Conditional mortgage approval is the moment when things start to feel real. You’re no longer just hoping to buy a home; you’re officially in the game. At this stage, the underwriter is basically saying: your numbers look good, your file makes sense, and we’re moving forward, but there are still a few boxes that must be checked before the money can be released. Those boxes are your conditions.

In this article, we break down what conditional mortgage approval really means, the most common conditions lenders ask for, the mistakes that can cause problems, and how to get through the final stretch to closing without surprises. Let’s get started!

Table of Contents

The Underwriter’s Role in Conditional Approval

Conditional mortgage approval doesn’t happen by accident. It’s driven by the mortgage underwriter. Think of the underwriter as a financial detective. They don’t just look at numbers; they look at patterns, consistency, and the full story behind your finances.

They review your credit history, debt-to-income ratio, assets, and job stability to answer one simple question: Is this borrower safe to lend to?

When an underwriter issues a conditional approval, what they’re really saying is:

“Your file looks solid. We’re comfortable moving forward, but we need a few final items to confirm everything before releasing the money.”

Those conditions are not a bad sign. They’re a normal and necessary part of the process. This step exists to make sure nothing is missed before the lender commits hundreds of thousands of dollars to the loan.

Conditional Approval vs. Other Key Mortgage Milestones

A lot of buyers mix up the different approval stages, so let’s put them in the right order, clearly and simply.

- Prequalification: This is the very first step. It’s usually a quick conversation about your income and debts. No documents are verified, and nothing is guaranteed. It’s just a rough estimate.

- Preapproval: Now things get more serious. Your credit is pulled, and basic documents are reviewed. You get a borrowing range, but this is still not a final commitment from the lender.

- Upfront / Verified Approvals: Some lenders underwrite early and give a stronger preapproval. This is helpful, but it’s still not the finish line. Once you choose a property, more conditions usually follow.

