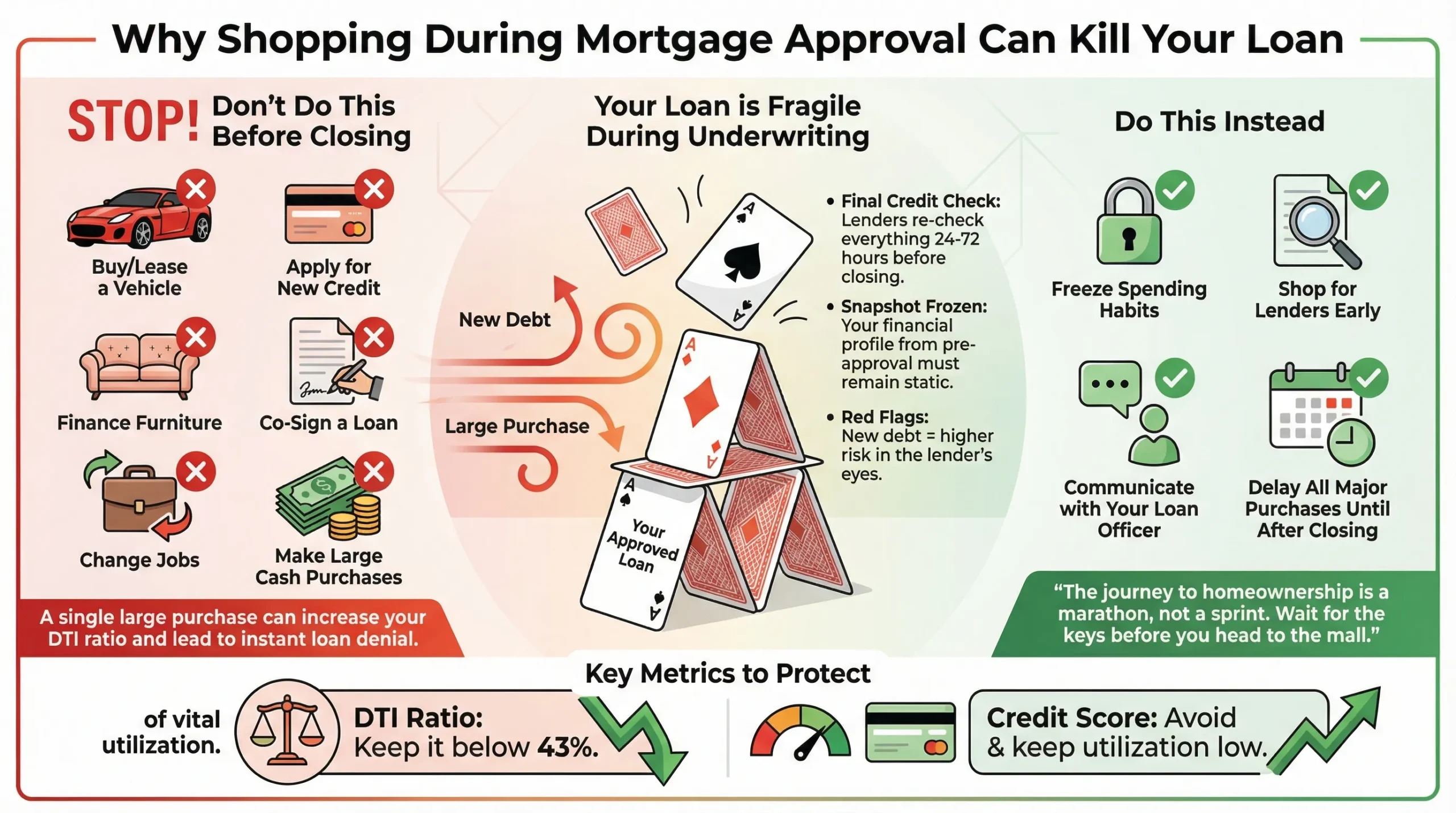

Shopping during the mortgage approval process is one of those mistakes that sounds harmless but can kill a deal at the last minute. I get it, you’re excited, you’re already picturing the new place, the couch, the car, the upgrades. But from application to closing, lenders are watching your finances very closely.

Your approval is based on a specific financial snapshot. Any change to that picture, like opening a new credit, financing furniture, buying a car, or even moving large amounts of cash, can trigger red flags. And once that happens, the lender can pause, re-underwrite, or deny the loan, even if you were days away from closing.

Let’s see how shopping during mortgage approval should be to protect your loan!

Table of Contents

The Critical Phase: Understanding Mortgage Underwriting

Many homebuyers mistakenly believe that once they receive a preapproval letter, their financing is guaranteed. However, a preapproval is merely a conditional approval based on the financial details provided at that specific time. The actual “heavy lifting” occurs during underwriting, where a mortgage underwriter performs a thorough examination of your employment history, debts, and assets to ensure you can afford the long-term commitment of a loan.

Underwriters are trained to look for “red flags,” which include any activity that suggests your financial stability has shifted. Because lenders typically perform a final credit check in the week leading up to closing, any shopping you have done in the interim will be revealed. If your credit score has dropped or your debt levels have risen, the lender has the legal right to change their mind and deny the loan.

