Are you tired of paying for rent every month? Let’s discuss what it takes to buy a house!

Moving from renting to owning your own home is an exciting step and a big one. However, first of all, you need to know if you qualify for a mortgage!

Lenders typically look at three items before they approve your application: Credit, Assets, and, most importantly, Income. When it comes to income, your debt-to-income ratio (DTI) is so important.

If you want to know what DTI is and how it relates to your mortgage application, you have come to the right place. In this article, we’ll break it down in plain language so you’ll know exactly how DTI plays into the mortgage process and what you can do to improve it.

Let’s get into it.

Table of Contents

What is the Debt-to-Income Ratio for Mortgages?

The debt-to-income ratio (DTI) is a percentage that compares your total monthly debt payments to your gross monthly income. Lenders use this ratio to assess how much of your income is already committed to repaying debt and to gauge your ability to handle additional debt in the form of a mortgage.

The formula for calculating DTI is straightforward:

In this formula:

- Total Monthly Debt Payments include all of your recurring monthly obligations, such as credit card payments, student loans, car loans, and your future mortgage payment.

- Gross Monthly Income is the total income you earn before taxes and deductions.

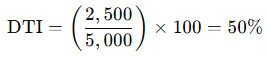

For example, if your monthly debts total $2,500, and your gross income is $5,000, your DTI would be:

This means that 50% of your income is going toward paying off debts, and the remaining 50% is available for living expenses, savings, and other financial obligations.

Types of Debt-to-Income Ratios

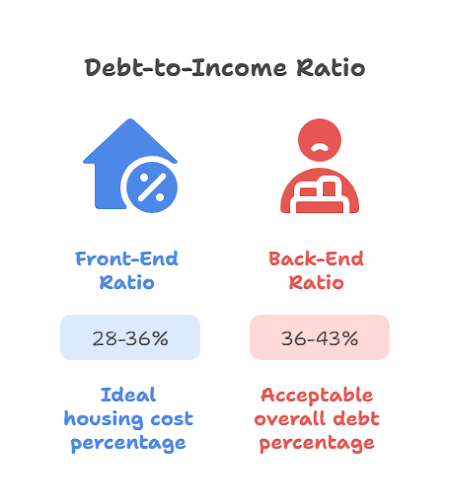

Lenders typically evaluate two types of debt-to-income ratios for mortgages when assessing a borrower’s financial health: the front-end ratio and the back-end ratio. Both ratios are important, but they focus on different aspects of your debt load.

1. Front-End Ratio

The front-end ratio, also known as the housing ratio, measures the portion of your income that goes toward housing costs if you were approved for your mortgage. These include:

- Your monthly mortgage payment (principal and interest)

- Property taxes

- Homeowners insurance

- Homeowners Association (HOA) fees (if applicable)

In most cases, lenders want the front-end ratio to be no more than 28-36% of your gross monthly income. A lower front-end ratio is ideal because it indicates that you are not overburdened by housing costs.

2. Back-End Ratio

The back-end ratio includes all of your monthly debt payments, not just housing costs. This means that in addition to your mortgage payment, you would also include:

- Credit card payments

- Car loans

- Student loans

- Personal loans

- Alimony or child support (if applicable)

Lenders typically look at the back-end ratio to assess your overall ability to manage debt. For most loan types, a back-end ratio of 36-43% is acceptable, but this can vary depending on the lender and the type of mortgage.

What is a Good Debt-to-Income Ratio for Mortgages?

When applying for a mortgage, including specialized loans like the FHA 203(k) loan, your Debt-to-Income (DTI) ratio plays a significant role in determining your eligibility and the terms of your loan. Ideally, your front-end DTI should not exceed 28% of your gross monthly income. This ensures that your housing expenses are manageable in relation to your overall financial picture.

For the back-end DTI, it’s best to keep this ratio at or below 36%. This demonstrates to lenders that you have enough room in your budget to cover both your ongoing obligations and your living expenses without stretching your finances too thin.

