When you’re getting ready to buy a home, one number matters more than most people realize: your debt-to-income ratio, or DTI. Simply put, DTI compares your monthly debts to your monthly income. The lower this number is, the better your chances of getting approved for a mortgage.

In our previous article, “Debt-to-Income Ratio for Mortgages: A Comprehensive Guide,” we explained what the DTI is and how to calculate it. Here, we’re focusing on what lenders actually consider an acceptable DTI for mortgage approval, especially for first-time homebuyers, and how it affects your approval.

Let’s get started!

Table of Contents

What Is Mortgage Readiness and Why Is DTI Important for That?

Are you really ready for a mortgage, or do you just feel ready?

Mortgage readiness is more than being able to make a monthly payment. It’s about your overall financial picture and whether you’re truly prepared to take on a home loan. When lenders review your application, they look at several factors, and your debt-to-income ratio (DTI) is one of the big ones.

A strong mortgage profile shows lenders that you can handle a mortgage on top of your current debts without stress.

- A lower DTI means more breathing room in your budget and more confidence from the lender.

- A higher DTI, on the other hand, tells them that most of your income is already spoken for, which can slow things down or stop approval altogether.

Understanding what an acceptable DTI for mortgage approval looks like is one of the first real steps toward homeownership. If you want to take a deeper look at where you stand, check out our First-Time Homebuyer Readiness page.

What Is Considered an Acceptable DTI for Different Types of Mortgages?

Short answer? There is no one-size-fits-all answer here. Each loan type looks at DTI a little differently. Below is a simple breakdown of the most common mortgage options and what lenders usually accept.

Quick note: the numbers below are back-end DTI ratios. If you’re not sure what front-end vs back-end means, check out our article on Debt-to-Income Ratio for Mortgages.

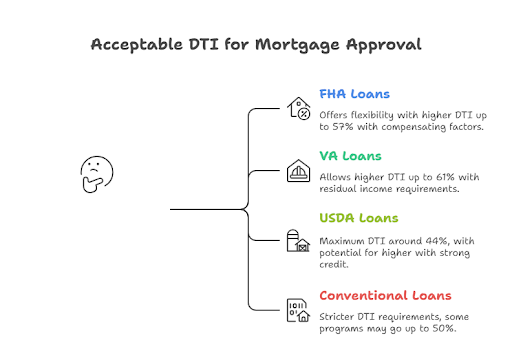

1. FHA Loans

FHA loans are very popular with first-time homebuyers. They allow lower credit scores and smaller down payments. The general guideline is a 43% DTI, but in reality, you can still get approved with a DTI as high as 57%. Of course, that higher number doesn’t come for free; you usually need strong compensating factors like a higher down payment or solid reserves. We’ll talk more about this later.

2. VA Loans

VA loans are backed by the Department of Veterans Affairs and are designed to help veterans and active-duty service members. The standard DTI is around 41%, but VA loans are more flexible than most people think. Higher DTIs can be approved based on residual income and other factors. At some lenders, if your DTI goes over 41%, you may need to meet 120% of the residual income requirement. Approvals might go up to 61% in some cases. Isn’t that crazy?

3. USDA Loans

USDA loans are meant for rural homebuyers. The standard DTI is usually around 41%, with a maximum of about 44%. Like other loans, this can be stretched if the borrower has strong credit and financials. The exact cap isn’t always clear, and it really depends on the lender.

4. Conventional Loans

Conventional loans are usually stricter. Most lenders want to see a DTI between 36% and 45%. Some programs may go up to 50% if you have excellent credit and strong compensating factors. But honestly, those cases are rare and not something you should count on.

Acceptable DTI for Mortgage Approval

Compensating Factors: When Is a Higher DTI Acceptable?

Having a high DTI doesn’t automatically kill your mortgage application. Lenders know real life isn’t perfect. If your numbers are strong in other areas, they may still approve the loan. These are called compensating factors. Basically, things that show you can still handle the mortgage even with a higher DTI. How much they matter depends on the loan type.

1. FHA Loans

FHA loans are flexible. Some common compensating factors are:

- Cash reserves: Lenders like to see money left over after closing. Usually, FHA wants at least three months of mortgage payments for a 1-2 unit property, and six months for 3-4 units.

- Small increase in housing payment: If your new mortgage payment isn’t much higher than what you’re paying now, that helps a lot.

- No unnecessary debt: If you don’t carry credit card balances or random loans, it strengthens your file.

- Extra income: Sometimes you have income that doesn’t fully count on paper, but still shows you can pay the loan.

- Residual income: This is the money left after all your main expenses. Lenders want to see you still have breathing room.

Note: All of this must be verified by the lender, and some lenders may ask for more. It’s never exactly the same.

2. VA Loans

VA loans are very unique and more flexible, but they are still serious about stability. Common compensating factors include:

- Strong credit history

- Low existing debt

- Long-term employment

- Good amount of liquid savings

- Military benefits

- High residual income

- Past homeownership experience

The VA wants compensating factors that are above normal guidelines. For example, a decent credit score might not help if residual income is low. But a very high score could change the whole picture.

3. USDA Loans

USDA loans also allow higher DTI if certain boxes are checked:

- Cash reserves: Usually three months of PITI after closing.

- Stable job history: Two years with the same employer is ideal. Social Security or retirement income can also count.

- Small payment increase: Your new payment shouldn’t be more than $100 or 5% higher than what you’ve paid over the last year.

- Energy-efficient homes: Homes that meet energy standards can actually help offset a higher DTI. Not many people know this.

4. Conventional Loans

Conventional loans look at similar factors, but they are usually stricter:

- Stable employment

- Higher credit score

- Larger down payment

Automated systems like Fannie Mae’s DU may allow DTI up to 50% if everything else is strong. Manual underwriting is tougher, but compensating factors still matter.

Lenders don’t just look at one number. If your DTI is high but you have savings, good credit, and steady income, you’re not out of the game. Compensating factors can make a big difference, sometimes more than people expect.

The Impact of DTI on Your Loan Terms

Your DTI doesn’t just affect your mortgage approval; it can also impact the loan terms you’re offered. For instance, borrowers with high DTIs might face:

-

- Higher Interest Rates: If your DTI is on the higher end, lenders might charge you a higher interest rate to compensate for the added risk.

- Larger Down Payment Requirements: In some cases, lenders may require a larger down payment if your DTI is high. This helps reduce the risk for the lender.

- Higher Interest Rates: If your DTI is on the higher end, lenders might charge you a higher interest rate to compensate for the added risk.

- Borrowing Limit: A high DTI may limit how much you can borrow.

What to Do If Your DTI Is Too High?

If your DTI is too high, there are several steps you can take to improve your chances of mortgage approval:

- Pay Down Debt: Start by paying off high-interest credit card debt and other loans. This reduces your monthly debt obligations and lowers your DTI.

- Increase Income: If possible, consider ways to increase your income through a side job or asking for a raise at your current job.

- Improve Your Credit Score: A higher credit score can give you more flexibility in terms of the DTI ratio you can qualify for.

Conclusion

The ideal DTI for mortgage approval is typically 43% or lower, but this can vary depending on the type of loan and compensating factors like your credit score and down payment. While a higher DTI can complicate the mortgage approval process, it is not an automatic disqualifier, especially if you have other strong financial characteristics.

Understanding your DTI and what is considered an acceptable DTI for mortgage approval is essential when preparing for homeownership. With proper planning, you can increase your chances of approval, even with a higher DTI.

Sign up now and let’s work on improving your financial profile today!

0 Comments