How to buy a house with bad credit? This is one of the most common questions for people who feel locked out of homeownership because of their credit score. If your score is under 580, you may think buying a house isn’t possible or that you’ll need years of credit repair before even trying.

The reality is different.

Today’s mortgage programs, updated lending guidelines, and smart preparation strategies have made it possible to buy a house with bad credit sooner than most people expect.

In this guide, you’ll learn:

- which loan options work for low credit,

- the lowest scores lenders accept,

- a clear step-by-step roadmap to prepare for mortgage approval, even under 580.

We’ll also cover mistakes to avoid, alternative strategies to qualify faster, grants and assistance programs, and answers to common questions about rates and mortgage insurance. Let’s get started!

Table of Contents

Can You Buy a House With a Credit Score Under 580?

When asking whether you can buy a house with a credit score under 580, it helps to understand why credit scores matter and how lenders assess risk.

- Credit score is a numerical representation of your credit history like payment behavior, amounts owed, length of credit, types of accounts, and recent credit activity.

- Most conventional loans used to require a credit score of at least 620, which served as a simple screening threshold to approve borrowers.

However, rules are changing:

✔ New Conventional Mortgage Rules (Nov. 16, 2025)

As of November 16, 2025, Fannie Mae and Freddie Mac removed the rigid 620 minimum credit score requirement for conventional loans submitted to their underwriting system (Desktop Underwriter). Under the new regime:

- No official minimum credit score exists for conventional loan evaluation.

- Approval is based on a holistic, risk-based assessment of your overall financial profile, such as income, assets, debt, and payment history, rather than a single number.

This means that even with a credit score under 580, you may be able to qualify for a mortgage if other parts of your financial picture are strong.

That shift is huge: it opens the door for many more applicants who were once automatically disqualified.

✔ Government-Backed Options Still Exist

Even before this update, government-insured loans like FHA and VA loans made homeownership possible for credit scores well below the traditional conventional mortgage line. We’ll cover these in detail next.

Best Home Loan Options if You Have Bad Credit

When you want to buy a house with bad credit, not all mortgage programs are created equal. Some have built-in flexibility that makes them a good match for applicants with lower scores.

Here’s an overview of the top programs:

FHA Loans (Federal Housing Administration)

The FHA loan program is one of the most flexible mortgage options for borrowers with low credit scores. FHA loans are backed by the U.S. Department of Housing and Urban Development, so lenders take on less risk and can approve more applicants.

Here’s how they work for bad credit:

- If your credit score is 580 or above, FHA allows you to make a down payment as low as 3.5%.

- If your credit score falls between 500 – 579, you can still qualify, but you’ll typically need a 10% down payment instead.

- No borrower with a credit score below 500 can typically qualify for an FHA home loan.

FHA loans come with mortgage insurance (which protects lenders) and often help buyers who are short on credit but have reliable income and savings.

VA Loans (Veterans Affairs)

If you’re an active duty service member, veteran, or eligible spouse, a VA loan can be an excellent way to buy a house with bad credit, sometimes with:

- No required minimum credit score by law (though individual lenders may set their own minimums).

- No down payment requirement in many cases.

VA loans are backed by the Department of Veterans Affairs and offer competitive terms for qualified applicants.

Fannie Mae and Freddie Mac Conventional Loans

Thanks to the recent removal of a hard minimum credit score, conventional financing through Fannie Mae and Freddie Mac is more accessible to applicants with low credit than it has ever been, as long as:

- Your overall financial profile supports repayment capacity.

- You have documented income, assets, and a reasonable debt-to-income ratio.

This doesn’t magically guarantee approval, but it means a bad credit score alone won’t automatically kill your application.

USDA Loans

For eligible rural or suburban home purchases, USDA loans (backed by the U.S. Department of Agriculture) can allow buyers without strict credit score requirements.

- USDA single-family guaranteed loans don’t set a specific score threshold, but they expect applicants to show willingness and ability to manage debt responsibly. However, , most lenders require credit scores above 640.

USDA loans typically have income limits and property eligibility requirements, but when you qualify, they offer 0% down payment mortgages.

What’s the Lowest Credit Score You Can Buy a House With?

With the evolving rules, the simple answer is: there is no absolute lowest credit score you can use to buy a home. But here are realistic boundaries:

- FHA: You can qualify with credit scores as low as 500 if you can make a 10% down payment.

- Conventional: No minimum score mandated by Fannie Mae or Freddie Mac systems, but lenders still have internal standards and risk thresholds.

- VA: No federal score minimum, though lenders may have their own requirements.

- USDA: No credit score minimum in guidelines, but strong payment history and stable finances help.

In practice, borrowers with scores in the 500–580 range are most commonly approved through FHA loans or a combination of loan programs and underwriting flexibility.

Keep in mind that very low credit scores (below 500) usually require credit improvement before lenders will consider an application.