While these are ideal ranges, it’s important to note that certain loan types, such as an FHA 203(k) loan, have more lenient DTI requirements. An FHA loan is a government-backed mortgage option designed to help first-time homebuyers or those with less-than-perfect credit secure home financing. For FHA loans, including 203(k) loans, the back-end DTI ratio can be higher than 36%, often up to 43% or even higher in some cases, especially if you have strong compensating factors like a larger down payment or stable income.

If your DTI ratio exceeds 36%, you might still qualify for a mortgage, but you may not receive the best interest rates or loan terms. In such cases, you may want to explore FHA 203(k) loans, which offer higher DTI thresholds and can provide more flexibility, particularly for buyers looking to purchase and renovate a home in one loan.

Debt-to-Income Ratio Requirements by Loan Type

Different mortgage programs have different requirements for DTI ratios. While all lenders aim to ensure you can afford a mortgage, some programs are more lenient than others. Let’s take a look at the DTI requirements for several popular loan types.

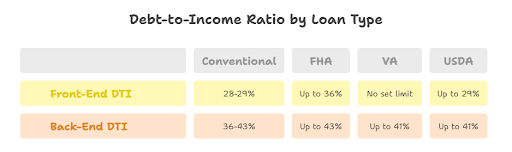

1. Conventional Loans

Conventional loans, which are not backed by the government, typically require a front-end ratio of 28-29% and a back-end ratio of 36-43%. However, these ratios can be more flexible for borrowers with excellent credit scores, a substantial down payment, and low debt levels.

For example, a borrower with a strong credit score (over 740) may be able to secure a conventional loan even with a back-end DTI ratio approaching 45%, but they will likely face higher interest rates due to the increased risk.

2. FHA Loans

The Federal Housing Administration (FHA) offers loans designed for borrowers who may not meet the stricter requirements of conventional loans. FHA loans typically allow for higher DTI ratios.

- Front-End DTI: Up to 36%

- Back-End DTI: Up to 43%

This makes FHA loans a good option for first-time homebuyers or borrowers with less-than-perfect credit. However, it’s important to note that FHA loans come with an upfront mortgage insurance premium (UFMIP) and ongoing mortgage insurance premiums (MIP) that can affect your monthly payment.

3. VA Loans

VA loans are backed by the U.S. Department of Veterans Affairs and are available to eligible veterans, active-duty service members, and certain members of the National Guard and Reserves. These loans typically do not have strict DTI requirements.

- Front-End DTI: No set limit

- Back-End DTI: Up to 41%

Because the VA guarantees a portion of the loan, lenders are more willing to offer flexible terms, including higher DTI ratios.

4. USDA Loans

The U.S. Department of Agriculture (USDA) offers loans to low- to moderate-income borrowers in rural areas. USDA loans allow for a DTI ratio of:

- Front-End DTI: Up to 29%

- Back-End DTI: Up to 41%

While USDA loans offer favorable terms for borrowers in eligible rural areas, they do have specific income and property eligibility requirements that must be met.

How to Calculate Your Debt-to-Income Ratio

Now that you understand the different types of DTI ratios, let’s walk through how you can calculate your own DTI.

Step 1: List All Monthly Debt Payments

You need to list all of your recurring monthly debt payments. This includes:

- Housing costs (rent or mortgage payments, property taxes, homeowners’ insurance)

- Credit card payments (minimum monthly payment)

- Student loans

- Car loans

- Personal loans

- Alimony or child support payments (if applicable)

Step 2: Determine Your Gross Monthly Income

Your gross monthly income is the amount you earn before any taxes or deductions. This can include:

- Salary or wages (before tax)

- Bonuses

- Overtime pay

- Commissions

- Rental income (if applicable)

- Investment income (if applicable)

Step 3: Calculate Your DTI

Once you have your total monthly debts and your gross monthly income, you can use the DTI formula to calculate your ratio:

For example, if your total monthly debts are $2,500 and your gross monthly income is $5,000, your DTI would be 50%.

