One of the most misunderstood parts of the mortgage process is how lenders verify your savings, down payment funds, and reserves. Many homebuyers assume lenders only look at the balance in their bank account, but that’s not how underwriting works. Lenders don’t just check how much you have. They check:

- where it came from,

- how long it has been there, and

- whether it’s acceptable under federal lending guidelines.

If you don’t know the rules, even innocent mistakes, like transferring money between your own accounts, can cause delays or denials.

This guide breaks down what lenders look for in bank statements for mortgages, so you know exactly how to prepare your accounts and avoid red flags.

Table of Contents

Why Bank Statements Are a Non-Negotiable Document

Lenders use your bank statements to verify the story told by your application and credit report. They need proof that you can not only afford the down payment and closing costs but also maintain sufficient cash reserves to handle future mortgage payments alongside life’s unexpected expenses. It’s a reality check on your financial health.

If your statements raise questions or show weak cash patterns, it can slow down underwriting or even hurt your approval chances. That’s why preparing your finances in advance is critical. If you’re unsure where to start, this guide on how to improve your credit for a mortgage walks you through the steps lenders actually care about, before your bank statements and credit profile are under the microscope.

The Four Pillars of Bank Analysing Bank Statements for Mortgages

Underwriters systematically examine your statements through four critical lenses:

1. Income Verification & Consistency

Lenders cross-reference the regular deposits on your statements with the income stated on your application. They look for:

-

Paycheck Stubs as Live Deposits: Consistent direct deposits from your employer that match your claimed salary.

-

Self-Employment & Business Revenue: For freelancers or business owners, deposits must show steady, credible income over a longer period (often 12-24 months).

-

Other Qualifying Income: Regular deposits from pensions, Social Security, or rental properties.

The Goal: To confirm a stable, verifiable income stream capable of repaying the loan.

2. Spending Habits & Financial Management

Your transaction history reveals your financial discipline. Underwriters analyze:

-

Recurring Monthly Obligations: Regular payments for loans, credit cards, subscriptions, and utilities.

-

Discretionary Spending: Patterns in dining, entertainment, and shopping.

-

Cash Flow Analysis: Ensuring your typical monthly income exceeds your monthly outflows.

The Goal: To determine if you live within your means and can absorb a new mortgage payment without strain.

3. Account Stability & History

Lenders prefer a narrative of control and growth. They assess:

-

Balance Trends: Is your balance steadily growing, stable, or frequently dipping near zero?

-

Transaction Patterns: Are there frantic, frequent transfers between accounts or to unfamiliar entities?

-

Account Age: Older, well-maintained accounts suggest financial maturity.

The Goal: To see responsible cash management and avoid accounts that appear chaotic or unreliable.

4. Sourced & Seasoned Assets

Funds for your home purchase must be transparent and stable. This involves two key concepts:

-

Sourcing: Lenders must know the exact origin of any large deposit. Acceptable sources include documented sales (e.g., a car), tax refunds, or properly documented gifts.

-

Seasoning: Money must typically be in your account for at least 60 days (two full statement cycles) to be considered “seasoned.” This proves it’s truly your asset and not a hidden loan.

The Goal: To prevent money laundering and ensure your down payment funds are your own, not borrowed.

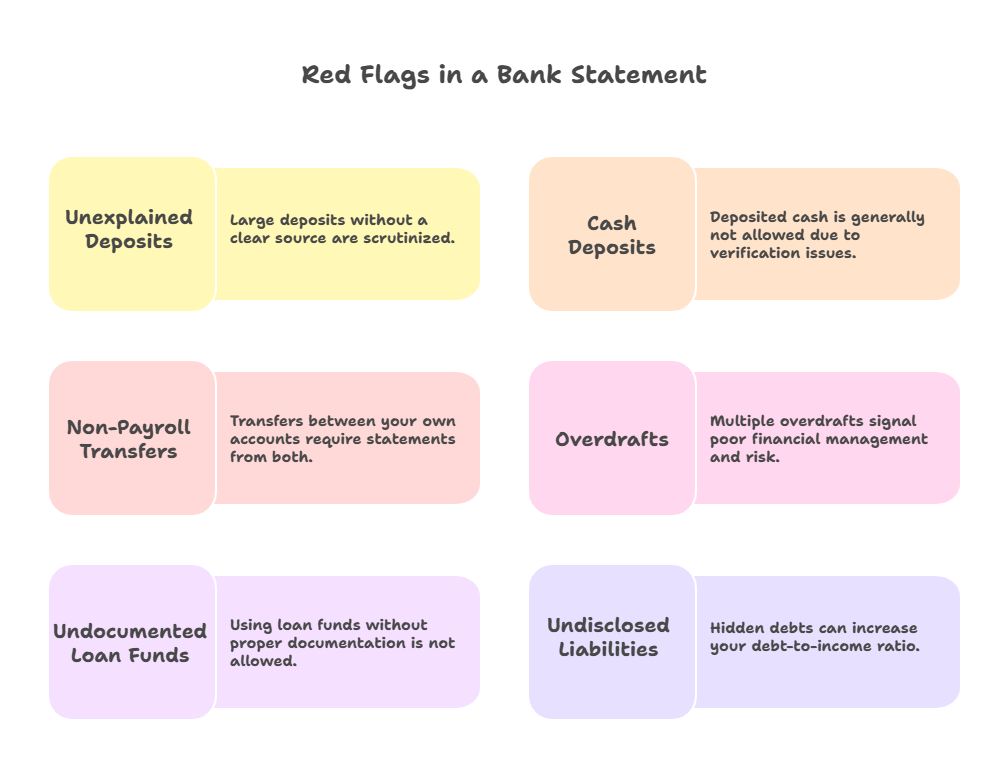

Critical Red Flags That Can Derail Your Mortgage Approval

Certain patterns trigger immediate scrutiny and can lead to delays, conditions, or denial.