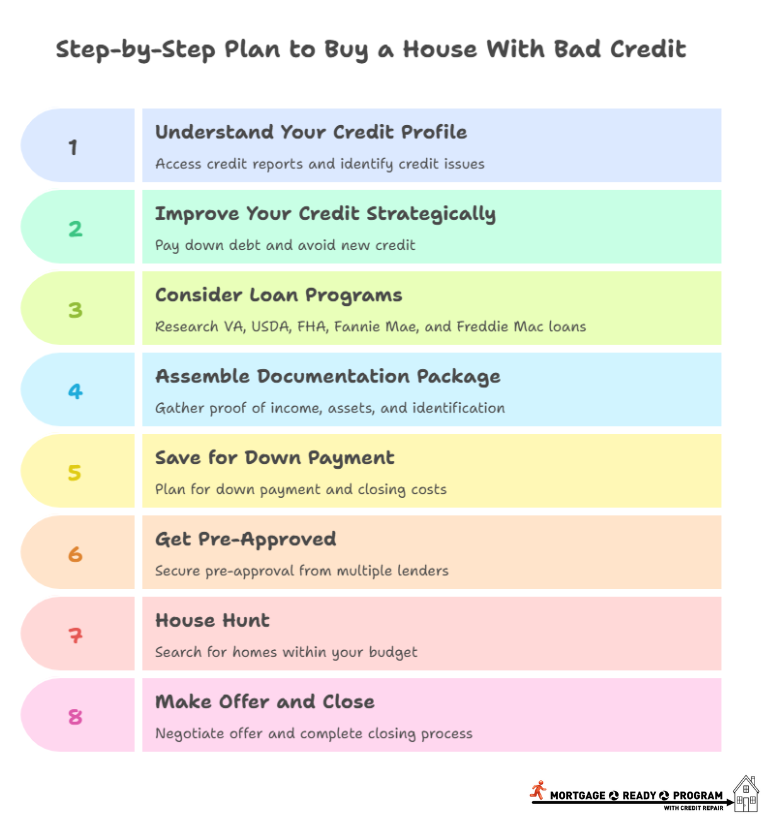

A Comprehensive Step-by-Step Plan to Buy a House With Bad Credit (under 580)

Now for the heart of this article: a realistic, roadmap-style plan you can follow to buy a home even if you’re starting with bad credit.

Step 1: Understand Your Credit Profile

Start by accessing your credit reports from the three major credit bureaus: Experian, Equifax, and TransUnion.

- Check for errors (incorrect accounts, mislabeled payments).

- Identify collections, late payments, and charge-offs.

- Note your FICO® score or VantageScore.

Understanding your starting point helps you create a targeted improvement strategy.

Along with this, build your mortgage readiness checklist by reviewing what lenders will evaluate: income, assets, debt levels, employment history, and credit history. This is also covered in greater depth in the First Time Homebuyer Readiness Guide.

Step 2: Improve Your Credit Strategically

While you may be able to secure a mortgage with bad credit, improving your score can lower your interest rate and increase your loan options. That’s what the Improve Credit for Mortgage resource can help you do.

Here are ways to strengthen your credit profile:

- Pay down overdue accounts and high-interest debt.

- Bring past-due accounts current.

- Avoid opening unnecessary new credit lines before applying.

- Keep credit utilization under 30% on revolving accounts.

- Negotiate the removal of negative information when possible.

Small improvements in credit behavior can materially impact your mortgage qualification strength.

Step 3: Consider Loan Programs That Match Your Profile

Based on your credit and financial situation, research which loan programs are available to you.

- If you’re a veteran or servicemember, see if a VA loan fits your goals.

- If you’re buying in a rural or suburban area, look into USDA guaranteed loans.

- If your score falls between 500–579, investigate FHA, Fannie Mae, or Freddie Mac financing.

Different lenders interpret guidelines differently, so shop around; lenders willing to approve a borrower at 550 with a 10% down payment might decline another applicant with identical scores because of risk tolerance differences.

Step 4: Assemble a Documentation Package

Mortgage underwriting is documentation-intensive. Typical requirements include:

- Proof of income (W-2s, tax returns, pay stubs)

- Asset statements (bank statements, investments)

- Identification and Social Security numbers

- Explanations for derogatory credit items

Having documentation organized, especially explanations for credit challenges, helps underwriters see the full context of your credit history.

Step 5: Save for Down Payment and Closing Costs

Bad credit doesn’t erase the need for funds to purchase a home. The amount you’ll need depends on the loan type:

- FHA: 3.5% down with a 580+ score; 10% down if score 500-579.

- VA and USDA: Often 0% down.

- Conventional: Down payment varies by lender; now more flexible with holistic evaluation.

Set a savings plan and understand all closing costs, including appraisal fees, title insurance, prepaid taxes, and lender fees. Planning early prevents down payment delays.

Step 6: Get Pre-Approved With Multiple Lenders

Pre-approval shows sellers you are a serious buyer and gives you a clear picture of how much you can borrow.

Work with lenders experienced in:

- FHA underwriting

- VA financing

- Conventional loans with holistic risk assessments

Ask them specifically if they approve borrowers with your credit profile, and have them explain underwriting overlays and internal score requirements.

