When buying a home, your down payment isn’t the only cost to prepare for. There is a set of fees and expenses known as closing costs. These costs cover the services needed to finalize your mortgage and officially transfer the property into your name.

In this comprehensive guide, we’ll walk you through everything you need to know about mortgage closing costs, including what they are, how much they might be, who’s responsible for paying them, and which loans cover closing costs.

Table of Contents

What is Mortgage Closing and What Happens on the Closing Day

The closing day marks the “finish line” of a real estate deal, particularly when the buyer is using financing. While a cash purchase is very quick, involving only a few documents to transfer ownership, the process is more complex when financing is involved.

The mortgage closing is the culmination of the deal where the buyer assumes the loan obligation, and ownership is legally transferred. It involves setting a specific date with the lender, reviewing the final figures, signing numerous documents related to the loan and property transfer, and exchanging funds and keys.

What Happens on the Closing Day?

The closing process is facilitated by a settlement agent (or closing agent), who manages the dispersal of funds and handles all checks.

1. Reviewing the Closing Disclosure

Before the closing date, the lender should provide the buyer with a document called a Closing Disclosure at least three days beforehand. This document details all aspects of the loan, including:

- The purchase price.

- The loan amount and interest rate.

- The monthly payment.

- A detailed listing of all closing costs.

- The final cash amount due from the buyer at the closing table (“cash to close”).

The buyer should review this document thoroughly before arrival and can bring it along to ensure the final numbers align.

2. Attendees and Seating

On the closing day, usually, the following individuals are present:

- The buyer, potentially their spouse, or anyone else who co-signed the loan.

- The sellers.

- The buyer’s realtor or attorney.

- The seller’s realtor.

- The settlement agent (closing agent).

The standard setup involves the buyers sitting on one side, the sellers on another side, and the closing agent facilitating the process.

3. Signing Documents

The buyer will sign documents. Most of the paperwork concerns the mortgage and the loan application. Documents to be signed include:

- The loan application.

- The note which is the official promise to pay back the loan.

- Documents discussing the mortgage, the terms of repayment, and any details concerning penalties or late fees.

The buyer is encouraged to ask questions to the realtor, mortgage advisor, or closing agent to ensure comfort and understanding of the deal.

4. Items the Buyer Must Bring

The buyer is required to bring two main items to the closing:

- Photo ID (usually a driver’s license).

- Cash to close. This is the final amount due out of pocket, as specified by the loan officer.

The cash to close must be from a certified source of funds and is typically delivered in one of two ways:

- A cashier’s check is handed directly to the closing agent.

- A wire transfer of funds to the title company, usually completed a couple of days before the closing, especially if the amount is high.

5. Transfer of Ownership

After the loan documents are finalized, attention shifts to the final deed. Signing this document officially transfers ownership of the property from the seller to the buyer, making the buyer the final homeowner.

6. Dispersal of Funds and Keys

The closing agent will then disperse the funds, often right at the closing table. This involves:

- The seller receives a check for their portion.

- The closing agent receives the buyer’s cash to close (either a cashier’s check or a receipt of the wire transfer).

- Commission checks potentially being received by the agents and loan officers.

Finally, the buyer receives the keys to the home, provided that occupancy is being traded at the closing table. However, the contract may sometimes allow the seller a few days post-closing to move out before the keys or codes are exchanged.

Overall, the closing day should not be a cause for stress, as the hard work has already been completed; the day is mostly for reviewing documents, fulfilling obligations, and finalizing the money transfer to receive ownership.

What Are Mortgage Closing Costs?

