Do you remember our previous article about verifiable incomes? If you didn’t read that, take a quick look at it before moving on with this article.

So you need a verifiable income as a fundamental part of your mortgage application. One of these types of income could be disability income. If you or a family member receives disability benefits, you need to understand which types of disability income are considered verifiable by lenders.

In this article, we will explore disability income and mortgages and discuss how these benefits are treated as income when applying for a mortgage. Let’s get started!

Table of Contents

Disability Income and Mortgages

First, let’s explore what disability income is. Disability income refers to financial support provided to individuals who are unable to work due to a disability. These benefits help cover living expenses and are intended to replace the income lost because of the inability to work.

Income is an essential factor that proves to lenders that you are able to pay back your mortgage. While traditional employment income is commonly used to qualify for a mortgage, disability income can also serve as a reliable source of income for mortgage approval. If you or a family member receives disability benefits, this income can help demonstrate your ability to repay the loan.

Now, let’s explore the different disability income programs that lenders may consider when you apply for a mortgage.

Understanding the Disability Income Programs

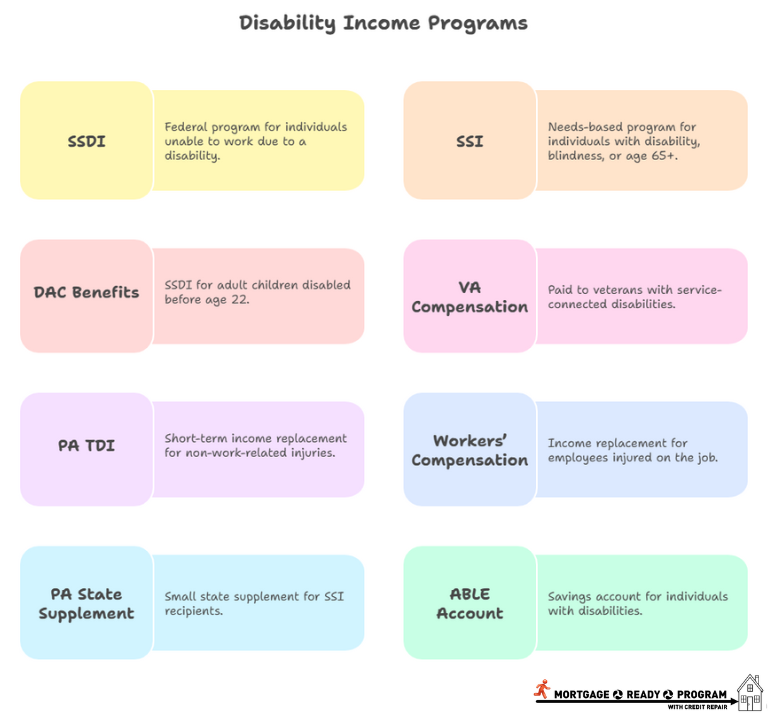

First, let’s break down the most widely known disability programs and how they work:

1. Social Security Disability Insurance (SSDI)

SSDI is a federal program designed to provide financial assistance to individuals who are unable to work due to a disability that is expected to last at least 12 months or result in death. To qualify for SSDI, individuals must have worked in jobs covered by Social Security and paid into the system for a required number of years.

Application: Apply online at ssa.gov/applyfordisability.

More info: Visit ssa.gov/disability.

2. Supplemental Security Income (SSI)

SSI is a needs-based program for individuals who have a disability, are blind, or are aged 65 or older, and have limited income and resources. SSI is available to those who may not have enough work history to qualify for SSDI, but who still meet the disability criteria.

While SSI is government-provided and guaranteed, it is a needs-based benefit. This means that the income and assets of the applicant or the applicant’s family are taken into consideration. SSI income is typically considered verifiable income, but only if the child or adult receiving SSI has a disability and the payments are ongoing.

Application: Apply online at ssa.gov/apply/ssi.

More info: Visit ssa.gov/ssi.

3. Disabled Adult Child (DAC) Benefits

Disabled Adult Child (DAC) benefits are a form of SSDI available to individuals who were disabled before age 22 and are the adult child of a parent who is receiving SSDI or who is deceased. The child must meet Social Security’s definition of disability to qualify for DAC benefits.

Like SSDI, DAC benefits are considered verifiable income, but only if the adult child is receiving the benefits because their parent qualifies for SSDI. The key here is that DAC benefits are a type of SSDI, so they are treated the same way by lenders.

This booklet will help you decide if you, your child, or a child you know may be eligible for SSI, SSDI, or DAC.

4. Veterans Affairs (VA) Disability Compensation

VA disability compensation is paid to veterans with service-connected disabilities. The benefit amount depends on the severity of the disability, which is rated by the VA. VA benefits are federal, guaranteed, and ongoing.

More info: Visit https://www.va.gov/disability/.

5. Temporary Disability Insurance (TDI) – Pennsylvania

PA TDI provides short-term income replacement for workers temporarily unable to work due to non-work-related injuries or illnesses. Benefits are typically paid weekly.

TDI can be considered verifiable only if the benefits are expected to continue during the mortgage application period. Because it is short-term, lenders may NOT count TDI for long-term mortgage qualification.

6. Workers’ Compensation (WC)

Workers’ compensation provides income replacement for employees injured on the job. Payments can be weekly or monthly, depending on state rules and settlement agreements.

Ongoing WC payments are considered verifiable for mortgage purposes. One-time lump-sum settlements or irregular payments generally cannot be counted as stable income.

7. Pennsylvania State Supplement (for SSI Recipients)

Pennsylvania offers a small state supplement to individuals already receiving federal SSI benefits. This supplement helps residents with additional cost-of-living support.

