Buying a home is one of the biggest financial decisions you’ll ever make. And before you start scrolling through listings or attending open houses, you’ll likely come across two important terms: Mortgage Pre-Approval vs. Pre-Qualification. While they may sound similar, they serve very different purposes in the homebuying journey. Understanding these differences is crucial if you want to set a realistic budget, make a strong offer, and move smoothly through closing. In this guide, we’ll break down Mortgage Pre-Approval vs. Pre-Qualification in detail, explain why one carries more weight than the other, and show you how to use both strategically.

Understanding your financial standing before making an offer is exactly what the Mortgage Ready Process is designed to help you do.

Table of Contents

Mortgage Pre-Approval vs. Pre-Qualification: The Core Difference

At the simplest level:

- Pre-Qualification is a rough estimate of what you might be able to borrow.

- Pre-Approval is a conditional commitment from a lender after verifying your financial information.

Both are valuable tools, but only pre-approval carries the kind of authority that makes sellers take you seriously. Pre-qualification is like looking at a house from the street, while pre-approval is equivalent to a thorough home inspection.

What Is Mortgage Pre-Qualification?

Pre-qualification is the first step many buyers take to gauge their readiness. It’s quick, informal, and based on the information you provide.

Pre-qualification is often the starting point in first-time homebuyer readiness, helping buyers understand affordability before taking more serious steps.

Features of Pre-Qualification

- Self-Reported Data: You’ll share details about your income, debts, and assets. No supporting documents are typically required.

- Soft Credit Inquiry: Some lenders may do a soft pull (which does not affect your credit score), while others may skip the credit check entirely.

- Speed: The process can take just minutes, often available via online calculators or lender apps.

- No Commitment: It doesn’t guarantee approval or loan terms.

Why Pre-Qualification Is Useful

- Helps you set an initial budget range.

- Allows you to compare lenders and mortgage products without obligations.

- Ideal if you’re just exploring the idea of buying a home.

For example, Alex is curious whether he can buy a condo in his city. He uses a lender’s online pre-qualification tool, inputs his salary and debt, and sees that he might qualify for a $250,000 loan. This helps him plan, but it’s not binding.

What Is Mortgage Pre-Approval?

Pre-approval is where things get serious. Here, lenders take a deep dive into your financial picture.

Features of Pre-Approval

- Document Verification: You’ll need to provide

- Last 2 years’ W-2s and tax returns

- Recent pay stubs (30 days)

- Bank statements (2 months)

- Investment account statements

- Valid government-issued ID

- Hard Credit Inquiry: Lenders run a hard pull on your credit, which may slightly lower your score (usually by 5–10 points).

- Conditional Offer: You receive a pre-approval letter that specifies how much you can borrow and may include an estimated interest rate.

- Stronger Authority: Sellers and real estate agents take pre-approval as a sign you’re a credible buyer.

Because pre-approval includes a full credit review, improving your credit for a mortgage before applying can significantly strengthen your results.

Why Pre-Approval Is Crucial

- Provides a clear spending limit so you don’t waste time looking at homes outside your range.

- Strengthens your offer in a competitive market.

- Prepares you for faster closing, since much of the underwriting is already complete.

Mortgage Pre-Approval vs. Pre-Qualification: Side-by-Side Comparison

| Feature | Pre-Qualification | Pre-Approval |

| Verification | Based on self-reported data. | Verified with official financial documents. |

| Credit Check | Soft inquiry, no credit impact. | Hard inquiry, may lower score slightly. |

| Timeframe | Minutes. | Days to a week, depending on responsiveness. |

| Result | Budget estimate. | Conditional loan commitment. |

| Seller Perception | Weak; shows only preliminary interest. | Strong; shows you’re ready and financially capable. |

Why Pre-Approval Matters More Than Pre-Qualification

While both tools are useful, pre-approval provides clear advantages that can make or break your homebuying experience.

1. Stronger Negotiating Power

Sellers prefer buyers with pre-approval because it reduces the risk of financing falling through.

2. A Defined Budget

Knowing your exact pre-approved loan amount prevents disappointment and wasted time. Instead of “guessing,” you’re working with verified numbers.

3. Faster Closing

Because your documents and financials have already been reviewed, the lender’s final approval process is much faster, often shaving weeks off closing.

4. Credibility in Bidding Wars

In competitive markets, pre-approval often makes the difference between winning and losing a home. In a Rochester, NY area real estate blog, Kyle Hiscock recounts a multiple-offer situation in which two bids came in for the same property: one from a buyer who was pre-qualified and another from a buyer who was pre-approved. Even though the pre-approved buyer’s offer was $1,000 lower, the seller accepted it over the higher pre-qualified offer. Why? The seller (and their agent) believed the pre-approved buyer was more likely to successfully close the deal.

