Can I Buy a House with Collections on My Credit Report?

This is a question many aspiring homeowners worry about, fearing that past financial missteps might have permanently shut the door to homeownership. The short answer? Yes, but with caution.

Collections are a serious negative mark on your credit, but they’re not an automatic disqualifier. Whether you can get approved depends on several factors: the type of collections, how old they are, the total amount owed, the mortgage program you’re applying for, and, most importantly, your current financial behavior.

In this guide, we’ll break down what lenders look for, how collections impact your mortgage eligibility, and practical strategies to improve your chances of approval.

Table of Contents

Understanding Collections and Charge-Offs

Before you jump into the home-buying process, it’s important to know exactly what lenders see when they pull your credit report.

A collection account appears when a debt, like a medical bill, credit card, or utility, goes unpaid for 120 to 180 days and gets turned over to a third-party collection agency. A charge-off is a bit different: it happens when the original creditor writes the debt off as a loss, deciding they don’t expect to collect it.

It’s crucial to know that a charged-off debt isn’t forgiven. It stays on your credit report for seven years and is often sold to collection agencies, who may continue attempting to collect until your state’s statute of limitations runs out.

Lenders categorize these items as derogatory credit, which raises red flags about your ability to repay. However, while they are serious marks, they don’t automatically block you from buying a home. With the right strategy and understanding, you can still qualify for a mortgage, even with collections or charge-offs on your report.

How Collections Impact Mortgage Eligibility

Lenders use a multifaceted risk assessment to determine your eligibility. The two most critical components are your credit score and your debt-to-income (DTI) ratio.

