Mortgage options for people with bad credit in Pennsylvania are more realistic than most people think; even if you’ve gone through tough financial moments like a bankruptcy, foreclosure, or carrying high debt. A low credit score can slow things down, but it doesn’t automatically knock you out of the homeownership game in Pennsylvania.

If you’re dreaming of owning a home in PA but feel stuck because of your credit score, you’re definitely not alone. According to the Experian data in 2024, about 13.2% of Americans fall into the “poor credit” range. The good news? Getting a mortgage with bad credit in PA is absolutely possible if you know where to look and how to prepare. This guide walks you through your best options, whether you’re buying in Philly, Pittsburgh, or anywhere in between, and shows you the steps to get approved with confidence.

Let’s get started!

Table of Contents

What Does “Bad Credit” Mean for a Mortgage in PA?

Credit score ranges can look a little different depending on the lender and the scoring model being used. But when it comes to base FICO® Scores, lenders generally group scores into these ranges:

- Poor credit: 300 to 579

- Fair credit: 580 to 669

- Good credit: 670 to 739

- Very good credit: 740 to 799

- Exceptional credit: 800 to 850

While conventional loans typically require a 620-660+ score, numerous Pennsylvania mortgage lenders offer alternative paths for lower scores.

Top Mortgage Programs for People with Bad Credit in Pennsylvania

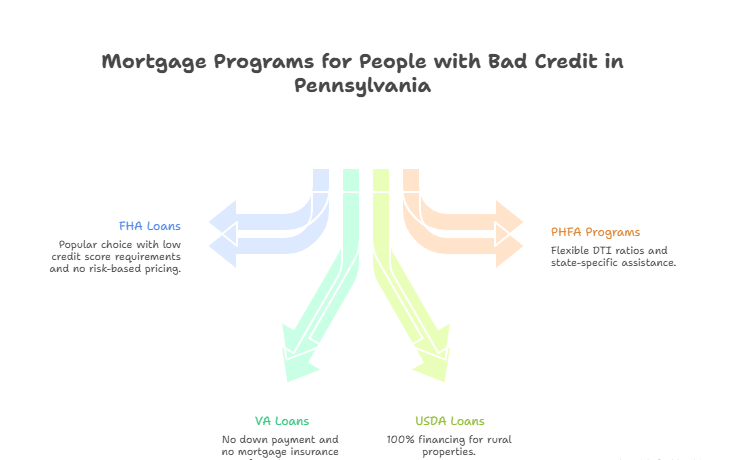

1. FHA Loans: The Most Popular Solution

Backed by the Federal Housing Administration, FHA loans are the go-to for borrowers with low scores.

-

Credit Requirements: Qualify with a score as low as 500 (10% down) or 580+ (just 3.5% down).

-

Key Benefit: No risk-based pricing. This means your interest rate won’t skyrocket based on your score alone, unlike with some conventional loans.

-

PA Perspective: Widely available through lenders across the state, making it a top choice in cities like Allentown, Scranton, and Erie.

2. VA Loans: $0 Down for Pennsylvania Veterans

With over 700,000 veterans in PA, this is a crucial program. VA loans are guaranteed by the Department of Veterans Affairs.

-

Credit Requirements: The VA itself sets no minimum score, but most Pennsylvania lenders look for a 580-620.

-

Key Benefits: No down payment and no monthly mortgage insurance, significantly lowering the barrier to entry.

-

PA Perspective: A powerful tool for eligible service members and spouses in military-friendly communities.

3. USDA Loans: 100% Financing in Rural PA

Targeting rural homebuyers, the USDA loan program offers no-down-payment options.

-

Credit Requirements: While flexible, most lenders prefer a 640+ score. You can apply with a lower credit score, but you may go through manual underwriting.

-

Key Benefit: 100% financing for eligible properties.

-

PA Perspective: Ideal for homes in eligible rural areas of counties like Monroe, Centre, Mifflin, and Lancaster.

4. Pennsylvania Housing Finance Agency (PHFA) Programs

Your local advantage. PHFA offers programs specifically for low-to-moderate-income residents.

-

Credit Flexibility: They often look beyond the score at job history, income stability, and down payment.

-

Key Benefit: May accept debt-to-income (DTI) ratios above 50%, offering flexibility for borrowers with existing debt.

-

PA Perspective: A must-explore state-specific resource with tailored assistance and counseling.

4 Key Strategies to Get Approved with Bad Credit in Pennsylvania

-

Make a Larger Down Payment: A down payment of 10%, 15%, or more significantly reduces lender risk and can offset a low credit score, especially with portfolio lenders.

-

Use a Co-Signer: A creditworthy co-signer (like a family member) can help you qualify for better terms. Remember, they share legal responsibility for the loan.

-

Request Manual Underwriting: A human underwriter can review your full story, including on-time rent or utility payments, not just an automated score.

-

Seek Help from Professionals: Yes, some mortgage programs allow lower credit scores—but you’ll need to make up for it with higher income, higher savings, or a bigger down payment. If you have time, improving your credit before applying is always the better move.

How to Quickly Improve Your Credit Score Before Applying

Don’t wait years. Take these actionable steps:

-

Dispute Credit Report Errors: Get your tri-merge report (Equifax, Experian, TransUnion) and dispute inaccuracies for a potential fast boost.

-

Negotiate “Pay-for-Delete”: Ask collection agencies to remove the negative entry in exchange for payment.

-

Lower Credit Utilization: Pay down revolving balances to below 30% (ideally 10%) of your credit limit.

-

Keep Old Accounts Open: Closing old accounts can shorten your credit history and lower your score.

If you want to improve your credit, start here.

The Bottom Line

Think of getting a mortgage with bad credit like hiking a steep trail in the Appalachians; it requires more preparation and the right guide, but the summit view of homeownership is worth it.

But remember, if you have the time, the smartest move is almost always to improve your credit before applying for a mortgage. And this isn’t a DIY situation, especially if you’re new to the process. Credit repair for a mortgage is precise and time-sensitive; one wrong move can set you back months. Working with professionals helps you fix the right things, in the right order, without hurting your chances.

Ready to start your path? Sign up Now!

0 Comments