Changing jobs before mortgage closing is one of those situations that feels exciting in real life but risky in lending reality. A better opportunity, higher pay, or a long-awaited career move can pop up right in the middle of your home search or even after you’re under contract. The problem? From a lender’s point of view, your job and income are the backbone of your mortgage approval.

While switching jobs before closing isn’t always a deal-breaker, it does add layers of scrutiny and can quickly complicate or even derail your loan. This guide breaks down the real risks, lender rules, and smart strategies you need to understand so a career move doesn’t cost you your home.

Table of Contents

Why Lenders Care About Your Job Status

From a lender’s perspective, a mortgage is a long-term financial bet, and job verification is one of the main ways they manage that risk. They want to see stability, consistency, and income they can reasonably expect to continue for years, not just months. When you change jobs, you break that established paper trail, and that’s when underwriters start paying closer attention.

If a job change happens after you’ve applied for a mortgage, the lender usually has to re-underwrite your loan using the details of the new position. That means rechecking income, employment terms, and long-term stability. At best, this causes delays and pushes your closing date. At worst, if the new role looks less stable, pays less, or relies heavily on commissions or bonuses, the lender can pull the approval altogether.

Therefore, you need to make sure you are completely mortgage-ready if you want to change your job.

The Two-Year Work History Rule

For a standard mortgage application, underwriters generally look for a consistent two-year work history. This doesn’t mean you must have been at the same company for two years, but they want to see steady income in the same or a related field. If you have been in the same industry or position for over two years, you typically face fewer hurdles. However, if you have been in your current role for less than two years, lenders will scrutinize several “compensating factors,” including:

-

Your specific qualifications and professional training.

-

The overall financial health of your new employer and industry.

-

The frequency of your job changes (to ensure you aren’t “job hopping”).

-

Any extended periods of unemployment or gaps in your resume.

-

Measurable increases in pay and responsibility over time.

Gaps in Employment

Lenders are sometimes lenient regarding gaps in employment if they were for valid personal reasons, such as caring for a family member or the birth of a child, provided you have now returned to a stable, full-time role. In these cases, a Letter of Explanation (LOE) is often required to bridge the gap for the underwriter, clearly outlining the reason for the gap and demonstrating your current stable employment.