Step 7: House Hunt With a Realistic Budget

Based on your pre-approval amount, start shopping within a price range you can afford.

Factor in:

- Monthly mortgage payment

- Property taxes

- Homeowners insurance

- Mortgage insurance (if required)

Important: Low credit scores often mean you’ll pay higher mortgage interest rates or mandatory mortgage insurance (like FHA’s mortgage insurance premium). Plan for that in your housing budget.

Step 8: Make an Offer and Close

Once you find a home you love and negotiate an offer, your lender will work with you through underwriting and final clear-to-close steps.

Maintain financial discipline; don’t open new credit, make big purchases, or change jobs before closing, as it can delay or derail approval.

Things to Avoid When Buying a Home With Bad Credit

Even well-intentioned buyers make mistakes that cost them time and money:

- Don’t ignore your credit report errors. Fix them before talking to lenders.

- Avoid big purchases (cars, furniture) on credit before closing.

- Don’t underestimate costs like mortgage insurance, taxes, and insurance premiums because low credit can increase these costs.

- Don’t rely on one lender. Different lenders have different risk tolerance; shop multiple approvals.

Alternative Plans to Buying a House With Bad Credit

If your credit score is holding you back from buying a home right now, don’t worry, there are plenty of ways to work around it. Let’s explore some alternative options that can help you become a homeowner, even with bad credit:

1. Rent-to-Own Agreements

If you’re not quite ready to buy but still want to move into a house, a rent-to-own agreement could be a great option. With this setup, you rent the home with the option to buy it later. A portion of your rent payments will go toward the future purchase price, which helps you build up savings for the down payment while improving your credit score over time.

2. Homebuyer Assistance Programs

Don’t forget about the various homebuyer assistance programs that can make a big difference. Many local governments and nonprofits offer grants to help with down payments or closing costs. These programs can make buying a home more affordable, even if your credit isn’t perfect. If you qualify, it could be the financial boost you need to secure your home. Check out the PHFA assistance programs if you live in Pennsylvania.

3. Co-Signers or Non-Occupying Co-Borrowers

If your credit is holding you back, consider asking someone with better credit to co-sign on your mortgage. This could be a family member or friend who agrees to take on some responsibility for the loan. Their stronger credit and income can help boost your chances of getting approved. It’s a smart move if you need a little extra support to qualify.

4. Boost Your Available Credit

One simple way to improve your credit score is by increasing your available credit. This can be done by paying down existing credit card balances or asking your credit card company for a higher credit limit. When you increase your available credit, your credit utilization ratio improves, which is a key factor in boosting your score. It’s an easy way to get things moving in the right direction.

5. Invest In Credit Deletion

If you’ve got old collections affecting your credit score, consider negotiating for them to be deleted from your credit report. Simply paying off a collection won’t remove it from your credit report, but asking the creditor to delete it can have a much greater impact. Getting any agreement in writing can significantly improve your score and put you in a better position to qualify for a mortgage.

6. Avoid Hard Credit Inquiries

Before you apply for a mortgage, try to avoid hard credit inquiries, as they can temporarily lower your credit score. A hard inquiry typically happens when you apply for new credit, like a credit card or loan. The fewer hard inquiries on your report before applying for a mortgage, the better your chances of getting approved.

7. Average Credit Scores for Co-Borrowers

If you’re applying for a mortgage with a co-borrower, Fannie Mae allows you to average your credit scores. So, if your score is 580 and your co-borrower’s score is 720, the lender will use an average score of 650, which could improve your chances of qualifying. However, the lowest credit score will still affect your mortgage rate, so it’s important to consider that when planning your mortgage.

These alternatives provide various ways to work around bad credit and still move toward homeownership. Whether through a co-signer, homebuyer assistance, or improving your credit with smart strategies, there are options out there to help you achieve your dream of owning a home.

Your Path Forward

Buying a house with bad credit requires strategy, education, and persistence. But it’s no longer an insurmountable barrier, not with the evolution of mortgage guidelines, government loan programs, and credit improvement techniques.

But remember, Mortgage readiness is about more than fixing a credit score. Lenders review patterns, stability, and preparation over time, not just numbers on a report. The Mortgage Ready Program is created to help buyers understand what lenders look for and how to prepare their full financial picture before applying for a mortgage. Sign up Now!

FAQs About Buying a Home With Bad Credit

What mortgage rates can I expect with bad credit?

Typically, lower credit scores result in higher interest rates. Lenders price loans based on risk, so a score under 580 may mean a higher cost of financing until your credit improves.

Will I always need mortgage insurance?

Many low-credit options like FHA loans require mortgage insurance regardless of down payment. Some conventional loans allow you to eliminate private mortgage insurance (PMI) once you reach 20% equity.

Can I rebuild credit while trying to buy?

Yes, and you should. Paying down debts, correcting errors, and building positive payment history improve lender confidence.

How soon can I buy after bankruptcy or foreclosure?

Time frames vary by loan type: FHA usually requires 2 years after bankruptcy, conventional may require longer, and VA depends on circumstances. A lender can explain specifics based on your history.

0 Comments