-

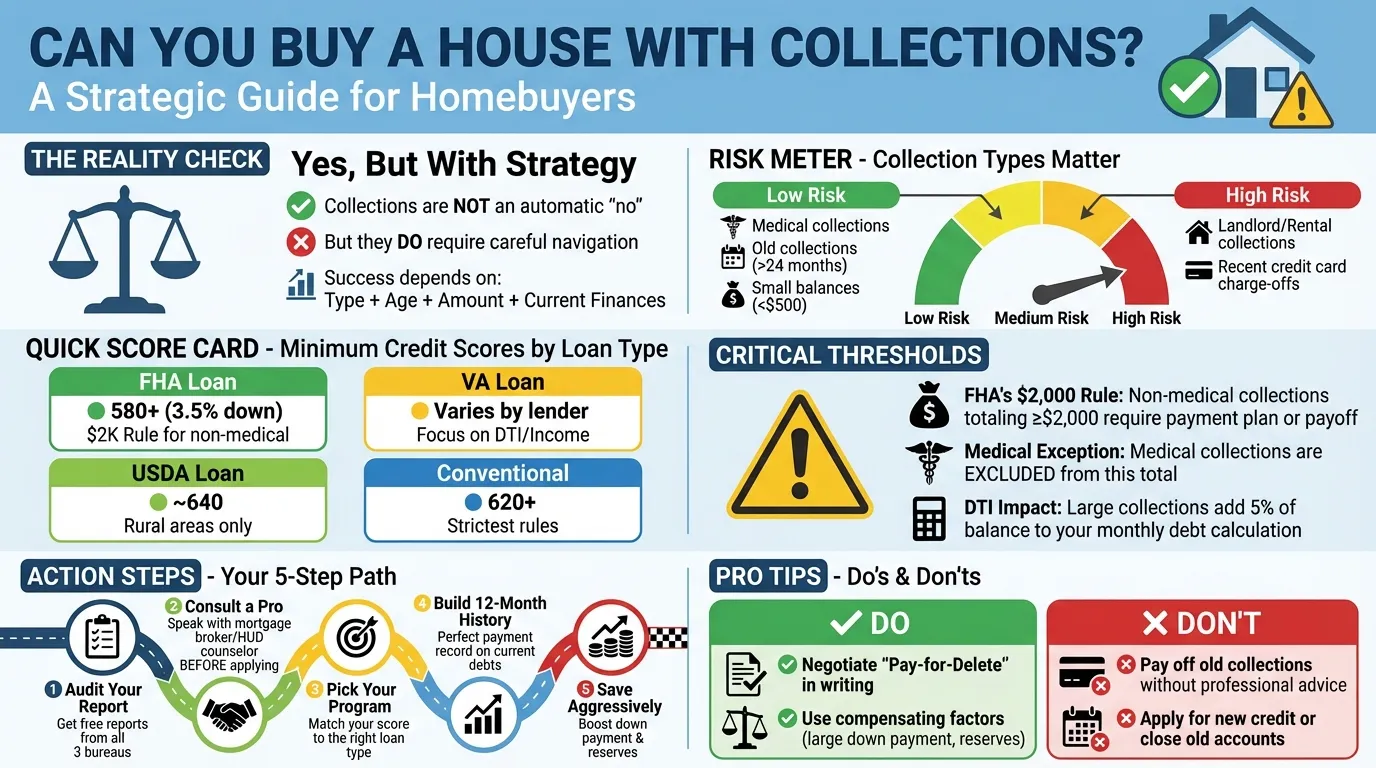

Credit Score Impact: Collections can significantly lower your FICO score, which affects your interest rate and loan eligibility. Scores below 620 typically limit you to government-backed loans (FHA, VA, USDA), while scores above 680 open doors to conventional financing with better rates.

-

Debt-to-Income (DTI) Ratio: This compares your monthly gross income to your monthly debt obligations.

-

Front-End Ratio: Measures housing costs (PITI) against income, ideally at or below 28%.

-

Back-End Ratio: Measures all monthly debt (housing, auto loans, credit cards, etc.) against income, with a general target of 36%-43%.

-

How Collections Impact Your Credit Score

Collections are considered a negative item on your credit report. They show lenders that, at some point, you didn’t pay a debt as agreed.

- When they’re new: Collections hurt the most. A fresh collection can drop your score by 50–100 points.

- Over time: The impact fades. After 1–2 years, the “sting” of that collection is smaller.

- After 7 years: Most collections fall off your report entirely, whether you pay them or not.

Important: Paying an old collection doesn’t remove it; it just updates the balance to zero. The record of the account stays until it ages off, which is why understanding the right credit repair strategy for homebuyers matters more than just paying everything in sight.

Mortgage Options for Borrowers with Collections

Different loan programs have varying levels of leniency toward credit blemishes.

1. FHA Loans

FHA loans are often the most accessible path for those wondering, “Can I buy a house with collections?” because they are designed for borrowers with lower credit scores and limited down payments. FHA is more flexible. Collections don’t always have to be paid off before closing.

However, if your total collections add up to more than $2,000, the lender may require:

- Verify that the debt is paid in full at the time of or prior to settlement using an acceptable source of funds;

- Verify that the Borrower has made payment arrangements with the creditor and include the monthly payment in the Borrower’s Debt-to-Income ratio (DTI); or

- If a payment arrangement is not available, calculate the monthly payment using 5 percent of the outstanding balance of each collection and include the monthly payment in the Borrower’s DTI.

For more information, refer to this link.

2. VA Loans

For veterans and active service members, VA loans offer significant flexibility. There is often no set minimum credit score or policy regarding collections; instead, lenders focus on your overall debt-to-income ratio and residual income. Small or aged collections are frequently overlooked if your current finances are stable.

3. USDA Loans

Similar to FHA guidelines, USDA loans for rural properties are generally lenient. They may approve applications with collections if the borrower provides a valid explanation and meets strict income and property location requirements.

4. Conventional Loans (Fannie Mae/Freddie Mac)

Conventional loans are typically the strictest. Not all negative accounts are handled the same way during underwriting, and the rules depend heavily on the property type.

- First, accounts that are past due but not yet in collections must be brought current before closing. There’s no flexibility here, late accounts are a red flag lenders won’t ignore.

- Medical collections are treated differently. They are excluded from the payoff limits and generally do not need to be paid off before or at closing.