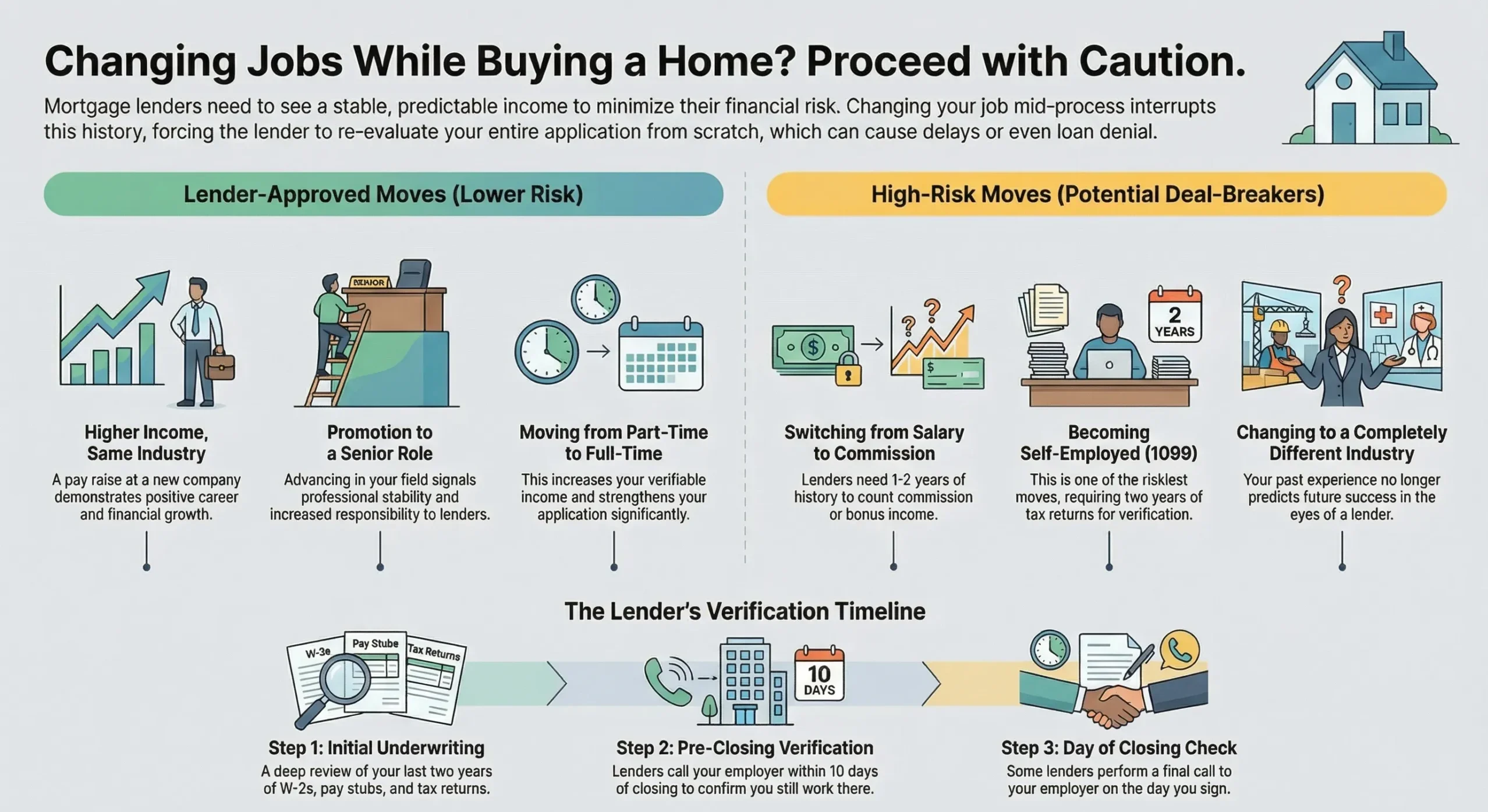

Acceptable vs. Unacceptable Job Changes

Not all career moves are viewed equally by mortgage underwriters. The nature of the switch determines whether it will be a minor hurdle or a deal-breaker.

Acceptable Changes (Positive Impact)

Changes that demonstrate career progression or increased stability are generally viewed favorably. These include:

-

Higher income within the same industry: Moving to a competitor for a 20% pay raise is seen as a strong positive.

-

Promotion to a more senior role: Advancing from a teacher to a principal, for example, signals professional growth and stability.

-

Moving from part-time to full-time: This increases your predictable income and significantly strengthens your application.

-

Documented Salary Jobs: Salaried positions with a clear offer letter and start date are the easiest for lenders to verify using pay stubs and W-2s.

Unacceptable Changes (High Risk)

Changes that make your income less predictable are red flags for loan officers. High-risk moves include:

-

Switching from salary to commission or bonuses: Lenders typically require a 12 to 24-month history of earning commission before they will count it toward your qualifying income.

-

Becoming an independent contractor (1099) or self-employed: This is one of the riskiest moves mid-process because it interrupts the paper trail of W-2 history. Most lenders require two years of tax returns to verify self-employment income.

-

Changing to a completely different industry: If you switch from pharmaceutical sales to managing a nightclub, your prior experience no longer predicts future success in the eyes of the lender.

-

Frequent lateral moves: Moving between similar-paying jobs without professional growth can make an applicant appear unstable or indecisive.

The Critical Verification Windows

Lenders do not just check your job at the beginning of the application; they verify it multiple times.

-

Initial Underwriting: A thorough review of your W-2s, pay stubs, and tax returns from the past two years.

-

Pre-Closing Verification: Typically, within 10 days of funding, lenders conduct a Verbal Verification of Employment (VVOE). They call your employer’s HR department to ensure you are still actively employed in the same position.

-

Day of Closing: Some lenders have been known to call the employer while the buyer is signing the final papers as a final fraud check.

Analogy: Changing jobs before mortgage closing is like trying to swap the engine of a car while you are driving it 70 mph down the highway; even if the new engine is better, the transition is incredibly dangerous for the vehicle’s stability.

Required Documentation for a Job Switch

If you must change jobs, you must be proactive and provide extensive physical proof to your lender immediately. You should be prepared to provide:

-

Signed Offer Letter: This must include your new title, salary, a hard start date (typically no later than 60 days after closing), and be on official company letterhead.

-

Most Recent Pay Stub: Lenders often want to see at least one pay stub from the new job before they will finalize the loan to confirm you have started and your pay matches the offer.

-

Verification of Employment (VOE) Form: A document completed by your new employer’s HR department confirming your role, pay structure, and probability of continued employment.

-

Transcripts or Licenses: For recent graduates or licensed professionals, college transcripts or professional licenses can sometimes support your qualifications for a new role in your field.