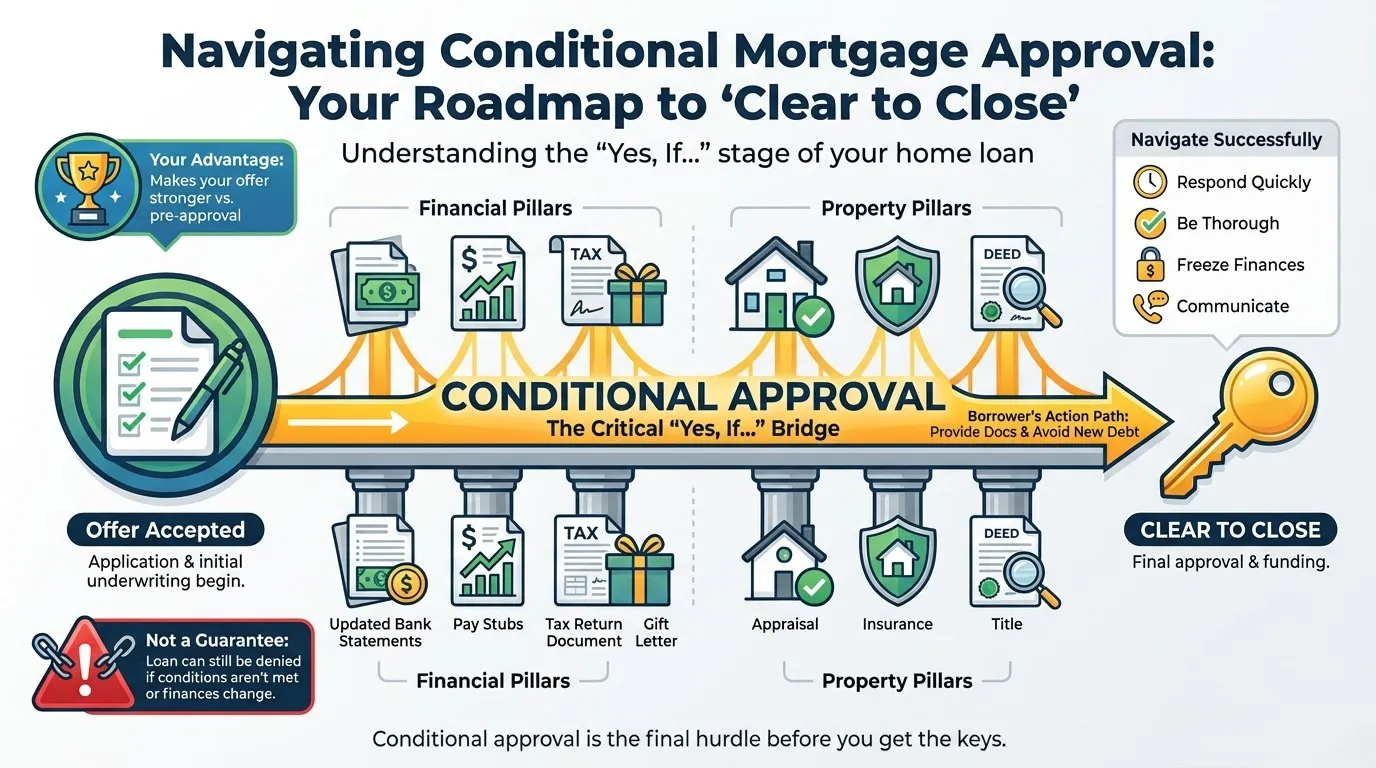

- Conditional Mortgage Approval: This happens after you’re under contract on a specific home. The underwriter has fully reviewed your file and approved the loan with conditions. At this point, you’re in a very strong position as a buyer, but the work isn’t done yet.

- Clear to Close (Final Approval): This is the green light. All conditions are satisfied, documents are finalized, and the lender is ready to fund the loan. Closing day is next.

Understanding where you are in this timeline helps you stay calm, focused, and proactive, especially during the conditional approval stage, where smart decisions matter the most.

If you’re a first-time buyer and want to make sure you’re fully prepared for each step, check out our First-Time Homebuyer Readiness Guide to stay ahead of the process.

Common Conditions of a Mortgage Approval

Why Conditional Approval Is a Big Win for Homebuyers

In a competitive market, conditional mortgage approval is one of the strongest cards you can play, right after a solid offer. Let’s see why:

- Stronger Offers: Sellers see conditional approval as proof that your financing is almost done. Compared to a basic preapproval, it makes your offer look safer, cleaner, and more likely to close.

- Faster Closing: Since the heavy underwriting work is already completed, clearing conditions is usually straightforward. That often means fewer surprises and a quicker path to closing.

- Builder Green Light: For new construction, most builders won’t even start without conditional approval. It shows them your loan is real, not just theoretical.

- Clear Direction: Instead of guessing where you stand, you get a clear checklist. You know exactly what’s needed and nothing more.

Can a Conditionally Approved Loan Still Be Denied?

Yes, conditional approval is not a final green light. It’s a “yes, as long as everything stays exactly as expected.” And that distinction matters.

Even at this stage, a loan can still fall apart. Major financial changes like opening new credit cards, buying a car, changing jobs, or experiencing a drop in income can stop a loan fast, sometimes just days before closing. Failing to satisfy conditions is another common issue. Missing documents, delays, or unresolved title problems can easily stall or kill the deal.

A low appraisal is another risk. If the home comes in below the purchase price and the buyer and seller can’t renegotiate, the loan may not move forward. And finally, any misrepresentation or errors, whether intentional or not, can lead to

Navigating to the Finish Line: A Borrower’s Checklist

If you want conditional approval to turn into clear to close, discipline matters.

- Move Fast: Treat every condition as urgent. If you can submit documents within 24–48 hours, do it.

- Be Precise: Make sure everything is complete, signed, and dated correctly. Small mistakes cause big delays.

- Freeze Your Finances: No new debt. No big purchases. No strange money moves. Wait until the keys are in your hand.

- Communicate Early: If something might delay a condition, tell your loan officer right away. Silence causes problems—communication solves them.

Once you submit your last condition, the underwriter performs a final review. If all is satisfactory, you will receive your Closing Disclosure (CD). By law, you must receive this document at least three business days before closing. Review it meticulously against your Loan Estimate to ensure no unexpected changes.

The “three-day rule” allows you to confirm the loan terms, interest rate, and cash-to-close amount. On closing day, you’ll sign a mountain of paperwork, the lender will fund the loan, and you’ll receive the keys to your new home.

Conclusion

The path to homeownership has a lot of steps, but conditional mortgage approval is one of the most important ones. It’s the bridge between applying for a loan and actually owning the home. Reaching this stage means you’ve made real progress, but it also means your focus needs to be sharp.

When you understand what conditional approval really means, respect the conditions attached to it, and move quickly to satisfy each one, you turn that cautious “yes, if…” into a solid “clear to close.” There’s no guesswork here; just follow the checklist, stay financially steady, and work closely with your lending team.

If you’re ready to start your homebuying journey the smart way, sign up today and get prepared from day one.

0 Comments