Closing on a home is one of the most exciting milestones of your life, but it’s also one of the most fragile. From the time your mortgage is conditionally approved until you sign closing documents, your financial stability is under a microscope.

Many buyers don’t realize that lenders perform last-minute credit checks, income verifications, and account reviews right before closing. That means any change to your financial profile, even something that feels minor, can jeopardize your mortgage approval. Given that, according to Redfin, 1 in 7 deals fall apart before closing, lenders scrutinize any last-minute changes closely.

Below, we explain the 20 most common mortgage closing mistakes in detail, so you know exactly what to avoid in the critical weeks leading up to closing.

Table of Contents

Why Do Lenders Re-Check Before Closing?

Mortgage lenders have one main priority: ensuring you can make your monthly payments. They verify this by analyzing your:

- Credit score (your track record of managing debt).

- Debt-to-income ratio (DTI) (your existing debt obligations vs. income).

- Employment status (your stability and reliability).

- Bank account balances (proof you can afford the down payment + closing).

Since weeks or months may pass between approval and closing, lenders do a final financial sweep. They want to see consistency, not new risks. Proactively improving your credit for a mortgage before closing helps reduce the risk of last-minute denials or delays.

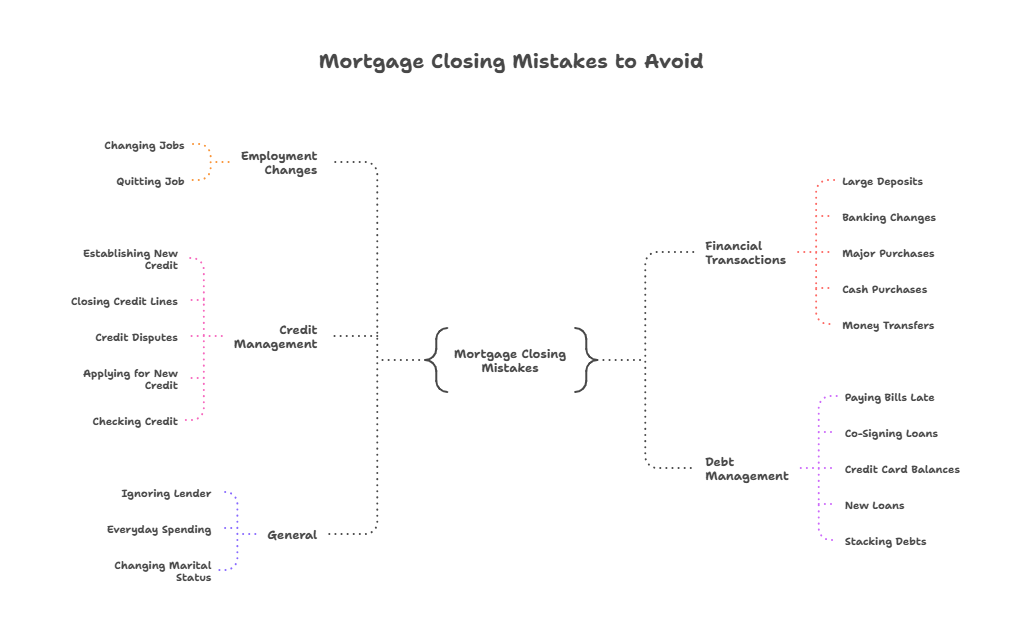

The 20 Biggest Mortgage Closing Mistakes to Avoid

1. Changing Jobs Too Close to Closing

Switching employers right before closing can seem harmless, especially if the new job pays more. But lenders value stability over change, and any employment shift can trigger new verification requirements. If your new role is commission-based or self-employed, the lender may not count that income at all, since they typically want two years of documented history. Even moving within the same field can be flagged as instability. To avoid this, try to remain in your current role until after the loan closes, or discuss the timing with your loan officer before making any moves.

2. Making a Large Deposit Without Documentation

A big deposit, like cash savings or money from a family member, is one of the biggest mortgage closing mistakes. Lenders are required to ensure funds are “sourced and seasoned,” meaning they come from a legitimate, trackable origin and have been in your account long enough to be considered stable. If you can’t explain where the deposit came from, the lender may assume it’s a hidden loan, which changes your debt profile. Always keep records such as pay stubs, bank transfer slips, or gift letters to verify deposits.

3. Paying Bills Late

Even a single late payment on a credit card, auto loan, or utility bill can seriously damage your mortgage approval. Late payments are quickly reported to credit bureaus and can lower your score by 50 points or more. That dip could push you below your lender’s credit threshold or bump you into a higher interest bracket. Beyond the numbers, a late payment makes you appear financially disorganized. Protect yourself by setting up auto-pay or reminders for every account until after your loan funds.

4. Establishing New Credit

Opening a new credit card, financing a store purchase, or applying for a personal loan before closing is one of the most common and costly mortgage closing mistakes. Every application creates a hard inquiry that can lower your score. A new account also reduces the average age of your credit history, another scoring factor. To underwriters, it signals you’re taking on new obligations right before one of the biggest commitments of your life. Hold off on all new credit until after closing.

5. Quitting Your Job

Quitting your job before closing almost guarantees your mortgage will be denied. Your lender has approved you based on proof of income from your current employer. Without a verifiable paycheck, your entire application collapses. Even if you plan to start a new job later, the absence of income documentation at the time of closing is a red flag. Simply put: no job means no loan. Wait until your mortgage has funded to make career changes.