- For one-unit primary residences, borrowers are usually not required to pay off outstanding collections, regardless of the balance. However, there’s an important caveat: if the lender marks a collection as “Paid by Close” in the loan application, the automated underwriting system (DU) will require proof that the debt is paid.

- For two- to four-unit owner-occupied properties and second homes, the rules tighten. If your total collections and non-mortgage charge-offs exceed $5,000, they must be paid in full prior to or at closing.

- For investment properties, underwriting is the strictest. Any individual collection or non-mortgage charge-off of $250 or more, or total accounts exceeding $1,000, must be paid in full before or at closing.

Advanced Strategies to Improve Your Approval Odds

1. The Strategic “Pay for Delete” Negotiation

When dealing with collection agencies, you can request a “Pay-for-Delete” agreement-a written promise to remove the negative mark from your credit report in exchange for payment (often for a settled amount less than the full balance). This can improve your credit score, but get the agreement in writing before paying.

2. Beware of “Re-Aging” and Timing Your Payments

A major risk when paying off old collections is inadvertently lowering your score. Paying an old debt updates the “Date of Last Activity,” making it appear recent to scoring models, which can cause a temporary score drop. If you have old collections and are within 3-6 months of applying for a mortgage, consult a loan officer or credit counselor before making any payments. Sometimes, it’s better to leave them untouched until after closing.

That’s why strategy is everything. At Mortgage Ready Program, we help you decide which collections to leave alone, which to settle, and when to make payments so they help instead of hurt.

3. Utilize Compensating Factors

A strong “compensating factor” can persuade an underwriter to approve a file with collections.

-

Large Down Payment: 10%-20% or more shows a serious commitment and reduces the lender’s risk.

-

Substantial Reserves: Having 6+ months of mortgage payments in savings after closing demonstrates financial stability.

-

Low Loan-to-Value (LTV) Ratio: A larger down payment creates a lower LTV, which is favorable.

-

Strong Rental History: Providing 12-24 months of on-time rent payments can offset a prior landlord collection.

4. Dispute Inaccuracies and Validate Debts

You have the right to:

-

Dispute Inaccurate Information: If a collection is not yours, is past the 7-year reporting period, or has an incorrect balance, file a dispute with the credit bureaus.

-

Request Debt Validation: Within 30 days of first contact, you can ask the collection agency to provide proof you owe the debt. If they cannot, they must remove it.

Why the Type and Age of Collections Matter Immensely

Lenders assess the risk level of collections differently:

-

High-Risk Collections: Landlord/rental collections are major red flags, as they directly question your ability to handle housing payments. Recent credit card charge-offs also signal ongoing financial distress.

-

Lower-Risk Collections: Older collections (over 24 months) and small balances (under $500) are often ignored by automated underwriting systems, especially for FHA and VA loans. Medical collections, as noted, are also lower risk.

The Path Forward: Expert Advice for the “Collections-Burdened” Buyer

Financial experts emphasize that if you cannot qualify for a mortgage due to collections, it may be a signal to focus on preparation. Homeownership brings unexpected costs, maintenance, repairs, tax increases, that can strain a budget already dealing with old debt. Consider these steps:

-

Get Pre-Reviewed: Speak with a professional mortgage specialist. They can give you a realistic roadmap.

-

Build a Solid 12-Month History: Focus on making all current payments (rent, utilities, auto loans) perfectly on time for at least a year. This shows reformed financial behavior.

-

Save Aggressively: Boost your savings for a larger down payment and significant reserves.

Conclusion

Ultimately, if you want to buy a house with collections, you need to know it is not a dead end. It’s a hurdle that can be cleared with the right plan and a solid understanding of how lenders evaluate risk. By prioritizing high-balance or recent collections, choosing the right loan program (often FHA-friendly), and clearly documenting your return to financial stability, you shift the focus from past mistakes to present readiness. The process requires patience, discipline, and smart guidance, but for many buyers, homeownership is absolutely within reach.

If you’re unsure where you stand or want a clear roadmap forward, sign up today and start with our Mortgage Ready Program, designed to help you move from credit uncertainty to homeownership.

0 Comments