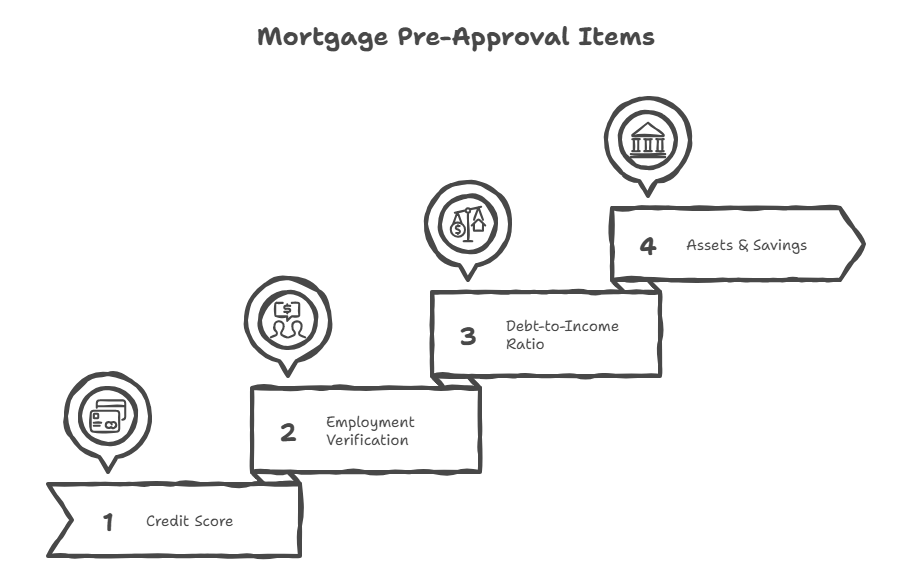

What Lenders Check During Pre-Approval

Pre-approval isn’t just about the numbers; it’s about proving financial stability. Here’s what lenders review:

1. Credit Score & History

Your credit score is one of the most important factors in the pre-approval process because it shows how responsibly you’ve handled debt in the past. Lenders use this three-digit number, along with your credit history, to determine your eligibility and to set your interest rate. Most conventional mortgages, as well as FHA loans, require a minimum credit score of 620. However, just meeting the minimum doesn’t guarantee favorable terms. Borrowers with higher scores, typically 740 and above, are more likely to secure lower interest rates, better loan options, and smoother approvals. In addition to the score itself, lenders review your credit history for red flags such as late payments, accounts in collections, or recent bankruptcies. A clean, consistent record reassures them that you’re a low-risk borrower.

2. Employment & Income Verification

Lenders also want to see stability in your employment and income. They aren’t just looking at how much you earn, they’re checking whether your income is steady and reliable. Typically, they like to see at least two years of consistent employment with the same employer or within the same field. This doesn’t mean job changes automatically disqualify you, but frequent shifts in career paths or gaps in employment may raise questions. For self-employed applicants, the process can be more rigorous, often requiring multiple years of tax returns and business documentation to prove consistent income. Why does this matter? Because lenders want to be sure you’ll be able to make your monthly mortgage payments over the long term. Stable income reduces their risk and increases your chances of approval.

3. Debt-to-Income Ratio (DTI)

Even if you earn a high income, lenders want to know how much of that income is already committed to existing debts. That’s where your debt-to-income ratio (DTI) comes into play. DTI measures the percentage of your gross monthly income that goes toward debts such as student loans, car payments, credit cards, and personal loans. Most lenders look for a DTI of 36% or less, which signals that your debt load is manageable. However, some loan programs, such as FHA loans, are more flexible, allowing DTIs as high as 43–50%. For example, if your monthly income is $6,000 and your debt payments total $2,000, your DTI would be about 33%. This falls comfortably within the typical range lenders like to see. A higher DTI doesn’t necessarily disqualify you, but it may limit the loan amount you can be approved for or result in higher interest rates.

4. Assets & Savings

Finally, lenders want to see proof of your assets and savings. This isn’t just about confirming that you have enough for the down payment; it’s also about ensuring you have funds set aside for closing costs and reserves. Reserves are particularly important because they demonstrate that you’ll still have money left after the purchase to cover unexpected expenses or emergencies. For instance, lenders may want to see that you have enough cash or liquid assets to cover two to six months of mortgage payments, even after paying your down payment and closing costs. Assets can include checking and savings accounts, retirement funds, or investment accounts. The more financial cushion you can demonstrate, the stronger your pre-approval application will be. For tips on improving credit and lowering debt-to-income ratio, check out our guide to financial readiness before homebuying.

