Table of Contents

Is it Worth Closing Old Credit Cards?

Closing old credit cards sounds like a smart move, but most of the time, it’s not. Especially if you’re planning to apply for a mortgage soon. Credit scores don’t work the way many people think they do, and shutting down old accounts can actually hurt you. When you close a card, you reduce your available credit and shorten your credit history. Both of these can lower your score. The small benefits, like cleaning things up or avoiding a fee, usually don’t outweigh the damage.

The only time closing a card might make sense is when it has a high annual fee, and you’re not using it at all, or if you know you tend to overspend. Even then, there’s often a better option, like downgrading the card instead of closing it. If your goal is mortgage approval, keeping old accounts open is usually the safer move.

For a comprehensive approach to managing your credit profile before a major loan, consider exploring our dedicated mortgage readiness program.

Does Closing a Credit Card Affect a Mortgage?

Absolutely. Closing a credit card can directly and negatively affect your mortgage application by triggering a drop in your credit score. Mortgage lenders use credit scores as a primary factor in determining your interest rate and loan approval. A lower score can mean higher monthly payments or even disqualification.

The effect is twofold: it raises your credit utilization ratio and can reduce the average age of your accounts. Both are key metrics in FICO scoring. Lenders interpret a rising utilization rate as increased financial risk, which is the last signal you want to send when applying for a home loan. Stability is paramount; any recent account closures can be a red flag to underwriters reviewing your tri-merge credit report.

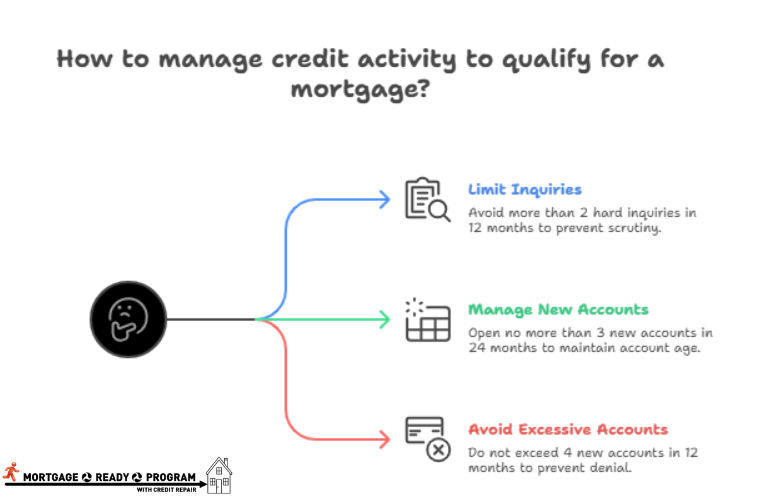

What is the 2/3/4 Rule for Credit Cards?

The 2/3/4 rule is a crucial mortgage lending guideline that assesses your risk based on recent credit activity. It helps underwriters determine if you’ve been seeking too much new credit, which could indicate financial stress and affect your ability to repay a mortgage.

| Rule Component | Description | Impact on Mortgage Qualification |

|---|---|---|

| 2 Inquiries | More than 2 hard inquiries on your credit report within the last 12 months. | May trigger scrutiny, suggesting you are actively seeking credit and potentially increasing your risk profile. |

| 3 New Accounts | Opening more than 3 new credit accounts within the last 24 months. | Can lower your average account age and indicate frequent borrowing, potentially leading to stricter underwriting or higher rates. |

| 4 New Accounts | Some lender variations disallow more than 4 new accounts in the last 12 months. | Viewed as aggressive credit-seeking behavior, which can be a direct cause for mortgage application denial. |

This rule underscores why closing old credit cards should be avoided. Closing an account doesn’t help you comply with this rule; it only removes a positive tradeline. Instead, focus on maintaining a clean, stable report. For targeted strategies on optimizing your credit within these guidelines, visit our resource on how to improve credit for a mortgage.

Will Closing an Old Credit Card Hurt My Credit?

