an appraisal to confirm the value.

If the appraisal comes in low:

- Renegotiate the price

- Increase your down payment

- Reassess options

Clear to Close

Once conditions are satisfied, you receive:

- A Closing Disclosure (3 days prior)

- Final numbers to review

Closing Day

You’ll attend a 1–2 hour signing, pay closing costs, and receive the keys to your Pennsylvania home.

Final Thoughts

Getting pre-approved is a big step, but the next steps after mortgage pre-approval in PA are what determine whether your home purchase moves forward smoothly.

Staying mortgage-ready isn’t about doing more; it’s about staying consistent, informed, and prepared through the entire process. Most issues after pre-approval come from small changes that could have been avoided with the right guidance.

Explore more: Pennsylvania Mortgage Ready Program

Get guidance on what mortgage readiness looks like for you and what steps may come next. Sign up Today!

0 Comments