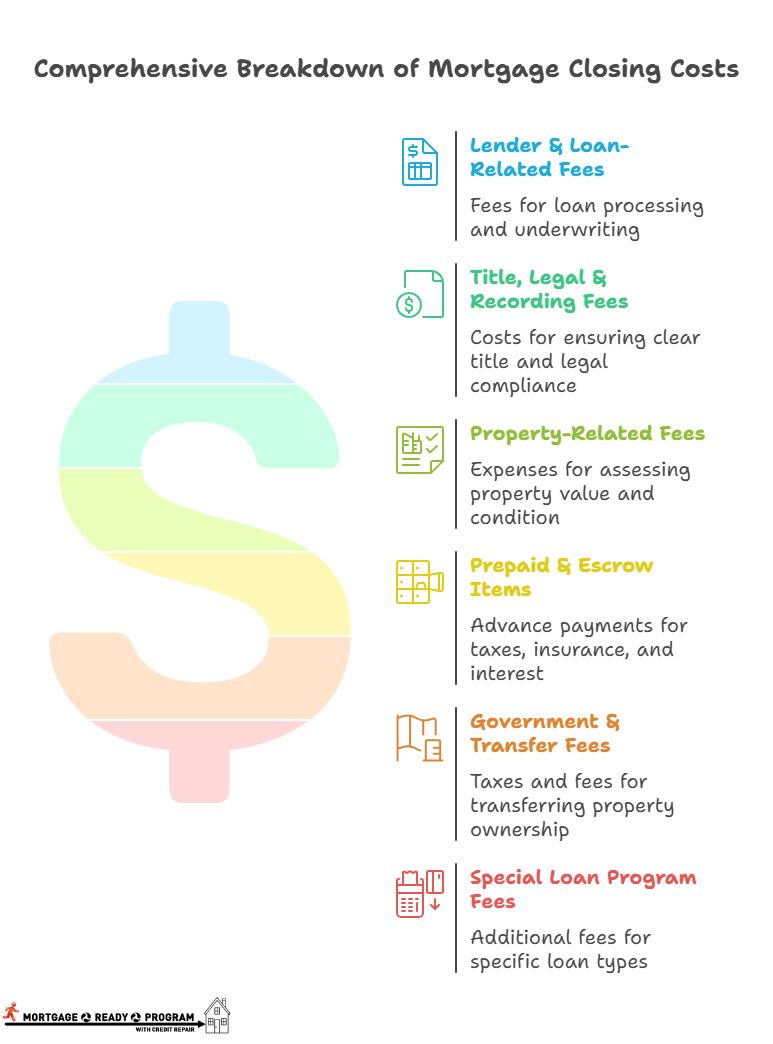

Mortgage closing costs are the fees associated with finalizing a home purchase and mortgage loan. Here’s a complete breakdown by category:

Lender & Loan-Related Fees

- Loan Origination Fee – Charged by the lender for processing and underwriting your loan (usually 0.5–1% of the loan).

- Application Fee – Covers the cost of processing your loan application (varies by lender).

- Underwriting Fee – For verifying your income, assets, and creditworthiness.

- Credit Report Fee – Cost to pull your credit history.

- Rate Lock Fee (optional) – If you lock your rate for a long period before closing.

- Discount Points (optional) – Prepaid interest that lowers your mortgage rate.

Title, Legal & Recording Fees

- Title Search Fee – Ensures there are no liens or ownership disputes.

- Title Insurance (Lender’s Policy) – Protects the lender against title defects.

- Title Insurance (Owner’s Policy) – Optional but recommended; protects you.

- Attorney Fee (if applicable) – For states where an attorney must be present at closing.

- Recording Fees – Charged by the local government to record your deed and mortgage.

- Courier or Wire Transfer Fee – For sending loan funds or documents securely.

Property-Related Fees

- Appraisal Fee – Determines the fair market value of the home (usually $400–$700).

- Home Inspection Fee – Checks for defects before closing ($300–$600).

- Survey Fee (if required) – Confirms property boundaries.

- Pest Inspection Fee – Often required by FHA/VA loans or in certain states.

Prepaid & Escrow Items

- Prepaid Property Taxes – You may need to pay taxes in advance at closing.

- Homeowners Insurance Premium – Usually the first year is paid upfront.

- Prepaid Interest – Covers interest from the closing date to the first payment.

- Initial Escrow Deposit – A reserve account for future taxes and insurance.

Government & Transfer Fees

- Transfer Taxes – State or local tax charged when ownership changes hands.