The Two Key Numbers You Must Protect

When you apply for a mortgage, you are essentially promising the lender that your financial situation will remain static. Two metrics are paramount, and shopping during mortgage approval jeopardizes both.

1. Your Debt-to-Income (DTI) Ratio

This is the percentage of your monthly gross income that goes toward paying debts (like car loans, student loans, credit cards, and the proposed mortgage). Most conventional loans have a strict DTI limit of 43-45%.

How Shopping Breaks It: Any new monthly payment, even a “no interest for 18 months” furniture payment, is counted as debt. Adding a $300 car payment or a $150 appliance financing plan can easily push you over the DTI threshold, transforming you from an approved borrower to a denied one overnight.

2. Your Cash Reserves and Assets

Lenders need to verify you have sufficient funds for the down payment and closing costs. More importantly, they often require proof of “reserves,” which is extra money left in the bank after closing to cover several months of mortgage payments. This proves you can handle emergencies without defaulting.

How Shopping Breaks It: A large cash purchase for a new living room set or a vacation booked before moving day directly depletes the assets the lender counted on. A suddenly lowered bank balance can trigger a request for further documentation or lead to denial if you no longer meet reserve requirements.

The Double-Edged Sword of Credit Inquiries

It’s crucial to distinguish between two types of inquiries: those for shopping for a mortgage and those for shopping for goods.

-

Smart Shopping: For a Lender. You are encouraged to get multiple mortgage quotes. Credit scoring models typically treat all hard inquiries for a mortgage made within a 14-45-day window as a single inquiry, minimizing the impact on your score.

-

Dangerous Shopping: For Credit. Applying for a new store credit card to get 10% off, financing a mattress, or getting a personal loan triggers a hard inquiry. Each can ding your credit score by 5-10 points and signals to underwriters that you are taking on new debt.

Furthermore, charging large amounts on existing cards increases your credit utilization ratio (the amount of credit you’re using versus your total limit). High utilization is a major factor in credit scores, and a sudden spike can cause a rapid decline.

12 Forbidden Activities Before Your Loan Closes

To ensure your loan sails through underwriting, avoid these activities entirely from application until the moment you have keys in hand:

-

Applying for new credit cards (including retail/store cards).

-

Buying or leasing a vehicle (the most common “loan killer”).

-

Financing furniture, appliances, or electronics.

-

Cosigning a loan for anyone (it becomes your legal debt).

-

Changing jobs or becoming self-employed (stability is key).

-

Closing existing credit accounts (this can hurt your credit age and utilization).

-

Making large, undocumented cash deposits (lenders must source all funds).

-

Moving money between accounts without a clear paper trail.

-

Making late payments on any existing bills.

-

Taking out payday loans or cash advances (a huge red flag).

-

Making large non-payroll deposits without a proper “gift letter” if from family.

-

Quitting your job to relocate (wait until after closing).

What If You Must Make a Purchase?

Life happens. If a critical, unavoidable expense arises (e.g., a car repair, a medical bill), transparency is your only shield. Contact your loan officer immediately, before making the purchase. They can advise you on the best way to proceed, perhaps by documenting the necessity or recalculating your qualifications. Never assume a purchase is “small enough” to fly under the radar.

Proactive Protection: Guarding Your Financial Profile

The best strategy is a defensive one:

-

Freeze Your Credit: Consider a soft freeze with the major bureaus to prevent new credit applications.

-

Live Frugally: Stick to essential purchases using your regular income.

-

Document Everything: If you receive any large monetary gifts, work with your lender to provide a proper gift letter upfront.

-

Communicate Constantly: Keep your loan officer informed of any changes in your income or life circumstances.

The Right Way to Shop: For Your Mortgage

Ironically, while you should avoid shopping for goods, you are strongly advised to shop during mortgage approval processfor your lender. Getting multiple loan estimates can save you thousands over the life of the loan. Do this early, during the preapproval stage, and concentrate your inquiries within a focused period to minimize credit score impact.

Shopping during mortgage approval for anything other than your loan terms is a high-stakes gamble with your dream home as the wager. The underwriting process is designed to ensure you can afford your new house, and last-minute debts contradict that very premise. View this period as a financial quiet zone. Your future self, the one relaxing in a home you own, will thank you for your discipline. Keep your finances steady, your credit report quiet, and delay all major spending until the day after you officially close. The mall, the car dealership, and the furniture store will all still be there, but your loan approval might not be if you visit them too soon.

Conclusion

The space between application and closing is not the time to test your luck. Shopping during mortgage approval can undo months, or even years, of hard work in a matter of hours. Underwriting is all about stability. The quieter your financial life stays during this phase, the smoother your loan will move to the closing table.

If you want to avoid costly mistakes and make sure you’re truly prepared, start with our Mortgage Readiness Guide. It walks you through what lenders look for, what to avoid, and how to protect your approval from day one

And if you want hands-on support from start to finish, the Mortgage Ready Program (MRP) is built exactly for this stage. We help you prepare, stay compliant during underwriting, and get to closing without unnecessary stress.

Sign up for MRP today and move toward homeownership the smart, safe way.

0 Comments