6. Making Major Banking Changes

Switching banks or moving money between accounts may seem harmless, but to an underwriter, it creates unnecessary complexity. Lenders need to see a clean, traceable path for your down payment and reserves. If you suddenly move funds into a new bank, they’ll request statements from both the old and new institutions, which can delay the process. Keep your accounts steady, avoid unnecessary transfers, and don’t open new banking relationships until you’re settled in your new home.

7. Closing Lines of Credit

Closing old credit cards or unused accounts may feel like good housekeeping, but it can hurt your mortgage approval. Closing a card lowers your available credit, raising your utilization ratio, the percentage of credit you’re using compared to your limit. It also shortens your average account age, another key factor in credit scoring. Together, these changes can reduce your score enough to affect your loan. Leave accounts open until your mortgage is finalized.

8. Co-Signing a Loan

Agreeing to co-sign for a friend or family member’s loan adds their debt to your financial profile. Even if they make every payment, the obligation shows up on your credit report and counts against your DTI. To lenders, it looks like you’ve taken on new responsibility at the worst possible time. Co-signing during the closing period can jeopardize your approval, so postpone any such commitments until you own your home.

9. Making Large Purchases on Credit

Even if you don’t take out a new loan, charging expensive items on your credit card before closing is risky. Large balances increase your utilization ratio, which can quickly drop your score. Lenders also factor in the minimum payments from new charges when recalculating your DTI. A few thousand dollars on a card could be enough to cause a denial. Keep balances low and wait to buy non-essential items until after closing.

10. Making Credit Disputes or Changes

Trying to clean up your credit by disputing errors or closing accounts right before closing can backfire. A dispute can put a tradeline in “pending” status, making it invisible to scoring models. Some lenders refuse to fund loans with active disputes because they can’t evaluate your full credit profile. Similarly, sudden account closures raise questions. Delay credit repairs until after your loan is finalized.

This is why any credit repair for homebuyers should be planned carefully and ideally completed well before the closing phase.

11. Taking Out New Loans

Auto loans, personal loans, or payday advances all count as new debt, which increases your DTI. Even if the payments seem small, underwriters must include them in your file. A new loan just before closing can throw off your ratios and disqualify you. Stay away from all new borrowing until your mortgage closes.

12. Running Up Credit Cards

Your credit utilization is a major scoring factor. Running up balances in the weeks before closing is dangerous because it lowers your score and makes you look financially stretched. Even if you intend to pay the balance off quickly, your statement balance is what lenders see. Keep spending steadily and balance under 30% of your limit.

13. Buying Large Items with Cash

Paying cash for big purchases, such as furniture or electronics, may seem safer than using credit, but it can still hurt your approval. Lenders require you to maintain a certain level of reserve cash available after closing. If you drain your savings for a purchase, you may fall short of that requirement. Keep your cash intact until you’re a homeowner.

14. Changing Marital Status

Marriage, divorce, or separation before closing alters your financial profile. Adding or removing a spouse can change income, debts, and ownership of assets. Lenders may need to re-run your application under new conditions, which delays or even voids the approval. If possible, delay legal changes in marital status until after you close.

15. Ignoring Your Lender

Your lender may ask for updated pay stubs, bank statements, or explanations during underwriting. Ignoring these requests or submitting documents late is a surefire way to stall closing. Underwriters need complete files to approve your loan, and missing paperwork signals disorganization. Respond promptly to all requests to keep your loan on track.

16. Submitting to Extra Credit Checks

Applying for credit elsewhere results in hard inquiries that lower your score. Even a few points can make a difference in your interest rate or approval status. During closing, you should avoid any actions that trigger new inquiries. If a retailer or lender offers you financing, decline until after you close.

17. Moving Money Around

Large withdrawals or frequent transfers between accounts create confusion for underwriters. They need to verify that your down payment and closing funds come from legitimate, stable sources. Moving money around complicates that verification and can delay approval. Keep your funds in place and stable until your loan funds.

18. Forgetting to Check Your Credit

It’s a mistake to assume your credit is safe once you’ve been approved. Errors, collections, or fraud can pop up at any time. If your lender sees negative changes on your report before closing, your loan may be re-evaluated. Monitor your credit through a reputable service and catch issues early, but avoid making drastic changes during closing.

19. Stacking Up Debts

Even small debts can add up. Buy-now-pay-later plans, extra credit charges, or new installment accounts might seem insignificant, but lenders view them collectively. Stacking debts increases your obligations, raises your DTI, and makes you appear financially unstable. The weeks before closing are a time to freeze spending, not add more debt.

20. Being Careless with Everyday Spending

Finally, don’t underestimate how daily spending habits appear to lenders. If your bank statements show erratic withdrawals, overdrafts, or sudden drops in balance, underwriters may see it as financial instability. Even if you technically qualify, such behavior creates doubt. Keep your spending consistent, avoid overdrafts, and maintain healthy balances.

Conclusion: Stability Wins

The most important lesson from the Mortgage Ready Program is this: stability wins. Every one of these mortgage closing mistakes stems from unnecessary change, new debts, new accounts, new jobs, or fluctuating balances. Your lender wants to see a steady, reliable financial picture from the day you apply until the day you close. Keep your money, credit, and employment consistent, respond quickly to your lender, and when in doubt, ask your loan officer before making any move. By avoiding these pitfalls, you’ll walk into closing with confidence and walk out with the keys to your new home.

Are you ready to begin the homeownership process? Sign up today!

0 Comments