This means that 50% of your income is going toward paying off debts.

How to Lower Your Debt-to-Income Ratio

A high DTI ratio can make it more challenging to secure a mortgage. Here are some steps you can take to reduce your DTI ratio and improve your mortgage prospects.

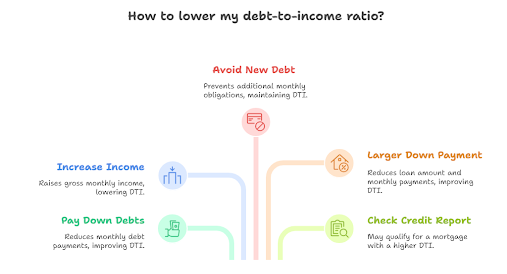

1. Pay Down Existing Debts

One of the most effective ways to lower your DTI ratio is to pay down your existing debts. Focus on high-interest debts, such as credit card balances, first. Paying down these debts reduces your total monthly debt payments and improves your DTI.

2. Increase Your Income

Another way to lower your DTI ratio is by increasing your income. This could involve:

- Asking for a raise at work

- Taking on a part-time job

- Starting a side hustle

Increasing your income will raise your gross monthly income, which in turn lowers your DTI ratio.

3. Avoid Taking on New Debt

Before applying for a mortgage, try to avoid taking on new debt. Each new loan, credit card balance, or personal loan increases your monthly debt obligations and raises your DTI ratio.

4. Consider a Larger Down Payment

A larger down payment reduces the overall loan amount, which can help reduce your monthly mortgage payment. A lower monthly mortgage payment will improve your front-end DTI ratio and make it easier to qualify for a mortgage.

5. Check Your Credit Report

Reviewing and cleaning up your credit report can also help you lower your DTI. A better credit score may allow you to qualify for a mortgage with a higher DTI ratio, as lenders may be more flexible with your financial situation. You can learn how to clean up your credit report by reading this helpful article on how to clean up your credit report.

Conclusion

Understanding and managing your debt-to-income ratio for mortgages is crucial when applying for a mortgage. By calculating your DTI, knowing the requirements for different loan types, and taking steps to lower your ratio, you can improve your chances of securing favorable loan terms. With the right approach, you can move forward on your path to homeownership with confidence.

Ready to take the next step toward homeownership? The Mortgage Ready Program can help you get prepared and improve your chances of securing a mortgage. Get started today on your journey to owning a home!

FAQs

Does my credit score affect my DTI ratio?

No, your credit score does not directly affect your DTI ratio. However, a higher credit score can make lenders more flexible with DTI requirements, making it easier for you to qualify for a mortgage.

Is rent included in the DTI calculation?

Yes, if you’re renting, your monthly rent payment is included in the DTI calculation. Rent is considered a housing expense, just like a mortgage payment.

Can I qualify for a mortgage with a high DTI ratio?

It depends on the type of loan you’re applying for and the lender’s specific policies. Government-backed loans, such as FHA, VA, and USDA loans, tend to be more lenient with higher DTI ratios, especially if you have other compensating factors, like a large down payment or strong credit score.

How can I improve my DTI ratio?

You can improve your DTI ratio by paying down debt, increasing your income, avoiding new debt, and making a larger down payment when applying for a mortgage.

What is considered a good DTI ratio for a mortgage?

A good DTI ratio for a mortgage is typically below 36%, though some lenders may allow higher ratios for certain loan types or with compensating factors.

Does a 401(k) loan affect my debt-to-income (DTI) ratio?

No, a 401(k) loan does not affect your DTI ratio. When you take a loan from your 401(k), it is considered a loan to yourself, meaning it is not counted as traditional debt by most lenders. As a result, your DTI ratio remains unaffected, and it won’t impact your ability to qualify for a mortgage.

0 Comments