Verifiable Income for Mortgages is one of the three main requirements every homebuyer needs to initiate the homebuying process. These key elements are: Income, Assets, and Credit.

Are you ready to learn about a crucial factor in getting a mortgage? Verifiable income plays a significant role in the home-buying process. Lenders want assurance that you can make your monthly payments for the next 15 to 30 years. They achieve this by evaluating your income to ensure it is reliable, consistent, and, most importantly, verifiable.

In this article, we will discuss different types of income and the importance of verifiable income for mortgages. Let’s get started!

Table of Contents

Understanding Income Types

When it comes to a mortgage, your income directly shows a lender whether you can repay the loan. That’s why we always tell our clients that the first thing lenders look at when reviewing your mortgage application is your income.

There are different types of incomes, and in this section, we are going to go over them one by one.

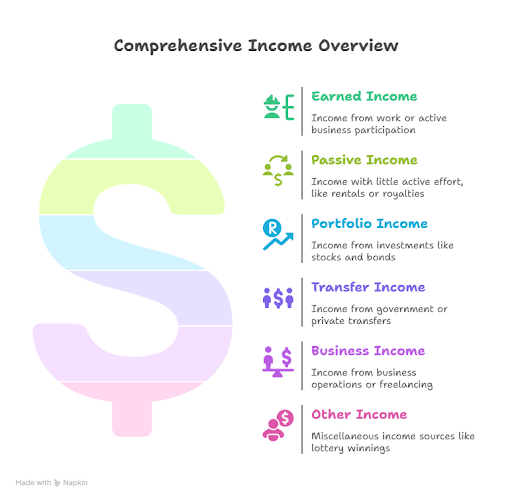

1. Earned Income (Active Income)

Earned income is the most common and easily verifiable income type. This is money you earn through work or active participation in a business. It includes wages, salaries, bonuses, tips, and income from self-employment.

- What is included: Wages, salaries, bonuses, commissions, tips, self-employment income, and income from businesses that you actively manage.

Since earned income is taxed at higher rates than other types of income, it is the easiest for lenders to verify. If you’re employed full-time or part-time, this income is straightforward and provides an immediate picture of your financial situation.

2. Passive Income

Passive income is money you earn with little to no active effort once the income stream is set up. It’s not something that happens through your day-to-day work; instead, it comes from investments, property rentals, royalties, or businesses in which you don’t play an active role.

- What is included: Rental income, royalties from intellectual property, income from limited partnerships, and income from businesses in which you don’t actively participate.

This income type is generally taxed at lower rates than earned income, but it can be harder to verify. Lenders will require proof that your passive income is reliable and consistent over time, especially if it’s used as your main income source for the mortgage application.

3. Portfolio Income

Portfolio income is money you make from investments such as stocks, bonds, and mutual funds. If you’re a savvy investor, you may have a steady flow of dividends, interest, and capital gains that contribute to your overall income.

- What is included: Interest, dividends, capital gains, annuities, and royalties from investments.

Portfolio income is often taxed at favorable rates, especially long-term capital gains. Lenders may want to see a steady history of this type of income to ensure it is a reliable and continuing source.

4. Transfer Income

Transfer income comes from government or private transfers and can include Social Security, unemployment benefits, pensions, alimony, and child support. While this type of income is not earned through active work, it can still be used to qualify for a mortgage if it’s consistent and documented.

- What is included: Social Security benefits, unemployment compensation, pensions, alimony, and child support.

Although transfer income is often not the primary source for mortgage qualification, it can still be used as long as it’s expected to continue for the foreseeable future. However, lenders may not accept this income as a standalone source, especially if the borrower is relying solely on these benefits.

5. Business Income

Business income refers to the profits earned from the operation of a business. This can include income from sales, services, freelancing, or consulting. For self-employed individuals, business income is an important source of income to document for a mortgage application.

- What is included: Revenue from business sales, profits from operations, or freelancing and consulting income.

Business income is subject to self-employment taxes and typically requires a bit more paperwork. If you’re self-employed, you’ll need to provide detailed financial documents, including tax returns and business records.

6. Other Income

This category includes various other types of income, like lottery winnings, gifts, inheritances, and prize money. While not common, these sources can be used to supplement your application if documented properly.

- What is included: Lottery winnings, gifts, inheritances, and prize money.

The taxability of these income sources varies. For example, gifts and inheritances are generally not taxable to the recipient, but in some cases, there may be exceptions.

Lenders review income consistency alongside the steps borrowers take to improve their credit for a mortgage, creating a complete financial profile.

The Importance of Verifiable Income for Mortgages

When it comes to applying for a mortgage, verifiable income for mortgages is essential. Lenders need to confirm that you have a reliable income stream to cover your future mortgage payments. In fact, verifiable income is one of the primary factors lenders look at during the mortgage approval process.

Why is this so important? Because it shows the lender that you can afford the home loan, and you need a steady income to be able to pay your monthly mortgage payments. If your income can’t be verified, it’s likely that your mortgage application will be rejected.

What Makes Income Verifiable?

