Have you ever thought about how to be financially ready to start the homebuying process? Buying a home requires thoughtful preparation; you can’t simply dive into the process. You need to think and learn how to achieve financial readiness when preparing to buy a home.

If you are considering buying a home in the future, this article is written for you. Here you will learn:

- What it means to be financially ready to buy a home

- When you should start thinking about financial readiness,

- How to be financially prepared,

- What mistakes to avoid, and

- A quick financial checklist

Let’s get started!

Table of Contents

What Does Financial Readiness Mean?

First, let’s see what being financially ready to buy a home looks like. It refers to your overall financial stability and your ability to handle both the upfront and long-term costs of owning a home. It’s not just about having enough money for a down payment. It’s about:

- Having a stable income

- Maintaining good credit

- Saving for emergencies

- Managing debt responsibly

Being financially ready means you can buy a home with confidence and avoid being overwhelmed by unexpected costs. This is one of the important steps of preparing to buy a home as a first-time homebuyer.

When Should You Start Preparing to Buy a Home?

According to Coldwell Banker’s “2025 American Dream Report: Over half (51%) of Americans plan to buy a home in 2025. This shows many buyers are actively saving and planning now.

Ideally, you should start preparing 1–3 years before you plan to buy a home. Early preparation allows you time to save money and build proper financial habits to improve your credit score and manage your debts. Depending on your current situation, you may be ready right now to buy a house or need around 1 year to begin the process. So you need to know how your financial health is.

Assess Your Current Financial Health

Before taking any major steps, evaluate where you currently stand:

- Are you securely employed?

- Is your income stable?

- Do you have consistent savings habits?

- Are you living paycheck to paycheck?

- How is your credit score?

- How much debt do you pay each month?

This will give you an idea of your financial situation.

Early self-assessment is the first step toward making sure you’re financially ready to buy a home. Although these are basic questions, they will give you an idea of your financial situation.

A detailed assessment requires knowledge, tools, and experience. Sign up for the Mortgage Ready Program now, so you don’t have to worry.

Understand Your Credit Profile

Your credit score determines the type of mortgage you qualify for and the interest rate you’ll receive.

To strengthen your credit profile, make sure you:

- Check your credit score and credit report

- Dispute any errors

- Pay bills on time

- Keep credit utilization low

- Open new lines of credit only when guided by an expert, as doing so can sometimes improve your credit profile and score

Remember, a higher credit score can save you thousands over the life of a mortgage. MRP manages every part of this process on your behalf to ensure your credit profile is strengthened correctly and efficiently.

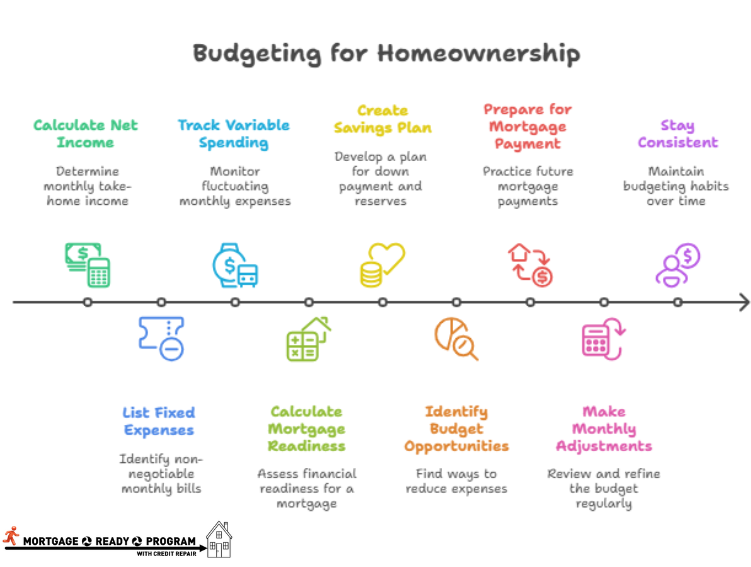

Start Budgeting

Budgeting is crucial for being financially ready to buy a home. Effective budgeting starts with asking yourself the following key questions:

- Can you afford the mortgage?

- Can you handle the payment increase (payment shock)?

- Do you have money left over after closing (reserves)?

A solid budget answers all three.

Budgeting isn’t about restricting yourself, it’s about:

- Showing lenders you’re responsible

- Preparing for your future mortgage payment

- Avoiding overdrafts and late payments

- Understanding where your money actually goes

- Building savings confidently

Most importantly, it gives you control, which reduces stress throughout the mortgage process.

Here we show you how to start budgeting step by step:

STEP 1: Calculate Your Monthly Net Income

This is the amount you take home after taxes, health insurance, and other payroll deductions.

Include ALL sources of income:

- W-2 job

- Second job

- Gig work (DoorDash, Uber, Instacart)

- Child support or alimony you receive (optional to disclose)

- Pension, Social Security, or disability income

- Consistent cash income (if deposit history can be documented)

Tip: If income changes month-to-month, use your average from the past 3–6 months.