More info: Visit https://www.ssa.gov/pubs/EN-05-11150.pdf.

8. ABLE Account Withdrawals (for Disabled Individuals)

An ABLE account is a special savings account for individuals with disabilities (onset before age 26) that allows them to save money without affecting eligibility for benefits like SSI or Medicaid. Money in the account can be used for qualified disability expenses, such as medical costs, housing, or education. Withdrawals from the account are considered verifiable income for mortgages only if they are used regularly to support living expenses, like rent or utilities.

More info: Visit paable.gov.

Which Disability Income Sources Are Most Reliable for Mortgages

Now, let’s explore which disability income sources are the most dependable and can be counted as verifiable income when applying for a mortgage.

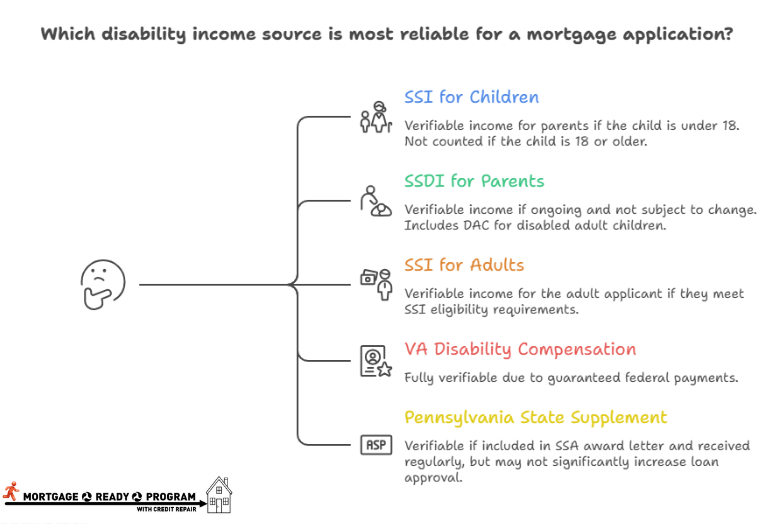

1. SSI for Children Under 18

If a parent or guardian is applying for a mortgage and a child under 18 is receiving SSI due to a disability, the SSI income is generally considered verifiable income for the household. The lender will count this income as part of the household income for mortgage qualification, and it will be used in the debt-to-income (DTI) ratio calculation.

The parent will need to provide the child’s SSI award letter and bank statements showing regular payments.

Note: Once the child turns 18, SSI is no longer considered the parents’ income; it becomes the child’s income. This income is not counted for the parents’ mortgage application. The SSI payments are not included in the parents’ household income for mortgage qualification purposes. So, if the child is over 18 and the parents are applying for a mortgage, the lender will not count the child’s SSI as part of the parents’ income unless the child qualifies for other forms of assistance, such as DAC benefits under SSDI.

2. SSDI for Parents (Including DAC for Disabled Adult Children)

SSDI payments are regular and guaranteed for those who qualify, which makes them verifiable income for mortgage purposes. For a mortgage, lenders will typically accept SSDI benefits as income if they are ongoing and not subject to change, unless there’s a specific indication that the disability benefits will end or change soon (such as a re-evaluation of the condition).

If the parent is receiving SSDI or the parent is deceased, and the child is receiving DAC benefits, these benefits are considered verifiable income for the household when applying for a mortgage. The parents’ SSDI or DAC benefits can be included in the DTI calculation for the parents’ mortgage application.

The parent or adult child receiving SSDI or DAC benefits will need to provide the SSDI or DAC award letter and bank statements showing regular payments.

3. SSI for a Disabled Adult (18 or Older)

If the disabled adult child is applying for a mortgage on their own and receiving SSI, the payments can be included as verifiable income in their mortgage application. However, as SSI is a needs-based program, the applicant must also meet income and asset limits for SSI eligibility, and this can affect the mortgage process.

The applicant will need to provide the SSI award letter and bank statements as evidence of their income.

4. Veterans Affairs (VA) Disability Compensation

VA disability payments are considered fully verifiable because they are guaranteed monthly federal payments.

5. Pennsylvania State Supplement (for SSI Recipients)

If this supplement amount is included in the SSA award letter and received regularly, it can be considered as a verifiable income. However, since it is typically a smaller amount, it might not significantly increase loan approval amounts.

Non-Verifiable or Limitedly Verifiable Income Sources

When it comes to disability income and mortgages, these income types may be more challenging to verify and might require additional documentation, or may not be accepted by all lenders:

1. Cash Income

- Documentation: Difficult to document; may require bank statements showing regular deposits and a history of cash transactions.

- Stability: Hard to demonstrate consistency and reliability.

2. No-Doc and Low-Doc Loans

- Description: Loans that require minimal or no documentation of income.

- Considerations: Typically offered to borrowers with strong credit histories and substantial down payments.

3. Seasonal or Irregular Income

- Documentation: May include pay stubs and tax returns, but income variability can be a concern.

- Stability: Lenders may require a longer history to assess income consistency.

4. Unverifiable Foreign Income

- Documentation: Difficult to obtain equivalent documentation; may require translations and verifications from foreign institutions.

- Stability: Challenges in assessing consistency and reliability.

Conclusion

So, did you see how disability income and mortgages can relate? This income can be verifiable for mortgages, but there are details for each program to understand. It’s crucial to prepare proper documentation, such as benefit verification letters and bank statements, to show that the income is consistent and ongoing. Always check with the lender to understand how disability income will be treated in your specific mortgage application.

And if you need assistance at every step of the mortgage process, count on MortgageReadyProgram. We are here to help you. Sign up Today!

0 Comments