The Negatives of Pre-Approval

While pre-approval is generally the stronger and more reliable step compared to pre-qualification, it isn’t without its drawbacks. Understanding these potential downsides can help you prepare for the process and avoid common mistakes.

1. Hard Credit Inquiry

One of the first things to know about pre-approval is that it involves a hard credit inquiry. Unlike the soft checks used during pre-qualification, a hard pull is recorded on your credit report and can temporarily lower your score by about 5–10 points. For most borrowers, this dip is minor and short-lived. However, if you’re on the borderline of a credit tier, for example, moving from a “good” range to “fair” it might affect the interest rate or loan options you qualify for. The good news? Credit scoring models, like FICO, typically treat multiple mortgage inquiries within a 45-day window as a single inquiry. This means you can shop around with several lenders without severely damaging your score. Still, it’s smart to check your credit before applying, resolve any errors, and pay down small debts to strengthen your position.

2. Time & Documentation Requirements

Another drawback of pre-approval is the time and effort required to provide documentation. Lenders will request a variety of financial records, including recent pay stubs, W-2s or tax returns, bank statements, and sometimes proof of additional assets. For borrowers with straightforward finances, this may only take a few hours. But if you’re self-employed, have multiple income sources, or own investment properties, gathering and organizing these documents can feel like a second job. In some cases, lenders may come back with follow-up requests, adding more time to the process. While this may feel burdensome, it’s a necessary step to prove your financial stability and the effort pays off once you’re ready to make a strong offer on a home.

3. Expiration of Pre-Approval

A pre-approval letter isn’t valid indefinitely. Most lenders issue them for 60 to 90 days. If you don’t find a home and make an offer within that timeframe, your letter will expire, and you’ll need to go through parts of the process again. This typically involves resubmitting updated bank statements or pay stubs and, in some cases, undergoing another credit check. For buyers in competitive markets, where it can take months to find the right property, this can feel frustrating and repetitive. To avoid unnecessary hassle, it’s best to time your pre-approval strategically; ideally when you’re ready to start touring homes seriously, not just browsing.

4. Emotional Pressure

Finally, pre-approval can create psychological pressure. When you receive a letter stating the maximum amount you qualify for, it’s tempting to treat that figure as your shopping budget. For example, if the lender pre-approves you for $400,000, you may feel inclined to only look at homes near that price, even if a $325,000 property would be a better fit for your financial comfort. This mindset can lead to overstretching your budget. Remember, pre-approval shows what you can borrow, not necessarily what you should. A good rule of thumb is to balance your lender’s number with your own comfort level, taking into account lifestyle expenses, savings goals, and potential future costs like childcare or home repairs.

Which One Do You Need?

Choose Pre-Qualification if… You’re just exploring whether you’re ready to buy. It’s an excellent first step for budgeting and gauging affordability. Choose Pre-Approval if… You’re serious about buying and plan to make an offer. A pre-approval letter is almost always required by sellers before accepting a bid. Most buyers start with pre-qualification and then move on to pre-approval once they’re ready to shop seriously.

Extra Considerations in the Pre-Approval Process

- While a pre-approval letter includes an estimated loan amount, some lenders also allow you to lock in your interest rate for a limited time. This rate lock ensures that even if market rates rise during your home search, your locked rate remains the same (so long as you close within the lock period and don’t make material changes to your loan application)

- First-time buyers often find pre-approval particularly valuable. It helps avoid surprises and builds credibility in markets where sellers may hesitate with inexperienced buyers.

- Some lenders offer “fully underwritten pre-approval,” which is even stronger. This involves an underwriter reviewing your file in advance, giving sellers near certainty of closing.

Final Thoughts: Mortgage Pre-Approval vs. Pre-Qualification

When it comes to Mortgage Pre-Approval vs. Pre-Qualification, both serve a role in the homebuying process, but pre-approval is the stronger, more valuable step. By moving beyond pre-qualification and securing a pre-approval, you’ll not only gain confidence but also increase your chances of landing your dream home in a competitive market. Ready to take the next step toward homeownership? Sign up for the Mortgage Ready Program today and put yourself in the strongest position possible when it’s time to make an offer.

Frequently Asked Questions (FAQ)

1. Is it better to be pre-approved or pre-qualified?

Pre-approval is better if you’re serious about buying. Pre-qualification is only a planning tool.

2. Does a pre-approval hurt your credit score?

Slightly. A hard inquiry typically lowers your score by only a few points and is temporary.

3. Does getting pre-approved cost money?

Many lenders offer it for free, though some may charge application fees. Always ask before applying.

4. Can I get pre-approved with bad credit?

Yes, but your loan options may be limited, and interest rates will likely be higher. Programs like FHA loans may still be available.

0 Comments