What to Do If You Lose Your Job Before Closing

Losing a job via layoff or discharge is a “red alert” situation. If this happens, you must contact your lender immediately. Hiding a job loss can be considered mortgage fraud because you sign documents at closing, swearing that your financial information hasn’t changed.

If you lose your job, you have a few options:

-

Pause the application: Ask the loan officer to pause rather than cancel to potentially save your earnest money and paid fees while you seek new employment.

-

Use a co-borrower’s income: If a spouse or partner earns enough to qualify for the loan alone, the lender may proceed without your income.

-

Find a new job quickly: If you secure a new role in the same industry with a similar or higher salary, the lender may still approve the loan after verifying the new employment, though delays are certain.

-

Explore alternative income sources: In some cases, lenders may consider documented side hustles, retirement/pension income, or alimony/child support if they are stable and can be verified.

Changing Jobs Before Mortgage Closing: The “Safe Zone”

Generally, once you have closed on the home and the loan has funded, you are in the clear to change jobs. After closing, the lender is primarily concerned with you making your regular monthly payments on time. Most lenders do not conduct employment verifications after the deal is recorded, unless they suspect fraud or the loan is being sold to a new servicer.

However, experts recommend waiting until you have made your first few mortgage payments comfortably to ensure your new career choice provides the financial stability needed to maintain the investment. If you default on the loan shortly after closing and the lender discovers you knew about a pending layoff or job change but didn’t disclose it, they could potentially take legal action for fraud.

Impact on Different Loan Types

Different mortgage programs have varying levels of flexibility regarding job changes:

-

Conventional Loans: Typically require two years of history, but can be flexible with an offer letter for same-industry moves, especially if it’s a higher salary.

-

FHA Loans: Known for being slightly more flexible toward those advancing in their line of work, they may even count commission income with less than a 12-month history if you stay with the same employer.

-

VA Loans: Consider active military duty as part of the two-year work history, and are often accommodating to military-related relocations and job changes.

-

USDA Loans: Have no strict minimum length of work history but require strong proof of stability and likelihood of continued employment in the current role.

Best Practices for Homebuyers

To ensure your home purchase remains on track, consider these expert tips:

-

Consult Professionals Early: Talk to your real estate agent and, most importantly, your loan officer before accepting a new job offer. They can give you a realistic assessment of the impact.

-

Close First, Switch Later: If possible, finalize the home purchase and closing before transitioning to a new company. Even a two-week delay can save your loan.

-

Maintain Your Credit: Do not open new lines of credit, make large purchases (like a new car), or close old credit cards during a job transition, as your Debt-to-Income (DTI) ratio and credit score are already under scrutiny.

-

Stay in the Same Industry: Lateral or upward moves in the same field are much easier to justify to underwriters than a total career pivot.

-

Be Proactive with HR: If you are moving to a large company, warn your new HR department that they will need to provide a quick verbal verification of employment (VVOE) to your lender.

Conclusion

Changing jobs before mortgage closing is not automatically a deal-breaker, but it is a high-risk move that demands precision, planning, and full transparency. Even a higher-paying “dream job” can disrupt your loan if the timing or documentation isn’t right. Lenders care less about the title and more about stability, continuity, and verifiable income.

If a job change is unavoidable, staying in the same industry, avoiding income gaps, and providing a clean, well-documented paper trail can make all the difference. Most importantly, keep your lender in the loop before anything changes. Surprises are what kill loans, and communication protects them.

When in doubt, pause and get expert guidance. A short delay in a career move is far easier to manage than losing a home at the closing table.

Ready to make sure you’re truly mortgage-ready?

Sign up with the Mortgage Ready Program (MRP) today and get clear, step-by-step guidance to protect your approval and move into homeownership with confidence.

Frequently Asked Questions (FAQ)

Can I start a new job during the mortgage process?

Yes, but it will require re-underwriting and could delay or jeopardize your loan. Full transparency with your lender is non-negotiable.

What if my new job pays significantly more?

A higher salary is positive, but lenders may still want to see one pay stub as proof. The increase can improve your Debt-to-Income (DTI) ratio, but the timing risk remains.

How long after closing can I change jobs?

Technically, immediately. The loan is funded. However, it’s financially prudent to ensure you are comfortable with the new role’s stability and can manage all new homeowner expenses.

Does a remote job change complicate things?

Not inherently, as long as it’s a W-2 salaried position in the same industry. The verification process is the same.

0 Comments