If you’re self-employed and working toward homeownership, you’ve probably already learned that income proof for self-employed borrowers can feel a little different than it does for W-2 employees. Instead of just pay stubs and W-2s, lenders need to understand your business income, consistency, and expenses.

This comprehensive guide breaks down the exact documentation, calculation methods, and strategies you need to successfully prove your income and qualify for a home loan. Let’s get started!

Table of Contents

Who is a Self-Employed?

Now, who counts as “self-employed”? The IRS defines a business as an activity you do regularly and primarily for income or profit. This can include freelancers, contractors, small business owners, and more. If you just sell a few crafts as a hobby or do something once in a while for fun, that’s not a business. This distinction is important because the documents you should provide to the lender differ if you are not self-employed according to the IRS definition. For example, if you sell crafts as a hobby, you’d report that on Schedule 1, but if you are a freelancer, you’d use Schedule C to report your income.

Now, let’s find out the required income proof for self-employed borrowers!

Why Is It Harder for Self-Employed Borrowers to Get a Mortgage?

Lenders want income that is steady, easy to follow, and easy to verify. For W-2 employees, that’s fairly simple; an employer confirms the numbers. For self-employed borrowers, it’s a different story. You are the employer, which automatically puts you in a higher-risk category in the eyes of an underwriter.

Here’s where most people get tripped up: smart tax planning usually means writing off expenses to lower taxable income, but mortgage underwriting works in the opposite direction. Underwriters are trying to see the highest reliable income you can support, not the lowest number you reported to the IRS. Recognizing this disconnect early is critical and it’s often the difference between a smooth approval and a frustrating denial for mortgage applications.

The Primary Path: Full Documentation Loans

The most common and often most affordable route is the “Full Doc” loan. Full Doc Loans, or full documentation loans, are exactly what they sound like: mortgages that require a complete financial paper trail. Borrowers must fully verify their income, assets, and employment, leaving little room for guesswork. This usually means submitting tax returns, pay stubs, bank statements, and other financial documents so the lender can clearly see where your money comes from and how stable it is.

This requires thorough verification of your income and assets, typically needing at least two years of self-employment history to establish a reliable trend.

Essential Documentation Checklist for a Full Doc Loan:

Lenders typically require a minimum of two years of self-employment history and the corresponding documentation.

-

Personal Tax Returns: IRS Form 1040 for the past two years, including all schedules, especially:

-

Schedule C: For sole proprietors or single-member LLCs.

-

Schedule E: For rental property or partnership income.

-

Schedule K-1: For income from partnerships, S corporations, or estates.

-

-

Business Tax Returns (if applicable):

-

Form 1120: For C-Corporations.

-

Form 1120-S: For S-Corporations.

-

Form 1065: For Partnerships.

-

-

Year-to-Date Financials: A Profit & Loss (P&L) Statement and balance sheet prepared by you or your accountant, typically within the last 60-90 days.

-

Business Licenses & Proof of Operation: Documents showing your business is active and in good standing.

- Bank Statements: Complete statements for both personal and business bank accounts, typically for the past 2-12 months, to show consistent cash flow and sufficient funds for a down payment and reserves.

- 1099 Forms: Copies of any 1099 forms received for income from clients or contractors.

-

W-2 Forms (if applicable): If you pay yourself a salary from an S-Corporation.

How Lenders Calculate Your Qualifying Income: The Schedule Analysis Method (SAM)

Underwriters don’t just glance at your bottom-line number and move on. For self-employed borrowers, they use something called the Schedule Analysis Method (SAM) to rebuild their real cash flow from the ground up.

Here’s why this matters: self-employed income is spread across multiple IRS schedules, and the numbers on your tax return don’t always reflect the cash you actually have available each month. Deductions, write-offs, and one-time expenses can make your income look lower than it really is. SAM gives lenders a structured way to cut through that noise and figure out what income is stable, reasonable, and likely to continue.

Instead of starting with AGI and subtracting items, the SAM approach starts at zero and adds back only what can be clearly supported, qualified income, and specific add-backs allowed by the guidelines. This is usually done with tools like Fannie Mae Form 1084 or Freddie Mac Form 91. The goal is consistency, accuracy, and a defensible income number that can survive underwriting scrutiny.

Common “Add-Backs” for Self-Employed Borrowers:

-

Depreciation & Amortization: Wear and tear on assets or the write-off of startup costs.

-

Business Use of Home: The home office deduction.

-

One-Time, Non-Recurring Expenses: Unusual losses (e.g., from a natural disaster) or major equipment purchases.

-

Interest: Business interest expenses may be added back.

Note: Lenders will differentiate between recurring and non-recurring items. A one-time windfall (like an asset sale) won’t be counted, while a one-time major expense may be added back.

Remember, the Schedule Analysis Method (SAM) doesn’t exist to inflate your income or push the numbers higher. It can also work the other way:

-

If income is declining year over year, SAM may average it down.

-

If expenses look inconsistent or unsupported, they won’t be added back.

-

One-time spikes or aggressive write-offs can raise red flags instead of helping.

SAM makes income more accurate, not automatically higher. When your numbers are clean and well-documented, it often works in your favor. When they’re not, it can reduce what qualifies. That’s why self-employed borrowers need to plan before applying, not just file taxes and hope for the best.

