If you’re buying a home in Pennsylvania, an FHA loan is often one of the easiest ways to get started, especially if your credit, savings, or income aren’t perfect yet. These loans are popular with first-time buyers because they allow lower credit scores and smaller down payments than many conventional options.

In this guide, we unpack FHA loan requirements in PA so you understand not just the numbers, but how lenders evaluate your mortgage readiness and what you can do to improve your chances of approval.

Table of Contents

What Is an FHA Loan and Why Does It Matter in Pennsylvania

An FHA loan is a mortgage insured by the Federal Housing Administration (FHA). The FHA doesn’t lend money directly; instead, it guarantees loans made by approved lenders, making them more willing to work with borrowers who might not meet stricter conventional requirements.

This guarantee can make FHA loan requirements in PA more flexible in key areas like:

- Credit score

- Down payment

- Debt-to-income

- Employment history

These loans are especially popular for first-time buyers and those with moderate income or limited savings.

Minimum Credit Expectations Under FHA Guidelines

FHA loans are known for accommodating a wider range of credit profiles than many conventional products. Technically, you can qualify with a score as low as 500, but that typically requires a larger down payment.

More importantly, FHA lenders review your full credit picture, including:

- Payment history and patterns

- Recent bankruptcies or foreclosures

- Collection accounts and judgments

- Explanation of any unique financial circumstances

Because each lender sets their own standards, called “lender overlays”, two different lenders may look at the same credit profile differently. That’s why it’s often wise to speak with multiple FHA-approved lenders to find the one whose expectations match your situation.

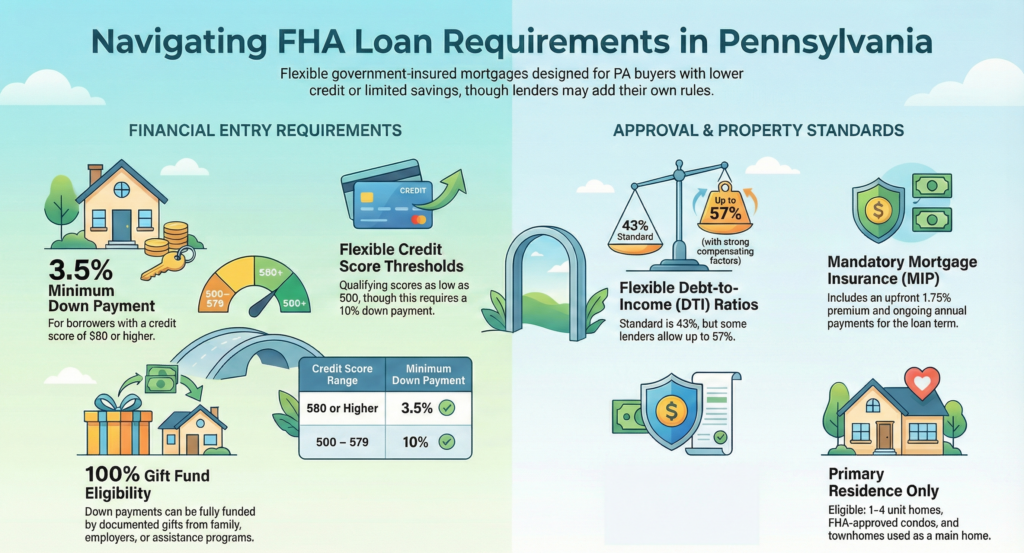

Down Payment Requirements in Pennsylvania

One of the most attractive features of FHA loan requirements in PA is the low down payment threshold:

- 3.5% down if your credit score is 580 or above

- Around 10% down if your score falls between 500–579

Both your down payment and renovation costs (if applicable) are combined in programs like the FHA 203(k). This makes it easier to finance improvements along with the home purchase, even when cash is limited.

Using Gift Funds Toward Your Down Payment

If you don’t have enough savings for the down payment, FHA guidelines allow family members, employers, friends with documented financial interest, or qualified assistance programs to gift down payment funds, provided proper documentation and a gift letter are supplied.

Understanding Debt-to-Income (DTI) Requirements

Debt-to-income ratio (DTI) measures the portion of your gross monthly income that goes toward debt payments, including your projected mortgage payment.

With FHA loans, you’ll commonly see DTI standards in the 40–43% range, but many lenders allow higher ratios, sometimes up to 50–57%, when compensating factors exist (like strong savings or a history of on-time payments).

Keeping your overall monthly debt payments in check (credit cards, student loans, auto loans, etc.) helps strengthen your application and signals to lenders that you can manage new and existing obligations responsibly.

Employment and Income Stability

Consistent income and predictable employment are essential parts of meeting FHA loan requirements in PA. Lenders typically want to see at least two years of steady employment, which may include:

- Multiple jobs over the period, as long as your income is stable or increasing

- Acceptable reasons for brief employment gaps (education, medical leave, etc.)

- Documentation that supports your earnings over time

If you’ve switched jobs within a year, lenders may seek additional verification that your income will continue. And if you’ve had extended gaps, lenders usually want documented reasons that show your financial stability wasn’t compromised.