Yes, closing an old credit card will likely hurt your credit score in the short to medium term. The damage primarily comes from two of the five major FICO score factors: Credit Utilization (30% of your score) and Length of Credit History (15% of your score).

| FICO Score Factor | How Closing an Old Card Hurts It | Potential Score Impact |

|---|---|---|

| Credit Utilization (30%) | Reduces your total available credit, causing your utilization percentage to spike if you carry any other balances. | High Impact. A utilization jump from 10% to 30%+ can drop a score 50+ points. |

| Length of Credit History (15%) | If it’s your oldest account, it reduces your Average Age of Accounts (AAoA). Closed accounts stop aging and eventually fall off your report. | Moderate to High Impact, especially for those with a thin credit file (<5 years history). |

| Credit Mix (10%) | Reduces the diversity of your revolving credit accounts. | Low Impact, unless it’s your only revolving account. |

This tangible harm to your credit score is why closing cards is discouraged during mortgage preparation. A lower score directly correlates to less favorable loan terms.

The Primary Danger: Credit Utilization Rate (CUR)

The most immediate consequence of closing old credit cards that people face is a worsened Credit Utilization Ratio (CUR). This ratio, calculated by dividing your total credit card balances by your total credit limits, is a supreme factor in your score.

Real-World Utilization Example

| Scenario | Total Credit Limit | Total Balance | Utilization Rate | Credit Score Implication |

|---|---|---|---|---|

| Before Closure: (2 Cards Open) | $10,000 | $3,000 | 30% (Good) | Score remains stable or improves slightly as balances are paid. |

| After Closure: (Close 1 card with $6,000 limit) | $4,000 | $3,000 | 75% (Poor) | Score can drop significantly, potentially jeopardizing mortgage approval. |

Preserving Your Credit History Length

Your credit history length is a testament to your long-term financial reliability. Closing your oldest card can prematurely remove a decade or more of positive history from your active profile. This makes you appear less experienced to automated scoring models and human underwriters alike. According to a report by FICO in 2019, most people with an 850 score have oldest accounts around 30 years old on average.

The Mortgage Lender’s Perspective: DTI and Risk Avoidance

Lenders seek borrowers who present minimal risk. From their viewpoint, closing a credit card before a mortgage application is an unnecessary and puzzling action that introduces volatility. It doesn’t improve your Debt-to-Income (DTI) ratio (the key metric for payment affordability) since a $0 balance card has a $0 minimum payment. It only harms the credit score they use to price your loan.

When Closing a Card Might Be Considered (and the Better Alternatives)

There are limited, justifiable reasons to close a card, such as exorbitant annual fees on an unused card or to eliminate the temptation of overspending. However, the smarter path is always to first explore alternatives that preserve your credit line and history.

| Alternative Strategy | How to Execute It | Benefit for Mortgage Readiness |

|---|---|---|

| Product Downgrade | Call the issuer and request to change your card to a no-annual-fee version within the same family. | Keeps account age, credit limit, and history intact while eliminating cost. |

| Negotiate a Retention Offer | Ask if the issuer can waive the annual fee for a year or offer bonus points to keep the account open. | Maintains credit profile stability while addressing the financial concern. |

| Manage for Activity | Make a small charge every 3-6 months and pay it off immediately to prevent inactivity closure. | Ensures the issuer doesn’t close the account, preserving your utilization buffer. |

The Mortgage Preparation Timeline and Checklist

Optimizing your credit for a mortgage is a marathon, not a sprint. Begin this process 6-12 months before you plan to apply. Use the following checklist to guide your actions:

| Timeline | Critical Actions (DO) | Actions to Avoid (DON’T) |

|---|---|---|

| 6+ Months Out | Check all 3 credit reports. Dispute errors. Pay down balances to <10% utilization. | Open new credit cards. Take out personal or auto loans. |

| 3-6 Months Out | Continue on-time payments. Let aging accounts mature. Get pre-approved. | Close any credit accounts, especially old ones. Miss any payments. |

| 0-3 Months Out | Maintain status quo. Keep utilization low. Gather financial documents. | Make large purchases on credit. Apply for new credit of any kind. |

Conclusion

Closing old credit cards while getting ready for a mortgage usually does more harm than good. If you ask me, the answer is simple: don’t close anything until after you close on the house. Credit experts, lenders, and mortgage underwriters all say the same thing: Leave your old cards alone before applying.

Before applying for a mortgage, your credit profile needs to stay stable. Think of it like a structure that’s already standing. Once the mortgage is closed and you’re settled into your new home, then you can clean things up if you want.

If you want to make sure you’re doing all the right things before applying, our Mortgage Ready Program is built to guide you step by step. Sign up and know exactly where you stand before lenders start looking.

0 Comments