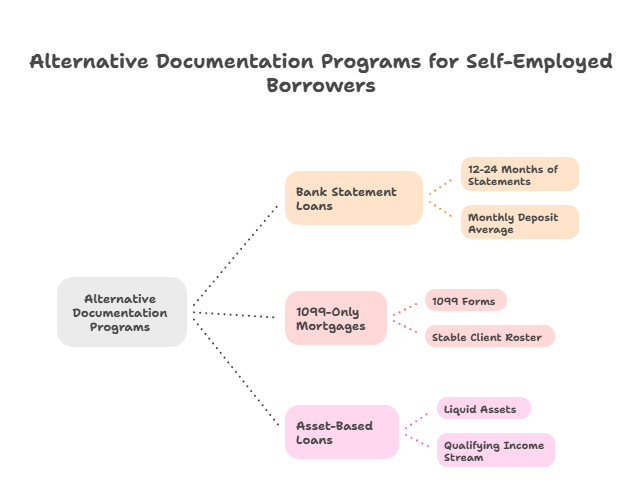

Alternative Documentation Programs for Self-Employed Borrowers

If significant tax write-offs depress your taxable income, these alternative loan programs can be a solution, though sometimes at a slightly higher interest rate.

1. Bank Statement Loans

-

How it Works: Lenders analyze 12-24 months of consecutive personal or business bank statements instead of tax returns.

-

Income Calculation: They average your monthly deposits. For personal statements, often 100% of deposits are counted as income. For business statements, lenders may apply an expense factor (e.g., 50%) to the deposits to estimate net income.

-

Best For: Borrowers with strong cash flow but high deductions (e.g., those with large depreciation expenses).

2. 1099-Only Mortgages

-

How it Works: Designed for independent contractors and gig workers, this loan uses your 1099 forms from clients over the past 1-2 years as primary income verification, alongside bank statements.

-

Best For: Freelancers with a stable roster of clients but less than two years of full tax returns.

3. Asset-Based or Asset Depletion Loans

-

How it Works: For high-net-worth individuals, lenders can create a “qualifying income” stream from your liquid assets (stocks, bonds, cash). The total asset value is divided by a term (e.g., 360 months) to create a monthly income figure.

-

Best For: Borrowers with substantial assets but lower documented income.

5 Key Strategies to Strengthen Your Mortgage Application

-

Optimize Your Credit Profile: Aim for a FICO score of 720 or higher. Excellent credit can offset the perceived risk of variable self-employed income and secure the best rates.

-

Lower Your Debt-to-Income (DTI) Ratio: Pay down debts before applying. While 43% DTI is often the max, aiming for 36% or lower significantly improves your approval odds and terms.

-

Prepare a Substantial Down Payment: 20-25% down is ideal. It reduces the lender’s risk, may eliminate the need for Private Mortgage Insurance (PMI), and demonstrates strong financial management.

-

Separate & Organize Your Finances: Maintain dedicated business and personal bank/credit accounts. Clean, distinct records simplify the underwriting process and present a professional image.

-

Work with a Specialized Mortgage Broker: Seek out lenders or brokers with proven experience in self-employed mortgages. They can match you with the right loan program and expertly guide your application.

- Make sure you are mortgage-ready: As a self-employed borrower, especially if you are a first-time homebuyer, you need to plan ahead and make sure you are mortgage-ready before you begin the process

Analogy: The Self-Employed Mortgage Application

Income proof for self-employed borrowers is like auditioning for a lead role without a script. A W-2 employee has a predefined script (their pay stub) that tells the lender exactly what to expect each month. You, however, must provide the director’s portfolio: past performances (tax returns), current rehearsal footage (P&L statements), and proof of your dedicated craft (business licenses) to convince them you can deliver a stellar, consistent performance for the entire run of the loan.

Next Steps: Prepare for Success

The real key to getting a mortgage when you’re self-employed is preparation and clean documentation. Ideally, you should start at least 12 months before you plan to apply. That means organizing your financial records, talking to a mortgage professional early, and, if needed, looping in a tax advisor to balance smart tax strategies with strong loan qualification.

If you’re not sure whether you’re truly ready to start the homebuying journey, don’t guess. Sign up today. The MortgageReady Program is built to walk you through the process step by step and make sure you’re positioned to qualify with confidence.

Frequently Asked Questions

How far back do lenders look at my self-employed income?

Most full doc loans require two full years of tax returns. Some alternative programs may only need 12-24 months of bank statements.

Can I get a mortgage with only one year of self-employment?

It’s very challenging but not impossible. You’d likely need exceptional credit, a large down payment, and proof of a related prior career (e.g., a CPA opening their own firm). Alternative documentation loans may be your best path.

Should I stop taking tax deductions to qualify for a mortgage?

Do not make drastic tax changes without consulting both your CPA and a mortgage advisor. The goal is to find a balance between smart tax planning and loan qualification. Sometimes, slightly higher taxable income in the two years leading up to a home purchase can be a strategic trade-off.

What is the single most important document for a self-employed mortgage?

Your Schedule C (for most freelancers/sole proprietors) or your corporate tax returns plus K-1s are the foundational documents. Your Year-to-Date P&L is crucial for showing current, ongoing health.

0 Comments