Securing a home loan is a multi-step journey that often feels like a marathon. While obtaining a pre-approval is a significant first step that allows you to start house hunting, it is not the final word on your financing. The mortgage underwriting process is the “last big hurdle” before you can officially close on a home and pick up the keys.

Underwriting is the detailed verification stage where a lender performs an in-depth review of your financial background to determine your eligibility and the risk associated with lending you money. Because your mortgage is as unique as your financial situation, understanding the intricacies of this process is essential for every homebuyer. So let’s explore the mortgage underwriting process!

Table of Contents

What is Mortgage Underwriting?

Mortgage underwriting is a behind-the-scenes evaluation that takes place after you have submitted a full loan application. During this phase, your application moves from a loan processor to a mortgage underwriter, who serves as a financial and real estate investigator. The primary goal of the underwriter is to verify that your financial profile matches the lender’s specific qualification guidelines and loan criteria. They assess your stability and the overall risk of the loan to ensure you are equipped to repay the mortgage in full and on time. Ultimately, the underwriter is the professional who makes the final decision to approve, deny, or pend your loan application.

As you can see, the final decision on your loan is made during the mortgage underwriting process. That’s why you need to be ready before this milestone in your homebuying journey. Our Mortgage Readiness Guide helps make sure you don’t miss anything and that you’re fully prepared when it matters most, especially if you are a first-time homebuyer.

The Key Players in the Process

While the underwriter makes the final call, several individuals collaborate to move your loan toward the finish line:

- The Borrower: You are responsible for providing accurate documentation and responding to inquiries promptly.

- The Loan Officer: This individual assists with the initial application and coordinates with the underwriting team.

- The Loan Processor: This person gathers and organizes your documents, ensuring the file is complete before the underwriter begins their review.

- The Underwriter: An employee of the lender (or an outsourced firm) who analyzes risk and confirms the loan meets all internal and investor guidelines.

- The Appraiser: An impartial professional who determines the fair market value of the property to ensure the collateral is sufficient.

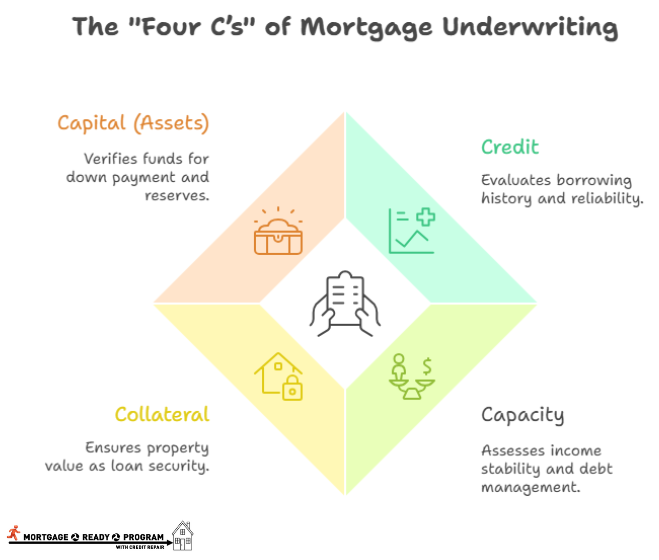

The “Four C’s” of Mortgage Underwriting

To determine creditworthiness and loan risk, underwriters focus on four main pillars, often referred to as the “Four C’s”:

1. Credit

Underwriters review your credit history and credit score to understand your past borrowing behavior and reliability. They look for patterns in how you have managed previous debts, such as car loans, student loans, and credit cards. A solid repayment history predicts your ability to make future mortgage payments on time. Be aware that many lenders check your credit twice: once at the start of the application and again right before closing to ensure nothing has significantly changed.

Our Credit Improvement Guide is a perfect starting point if you are looking for ways to improve your credit.

2. Capacity

This refers to your ability to repay the loan based on your income and current financial obligations. Underwriters evaluate your employment history, income stability, and debt-to-income (DTI) ratio. Lenders divide your total monthly debt payments (rent/mortgage, auto loans, student loans) by your gross monthly income. For example, if you earn $5,000 monthly and have $2,100 in combined debt, your DTI is 42%.

For more information about DTI, refer to this article: Debt-to-Income Ratio for Mortgages: A Comprehensive Guide

3. Collateral

The lender must ensure that the property being purchased serves as adequate security for the loan. This is verified through a property appraisal, which confirms the home’s fair market value. If a borrower defaults, the lender needs to be certain they can recover the unpaid balance by selling the property.

4. Assets (or Capital)

Underwriters examine your checking, savings, and investment accounts to verify you have the funds for a down payment and closing costs. They also look for cash reserves. This is the money left over after the purchase that ensures you can handle mortgage payments if unexpected expenses arise.

