The fastest way to boost your credit score for mortgage applications is a primary concern for many prospective homebuyers, as your credit score is the single most influential factor in determining the interest rate you receive. While building a truly robust credit history is often described as a “marathon, not a race,” there are specific, high-impact actions you can take to see significant movement in your score within a few weeks to months.

This guide outlines the strategic, rapid interventions that can elevate your score in the critical window before you apply. Let’s get started!

Table of Contents

Master Your Credit Utilization: The 30% Solution

Credit utilization, which is the percentage of your available credit you’re using, is a pivotal factor, accounting for 30% of your FICO score. It’s also one of the fastest factors to adjust.

-

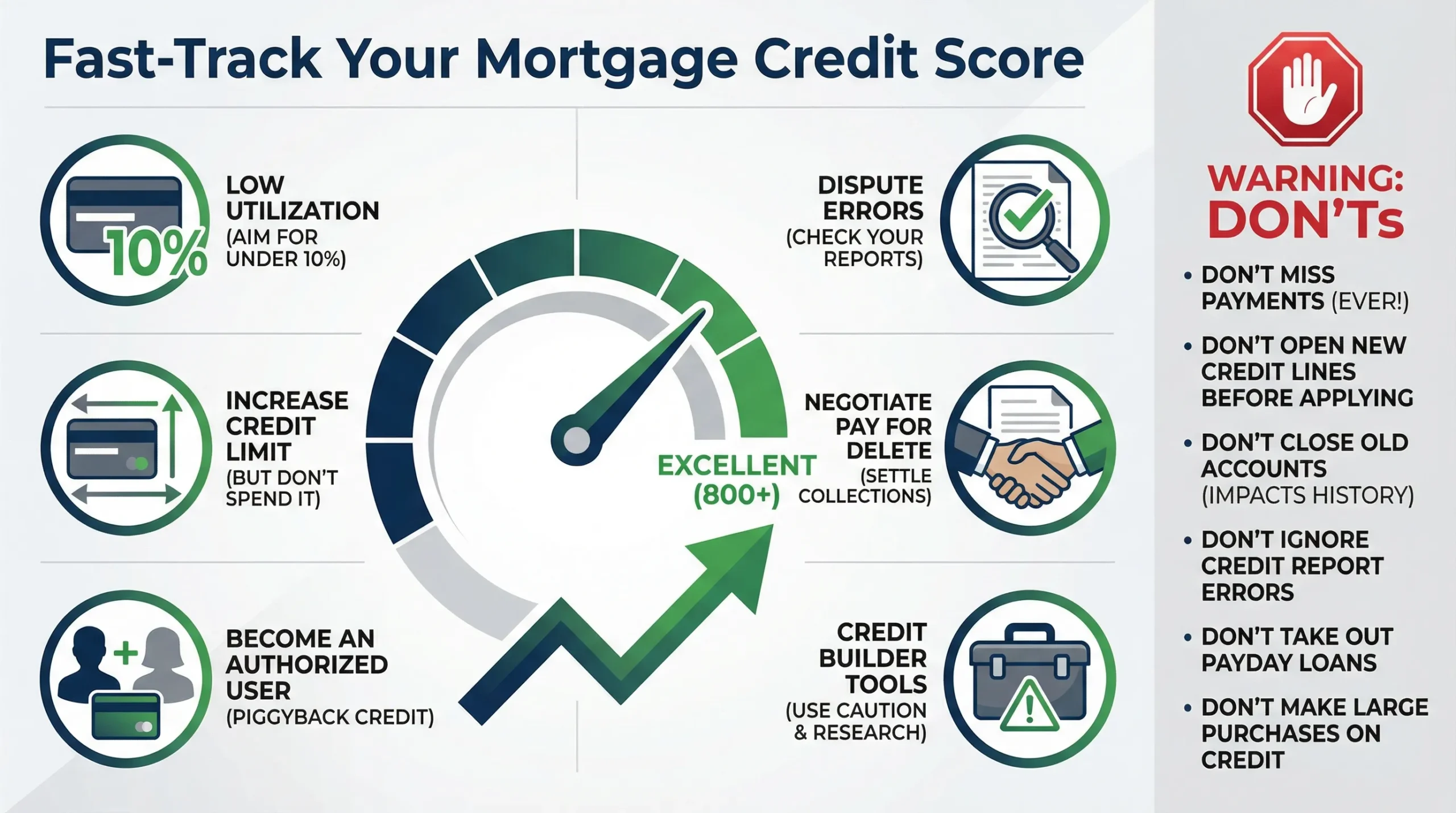

Aim for the Single Digits: The common advice is to stay below 30% utilization. However, for a rapid boost aiming for the best mortgage rates, target below 10%, and ideally below 7%, on each card and in total.