There are valid exceptions, such as time spent in school, military service, medical leave, or being a full-time caregiver, but these typically require strong supporting documentation to demonstrate ongoing financial stability.

FHA Loan Limits in Pennsylvania

FHA loans have maximum lending limits that vary by county and home type, from $541,287 for single-family homes in most areas to $630,200 in higher-cost metros in 2026. In Pennsylvania, this means the maximum amount you can borrow with an FHA loan depends on the specific county where the property is located.

These limits are updated annually and intended to reflect local housing costs. Make sure your purchase price does not exceed the FHA limit for your county; your lender will verify this before closing.

To see Pennsylvania FHA loan limits for each county, refer to this link.

Mortgage Insurance Premium (MIP): Upfront and Ongoing

All FHA loans require mortgage insurance to protect lenders in the event of default. This insurance has two parts:

- Upfront Mortgage Insurance Premium (UFMIP): Usually 1.75% of the loan amount and can often be financed into the loan.

- Annual Mortgage Insurance Premium (MIP): Spread out into monthly payments (from 0.5% to 0.75% of the loan amount based on the loan amount.

While this adds to your overall cost, it’s one of the reasons FHA loans can be accessible with lower credit scores and smaller down payments. Be aware that FHA MIP, unlike conventional PMI, typically remains in place for the life of the loan unless:

- You refinance into a non-FHA product at a later date or

- If you made a down payment of more than 10%, you can request that the FHA mortgage insurance (MIP) be removed after 11 years.

Eligible Properties Under FHA Guidelines

To satisfy FHA loan requirements in PA, the home itself must meet basic safety and livability standards. Eligible properties include:

- Single-family homes

- Multi-unit homes (up to four units, with owner occupancy)

- Condominiums approved for FHA financing

- Townhomes and certain mixed-use properties

Properties must be intended as a primary residence, not investment or vacation homes, and you must plan to occupy the property within a specified timeframe.

Additionally, FHA generally prohibits financing homes that were recently flipped (sold within 90 days), unless special circumstances apply and proper documentation is provided.

An FHA appraisal, required for approval, ensures the property meets these minimum standards.

Preparing for Your FHA Loan Journey

Meeting FHA loan requirements in PA isn’t just about checking boxes; it’s about showing lenders that you are financially prepared to take on homeownership responsibly. FHA guidelines may be flexible, but lenders still look for patterns of stability, consistency, and readiness across your entire financial profile.

- Know your credit profile and look for ways to improve it

- Plan ahead for down payment and closing costs

- Keep debts manageable and documented

- Maintain stable employment or provide acceptable explanations for gaps

- Gather all required documentation early

This level of preparation doesn’t just help you qualify; it creates confidence. It’s the foundation of true mortgage readiness, and it’s exactly how the Pennsylvania Mortgage Ready Program helps homebuyers move from planning to approval with clarity and control.

Next Steps: Become Mortgage-Ready and Apply with Confidence

Now that you know what FHA loan requirements in PA entail, from credit and down payment to income, debt, and property standards, your next move should be strategy, not stress.

Take your preparation further with structured guidance, personalized checklists, and coaching that help you become mortgage-ready on your terms.

Ready to take the next step? Sign up for the Mortgage Ready Program and start your journey with confidence.

Frequently Asked Questions

Is meeting FHA loan requirements in PA enough to get approved?

Meeting the minimum FHA guidelines is a starting point, not a guarantee. While FHA allows more flexibility than some loan programs, lenders still evaluate your full financial picture, including credit behavior, income stability, debt structure, savings, and documentation. Mortgage readiness focuses on aligning all of these areas before you apply, which reduces delays and surprises.

Do lenders only look at my credit score for an FHA loan?

No. Your credit score is just one piece of the puzzle. FHA lenders pay close attention to payment history, recent late payments, collections, utilization, and how consistently you’ve managed credit over time. Two borrowers with the same score can receive very different outcomes depending on these factors.

How much money should I have saved before applying?

While FHA loans allow a low down payment, lenders also look for funds to cover closing costs and sometimes reserves. Being mortgage-ready means understanding your full cash-to-close requirement and having documented, acceptable funds in place, not just the minimum down payment.

Can I qualify for an FHA loan if I’ve changed jobs or had gaps in employment?

Yes, but documentation and timing matter. Lenders want to see stable, ongoing income and clear explanations for any gaps. Acceptable reasons may include school, medical leave, caregiving, or career advancement, but they must be supported and fit within FHA and lender guidelines.

What causes delays or denials with FHA loans?

Common issues include applying before credit has stabilized, undocumented or inconsistent income, high debt-to-income ratios, insufficient funds at closing, or missing documentation. Most of these problems can be avoided with proper preparation and guidance before submitting an application.

How does mortgage readiness help with FHA loan approval?

Mortgage readiness helps you prepare ahead of time, organizing your credit, income, debts, savings, and documents so that when you apply, your profile aligns with lender expectations. Instead of reacting to issues during underwriting, you’re positioned proactively, which often leads to smoother approvals and less stress.

0 Comments