Write down your total monthly take-home income. This number is your starting point.

STEP 2: List Your Fixed Monthly Expenses (The Non-Negotiables)

Fixed expenses are bills you must pay each month. These rarely change.

Examples:

- Rent

- Car payment

- Insurance (car, health, life)

- Cell phone

- Utilities

- Internet

- Childcare

- Minimum credit card payments

- Student loans

Add these up. These bills show lenders your current obligations (your debt-to-income ratio).

STEP 3: Track Your Variable Spending (Where Money Slips Away)

These are expenses that change month to month:

- Groceries

- Gas

- Eating out

- Coffee shops

- Shopping

- Personal care

- Entertainment

- Kids’ activities

- Miscellaneous spending

Most people underestimate this area.

To get a real number:

- Open your banking app.

- Look at the last 30 days.

- Total the categories honestly.

Your budget becomes accurate only when your variable spending is realistic, not optimistic.

STEP 4: Calculate Your “Mortgage Readiness Number”

Now do this:

Net Income – Total Monthly Expenses = Your Surplus (or deficit)

This number reveals:

- How much you can realistically save

- Whether you can handle a future mortgage payment

- Whether payment shock could be a problem

- How long will it take to build down payment & reserves

A healthy financial goal is to maintain a monthly surplus of $500–$1,000 and build a consistent pattern of savings in the months leading up to your mortgage application.

If your surplus is small or negative, don’t worry, budgeting helps fix that.

STEP 5: Create Your Savings Plan

A homebuyer must save for three financial buckets:

- Down Payment

- FHA: 3.5%

- Conventional: 3–5%

- VA/USDA: $0

- Closing Costs

Usually 2–5% of the purchase price.

- Reserves

Lenders like to see:

- 2–3 months of mortgage payments

- More reserves = stronger approval

STEP 6: Identify “Budget Opportunities”

Find out how you can cut your expenses. These small changes create big results:

- Cut non-essential subscriptions

(You’d be shocked how many people forget about their $9.99 and $14.99 monthly fees.)

- Reduce eating out

Not eliminate, just adjust.

- Use autopay to avoid late fees

A single missed payment can end your mortgage approval. ( We will discuss late payments in a separate article.)

- Build a separate savings account

Name it “Home Fund” so you don’t touch it.

Budgeting isn’t about cutting everything. It’s about making room for your homeownership goals.

STEP 7: Prepare for Your Future Mortgage Payment

To avoid payment shock, your future mortgage payment should feel comfortable, not scary.

Try this exercise:

Start practicing your future mortgage payment today.

If you currently pay $1,200 in rent and your future mortgage may be $1,700:

- Start transferring $500/month into savings

- Do this for 3–6 months

This proves you can handle the payment and build reserves at the same time.

Lenders love to see this.

STEP 8: Make Adjustments Monthly

Your first budget won’t be perfect; nobody’s is.

Aim to review your budget:

- Once a week (quick check-in)

- Once a month (full review)

Ask yourself:

- Did my planned spending match my actual spending?

- Did unexpected expenses come up?

- How much did I save?

- Am I closer to my homeownership goal?

The goal is progress, not perfection.

STEP 9: Stay Consistent (This Matters More Than Anything Else)

You do NOT need a perfect budget to buy a home.

You DO need:

- Consistency

- Stability

- On-time payments

- Strong savings habits

- Predictable financial patterns

Lenders look at your behavior over time, not one good month.

Remember, a budget is not a restriction; it’s your roadmap to homeownership.

Manage and Reduce Debt Before Applying

High levels of debt can lower your credit score and increase your DTI ratio and your mortgage approval chances.

To support being financially ready to buy a home, try to:

- Pay down high-interest debt first

- Avoid new credit inquiries

- Make consistent, on-time payments

Financial Mistakes to Avoid When Preparing for Homeownership

Common mistakes can slow down or even derail your progress toward homebuying. These include making large purchases before applying for a mortgage, changing jobs unexpectedly, taking on new debt, or ignoring inaccuracies on your credit report. Another frequent mistake is underestimating the cost of homeownership, such as maintenance, taxes, and utility expenses. Avoiding these pitfalls protects your financial stability and keeps your homebuying timeline on track.

Quick Financial Readiness Checklist

Before you begin house hunting, make sure you’ve checked off the essential steps:

- Your credit score is strong

- Your down payment is growing

- Your emergency fund is solid

- Your debt is manageable

- Your budget is clear

- Your income is stable and verifiable

- You have a plan for preapproval

Completing this checklist confirms you are financially ready for homebuying and sets you up for success.

Final Thoughts

Being financially ready for homeownership is a process that takes time, discipline, and thoughtful planning. But each step you take brings you closer to owning a home with confidence. By preparing early, strengthening your credit, saving strategically, and managing debt, you give yourself the best possible start. With the right preparation, your dream of homeownership becomes not just achievable but sustainable.

You do not have to go through this process alone. The Mortgage Ready Program is your lifesaver when it comes to homebuying. Sign up today!

0 Comments