-

Strategic Payment Timing: Don’t wait for the statement. Pay down balances before your card issuer’s billing cycle closes and reports to the credit bureaus. This ensures a low balance is recorded.

-

The AZEO Method: “All Zero Except One” is a powerful short-term tactic. Pay every credit card balance to $0, except for one card. On that single card, allow a tiny balance (e.g., 1% of the limit) to report. This can maximize your score 30-45 days before your mortgage application by showing active, responsible use without high utilization.

Rapidly Increase Your Available Credit

Lowering your utilization can be done by increasing your credit limits, effectively giving you more breathing room.

-

Request Credit Limit Increases: Contact your card issuers, especially if your income has increased or you have a long history of on-time payments. Crucially, ask if this will be a “soft” or “hard” inquiry. A soft pull won’t hurt your score; a hard inquiry can cause a minor, temporary dip.

-

Never Close Old Cards: Closing an unused card reduces your total available credit, which can instantly spike your overall utilization ratio and shorten your credit history length, both harmful to your score.

The Power of Becoming an Authorized User

If you have a “thin” file or need a quick infusion of positive history, this is a highly effective strategy.

-

Borrow Positive History: By becoming an authorized user on the account of a trusted person (like a family member) with a long history of perfect payments and a high credit limit, that account’s positive history can be added to your report.

-

No Risk to the Primary User: You don’t need a card or account access. The primary user maintains full control. Ensure the card issuer reports authorized user data to all three credit bureaus for maximum impact.

Scrub Your Credit Reports for Errors

Federal Trade Commission (FTC) studies have found that around 20% of people have errors on at least one of their credit reports, meaning roughly one out of every five consumers sees inaccurate information.

-

Get Your Credit Reports: Set up your credit monitoring using Smart Credit.

-

Dispute Inaccuracies Aggressively: Look for accounts that aren’t yours, late payments you made on time, balances incorrectly reported, or old negative items (over 7 years) that should have been removed. File disputes directly with each bureau online; by law, they must investigate within 30-45 days. A successful removal can lead to an immediate score jump.

Strategically Handle Collections and Delinquencies

If you are considering the fastest way to boost your credit score for mortgage success, you need to know that payment history (35% of your score) is the hardest to fix quickly, but strategic action can help.

-

Goodwill Letters for Isolated Lates: For a single late payment on an otherwise perfect account, a polite “goodwill letter” to the creditor asking for forgiveness can sometimes result in its removal.

-

The “Pay-for-Delete” Negotiation: For collection accounts, you can negotiate with the collector. Offer to pay the debt in full or settle for less in exchange for them deleting the collection entry entirely from your credit report. Get any agreement in writing before you pay. Note: This is not always possible, as not all agencies agree to it.

-

Understand Mortgage Underwriting: Even if a paid collection doesn’t dramatically boost your score under some models, mortgage underwriters will view a satisfied collection more favorably than an open, unpaid one.

Utilize Modern Credit-Boosting Tools (With Caution)

New services allow you to add non-traditional payment data.

-

Rent and Utility Reporting: Services like Experian Boost can add positive utility, phone, and streaming service payments. Separate rent-reporting services (e.g., Rental Kharma, PayYourRent) can add your rental history.

-

The Major Caveat: Most mortgage lenders use older, specialized FICO scores (FICO 2, 4, 5) that do not incorporate this “boosted” data. Use these tools as a potential supplement, but never as your primary strategy. The core tactics above are what mortgage lenders will see.

The Mortgage Application “Danger Zone”: What to Avoid

In the 3-6 months before applying, protect your score vigilantly.

-

No New Credit Applications: Every hard inquiry from applying for a new credit card or loan can lower your score. Let your credit profile sit undisturbed.

-

Avoid Overdrafts: Consistent use of an arranged overdraft can be a red flag to mortgage lenders, suggesting you live beyond your means.

-

Audit Your Bank Statements: Lenders will scrutinize 3-6 months of statements. Avoid large, unexplained cash deposits, frequent gambling transactions, or payday loan usage, as these can lead to application denial regardless of your credit score.

MortgageReady Program to the Rescue

The fastest way to boost your credit score for mortgage success hinges on a focused, aggressive, and strategic approach to the factors you can control quickly: utilization, errors, and strategic credit file additions.

Credit repair is a complicated and sensitive process; one small mistake can seriously damage your credit. This article was only a brief educational overview, and if you’re new to this, it can still feel overwhelming, right? That’s exactly why we created the MortgageReady Program. Our team specializes in credit improvement and homeownership solutions, and we can help you become a homeowner, even if you have bad credit.

Sign up today to start your journey. And if you’d like to learn more, check out our Credit Repair Guide.

0 Comments