The Mortgage Underwriting Process Timeline

This is one of the questions almost every homebuyer asks. And the honest answer is: it depends. The mortgage underwriting timeline changes based on the lender’s workload, how complicated your finances are, and how fast you send the documents they ask for. So no, there’s no exact number. But here are some realistic estimates:

- Initial Review: Usually takes about three business days once your documents are received.

- Total Timeframe: The entire process, from application to closing, typically spans 30 to 60 days. However, Zillow Home Loans states that the mortgage underwriting process typically takes between 30 and 45 days to complete as part of the full mortgage approval timeline.

- Delays: Factors that can slow the process include missing signatures, large unexplained bank deposits, complex self-employment income, or issues discovered during the appraisal or title search.

The key here is patience. You’re buying a home that you and your family may live in for many years. That’s a big life milestone. Waiting a few extra weeks to get it right is worth it… right?

Essential Documentation Checklist

Underwriters require extensive documentation to verify the details provided in your application. Standard requirements include:

- Income Proof: Pay stubs from the last 30 days and W-2 or 1099 forms from the past two years.

- Tax Documentation: Federal tax returns for the past two years.

- Asset Statements: Bank and investment account statements, typically covering the last two months.

- Debt Details: Statements for outstanding long-term debts like student loans or car notes.

- Special Documents:

- Self-Employed Borrowers: May need profit-and-loss statements, balance sheets, and business tax returns.

- Gift Letters: If a family member provides funds for your down payment, you must provide a letter stating the money is a gift and does not need to be repaid.

- Letter of Explanation: You may be asked to clarify specific issues, such as a gap in employment, a late payment on your credit report, or a large, unusual deposit in your bank account.

Property Review: Appraisals and Title Searches

Underwriting involves more than just evaluating the borrower; it also requires a deep dive into the property itself.

The Appraisal

A professional appraiser inspects the home and compares it to “comps” (comparable properties recently sold in the area) to determine its value. If the appraisal comes in lower than the purchase price, the underwriter may suspend the application. In this case, you may need to renegotiate the price with the seller, pay the difference out of pocket, or walk away from the deal.

The Title Search

The lender works with a title company to ensure the property can be legally transferred to you. The search looks for liens, claims, unpaid taxes, or easements that could derail the loan. Once cleared, title insurance is typically required to protect against future legal claims to the property.

Decoding the Underwriting Decision

Once the underwriter completes their review, they will issue one of the following decisions:

1. Approved (Clear to Close): This is the ultimate goal. It means you have met all requirements, and your closing can be scheduled.

2. Approved with Conditions: This is a common outcome where the loan is likely to be approved, but you must first resolve minor issues, such as providing a missing signature, an updated pay stub, or proof of homeowners’ insurance.

3. Suspended (Pending): The underwriter needs more information before making a final decision, often because they cannot yet verify your income or employment.

4. Denied: The loan is rejected. This can happen due to high debt, a low credit score, or if the borrower took on new debt during the process. If denied, you can seek clarification from your loan officer and take steps to improve your credit or DTI before reapplying.

Common Challenges

Several hurdles can arise during the mortgage underwriting process, but most can be mitigated with preparation. Let’s go over some common challenges:

- Unstable Income: Frequent job changes or inconsistent income can raise red flags. Lenders prefer at least two years of consistent history in the same line of work.

- Incomplete Applications: Errors or missing information on your application can lead to incorrect risk assessments and significant delays.

- Credit Fluctuations: Taking on new debt (like a car loan) or increasing credit card balances while in underwriting can change your DTI and disqualify you from the loan.

- Unverifiable Assets: Large deposits that cannot be traced to a known source may be excluded from your qualifying assets.

Pro-Tips for a Smooth Underwriting Experience

To expedite your approval and avoid unnecessary stress, follow these guidelines:

- Be Responsive: Aim to return all requested documents within 48 hours to keep the timeline on track.

- Protect Your Credit: Do not apply for new credit lines, close existing accounts, or make large purchases that could decrease your assets until after you close.

- Maintain Transparency: Be honest about your finances from the start. Underwriters will uncover discrepancies, so it is better to provide a letter of explanation upfront for any potential issues.

- Keep Your Job Stable: Avoid changing jobs or your pay structure (e.g., moving from a salary to commission) during the process.

Conclusion

Think of the mortgage underwriting process like a high-security airport checkpoint. Pre-approval was your ticket and initial ID check that allowed you into the terminal. Underwriting, however, is the full-body scan and luggage inspection. The underwriter is the security officer making sure every “item” in your financial history is safe, accounted for, and meets the strict requirements before you are cleared to board your “flight” to homeownership.

If you want to walk into underwriting with confidence instead of stress, the Mortgage Ready Program is built for exactly that. Sign up and make sure nothing in your finances surprises the underwriter when it matters most.

0 Comments