- Recording Taxes or Stamps – Paid to the county or state for recording the transaction.

Special Loan Program Fees (if applicable)

- FHA Upfront Mortgage Insurance Premium (UFMIP) – 1.75% of the loan amount (can be financed).

- VA Funding Fee – 0.5–3.6% depending on loan type and veteran status.

- USDA Guarantee Fee – 1% upfront and 0.35% annual fee.

- 203(k) Supplemental Fees – For renovation loans, may include HUD consultant and draw inspection fees.

How Much Are Mortgage Closing Costs?

Mortgage closing costs can vary, but they generally range from 2% to 5% of the home’s purchase price. For example, if you’re buying a home for $300,000, you can expect to pay anywhere between $6,000 to $15,000 in closing costs.

It’s essential to ask your lender for an estimate of closing costs early in the process so you can budget accordingly.

Who Should Pay the Mortgage Closing Costs?

Closing costs are usually paid by the buyer, but that’s not always the case. In a buyer’s market, or when a seller is motivated, they may agree to cover some of those costs – mainly the real estate agent’s commission and, in many areas, the transfer tax – to help the deal go through. The amount is negotiable, and your agent can help you structure the offer in a way that makes sense.

When a seller agrees to pay part of the buyer’s closing costs, it’s called a seller concession. Concessions can make a big difference in helping a buyer get to the closing table, especially when cash is tight. According to a report by Redfin on Apr 21, 2025, “Home sellers gave concessions to buyers in 44.4% of U.S. home-sale transactions in the first quarter.” This number for Philadelphia is 27.6%.

That said, lenders limit how much a seller can contribute based on the loan type:

- Conventional loans:

- Up to 3% of the sale price (or appraised value, whichever is lower) if the buyer’s down payment is under 10%.

- Up to 6% if the down payment is between 10% and 25%.

- Up to 9% if the down payment is 25% or more.

- For investment properties, the limit is 2%, no matter the down payment.

- FHA loans: Up to 6% of the sales price.

- USDA loans: Up to 6% of the sales price.

- VA loans: Up to 4% of the loan amount.

When Are Closing Costs Paid?

Mortgage closing costs are typically due at the time of closing. You’ll need to bring a cashier’s check or wire transfer for the amount specified in your closing disclosure. This is usually done a few days before closing to allow enough time for funds to be processed.

Which Loan Covers Closing Costs?

Not all loans cover closing costs, but some do. Here’s a breakdown:

- FHA Loans: FHA loans allow sellers to contribute up to 6% of the home purchase price toward closing costs.

- VA Loans: Veterans Affairs (VA) loans generally don’t require closing costs for eligible veterans. The seller can pay for them in some cases.

- Conventional Loans: Closing costs are typically the buyer’s responsibility, but some lenders may offer closing cost assistance through special programs or by rolling them into the loan itself.

If you live in Philadelphia and you are buying your first home, you may be eligible for this closing cost assistance program.

Conclusion

If you’ve made it so far, you’ve learned a lot about mortgage closing costs. Remember, closing costs vary depending on your lender, location, and the property itself. Always review your Loan Estimate and Closing Disclosure carefully so you know exactly what you’ll owe before signing.

Ready to take the next step toward homeownership? The Mortgage Ready Program can help you get prepared and improve your chances of securing a mortgage. Sign up today to get started on your journey to owning a home!

FAQs

1. Can closing costs be rolled into the mortgage?

Yes, in some cases, your lender may allow you to roll closing costs into your mortgage loan, although this will increase your monthly payments and the overall amount you owe.

2. Are closing costs the same for everyone?

No, closing costs vary depending on the loan type, lender, location, and the price of the home. It’s important to review your loan estimate closely.

3. Can I negotiate closing costs with my lender?

In some cases, you may be able to negotiate certain fees. It’s worth asking your lender if they can reduce or waive specific charges.

4. Do closing costs include the down payment?

No, closing costs are separate from the down payment. While both are required at closing, the down payment is applied toward the purchase price of the home, while closing costs cover fees associated with securing the mortgage.

0 Comments