So, what qualifies as verifiable income for mortgages? The key is simple: documentation. Lenders need hard proof that your income is consistent and reliable over time. Verifiable income is income that can be backed up by official records, stuff like pay stubs, tax returns, and bank statements.

If you’re using earned income (your job) or self-employment income, the documentation you provide will be fairly straightforward. You’ll need things like your most recent pay stubs, W-2 forms, and, for self-employed people, two years of tax returns and profit-and-loss statements.

But not all income types are so easy to verify. With the MortgageReadyProgram, we’ve been able to work with clients with various situations. Therefore, we are completely familiar with the process.

Income verification rules can vary slightly by lender, especially for mortgage readiness in Pennsylvania.

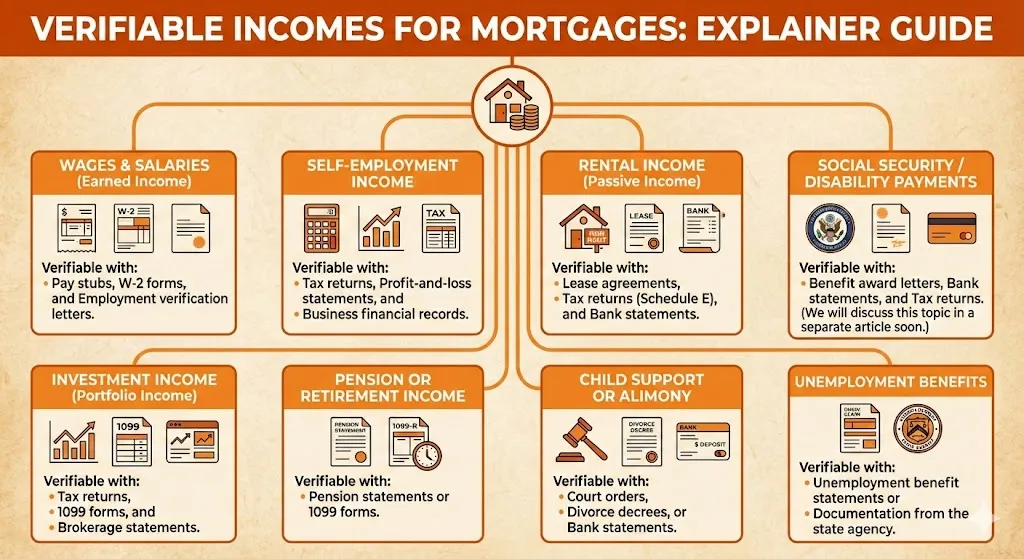

Verifiable Incomes for Mortgages:

- Wages and Salaries (Earned Income)

Verifiable with pay stubs, W-2 forms, and employment verification letters. - Self-Employment Income

Verifiable with tax returns, profit-and-loss statements, and business financial records. - Rental Income (Passive Income)

Verifiable with lease agreements, tax returns (Schedule E), and bank statements. - Social Security or Disability Payments

Verifiable with benefit award letters, bank statements, and tax returns.

We will discuss this topic in a separate article soon. - Investment Income (Portfolio Income)

Verifiable with tax returns, 1099 forms, and brokerage statements. - Pension or Retirement Income

Verifiable with pension statements or 1099 forms. - Child Support or Alimony

Verifiable with court orders, divorce decrees, or bank statements. - Unemployment Benefits

Verifiable with unemployment benefit statements or documentation from the state agency.

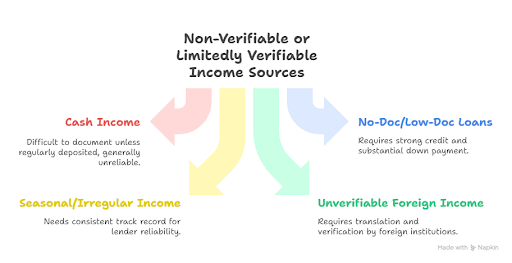

Non-Verifiable or Limitedly Verifiable Income Sources

Some income sources are not easily verifiable. If you receive income that doesn’t have clear documentation, it may not qualify for use in a mortgage application.

- Cash Income

Hard to document unless deposited regularly into your bank account. This is typically not considered reliable for mortgage qualification. - No-Doc and Low-Doc Loans

These types of loans require minimal or no income documentation, but they are often reserved for borrowers with strong credit histories and substantial down payments. - Seasonal or Irregular Income

Income from seasonal work or irregular sources may be harder for lenders to rely on unless there’s a proven, consistent track record over time. - Unverifiable Foreign Income

Foreign income that cannot be documented to meet U.S. standards may not be accepted by lenders unless translated and verified by foreign institutions.

Conclusion

Getting a mortgage isn’t just about picking a nice house and hoping the bank says “yes.” Lenders want proof you can actually pay them back, and that means verifiable income. Before you dive in, it’s worth knowing exactly what kinds of income count, so you don’t get blindsided halfway through and end up saying, “Wait… my side hustle selling cat sweaters doesn’t qualify?”

If this is your first time navigating income documentation, our first-time homebuyer readiness guide walks you through every step.

Also, if you are interested in knowing about other essential elements of mortgage approval, let us know in the comments below!

Ready to make your homeownership dream a reality? Sign up today!

0 Comments