1. Unexplained Large Deposits

This is the #1 issue that delays mortgage approval. A “large deposit” means:

- Any deposit that is not your paycheck

- Any amount greater than 50% of your monthly income (Fannie Mae rule and FHA rule)

- Any amount that’s inconsistent with your pattern

If the source cannot be proven, the deposit cannot be used. Lenders will subtract unverifiable deposits from your available funds.

2. Cash Deposits (Almost Always Unusable)

Deposited cash is not allowed for:

- FHA

- Conventional

- VA

- USDA

Why? Because lenders cannot verify where the cash came from. If it’s in the form of:

- ATM cash deposit

- Cash handed to you

- Tips deposited as cash

- Cash savings suddenly appearing in the bank

…it will almost certainly not be allowed.

3. Non-Payroll Transfers Between Your Own Accounts

This confuses many buyers. If you transfer your own money from:

- CashApp → Checking

- Chime → Savings

- PayPal → Checking

- One bank → Another bank

The underwriter may require statements from BOTH accounts. Because a transfer is considered a “large deposit” unless the lender sees both sides of the transaction.

4. Overdrafts

An overdraft occurs when you don’t have enough money in your account to cover a transaction, but the bank pays the transaction anyway. Overdrafts signal poor cash management, inconsistent finances, and a high risk of mortgage default. A single overdraft may be okay. Multiple overdrafts in the last 60 days can:

- Delay approval

- Require explanations

- Result in denial (especially for FHA)

5. Using Loan Funds Without Documentation

If the money came from a personal loan, credit card cash advance, payday loan, Zelle from a friend, Venmo from a family member, it’s not allowed, unless properly documented and acceptable under law.

If it came from a:

- Gift → you need a gift letter + proof of donor’s funds

- 401(k) loan → you need loan terms + repayment schedule

- Sale of personal property → you need a bill of sale + proof of deposit

6. Undisclosed Liabilities

Regular automated withdrawals to a creditor not listed on your credit report (e.g., a private loan, “buy now, pay later” plan, or undisclosed auto payment) suggest hidden debt. This can unexpectedly increase your debt-to-income (DTI) ratio beyond qualifying limits.

Documentation Requirements: Getting It Right

As mentioned above, lenders get a lot of information from your bank statement. For this reason, bank statements for mortgages are highly important. To ensure a smooth process:

-

Provide ALL pages of each statement, even blank ones or terms and conditions pages.

-

Submit 2-3 months of the most recent statements for traditional W-2 employees.

-

Self-employed borrowers should be prepared to provide 12-24 months of statements to demonstrate income stability.

-

For gift funds, include a signed gift letter from the donor (meeting lender specifications), proof of the donor’s ability to give, and documentation of the transfer.

The Future is Here: AI and the Forensic Audit

When it comes to bank statements for mortgages, lenders are no longer relying only on human review. Many of them now use AI-powered tools to analyze your statements faster and more accurately. What used to take days can now be done in minutes, so you need to be extra careful with what shows up on your account.

These systems basically run a deep audit of your bank activity. They can spot altered documents, fake transactions, or anything that looks off, things like inconsistent fonts or edited numbers. Even small details that a human might overlook can get flagged.

AI tools also look for unusual patterns. Perfectly rounded deposits, missing check numbers, or strange gaps in transactions can raise questions. And beyond that, lenders use this data to study your cash flow over time. They want to see if your balance history supports your ability to make future mortgage payments, not just today but months down the line.

With AI involved in the review process, accuracy and consistency are critical. One careless move can slow things down or create unnecessary problems during underwriting.

Proactive Steps Before You Apply

Follow these rules for at least 60 days before pre-approval:

- Plan Ahead: Keep your money in ONE primary account. Avoid large, unexplained deposits for at least two months before applying.

- Avoid Overdrafts Entirely

- Simplify Your Accounts: Minimize excessive transfers between accounts. Consider consolidating funds.

- Document Everything: Keep records for any unusual deposits (sale receipts, gift letters).

- Review Your Statements: Scrutinize your own last 3 months of statements with a lender’s eye. What story do they tell?

Conclusion

Bank statements for mortgages are not just another item on a lender’s checklist; they’re a critical part of your entire mortgage package. This is one document you can’t afford to overlook or treat casually. Lenders need to see a complete, clear, and credible financial picture before they feel confident approving your loan. When everything lines up, it tells them one simple story: you’re prepared, reliable, and ready for homeownership.

Understanding how lenders review your finances gives you a real advantage. Our Mortgage Readiness Guide helps you prepare every piece of the puzzle so there are no surprises during underwriting.

If you’re serious about buying a home and want to do it the right way, sign up now and start your homeownership journey with confidence.

0 Comments