Opening credit before closing is a risky move that can cost you the deal right at the finish line. The time between your offer getting accepted and the day you sign is the financial quiet period. Your job is simple: keep everything exactly the same. From the moment you apply until the loan is funded, you’re under a microscope. Even a small thing, like applying for a store credit card or triggering a new inquiry, can force the lender to re-check your file. That can mean delays, or worse, a denial.

So let’s break down why opening credit before closing is one of the biggest mistakes you can make and how to protect your loan until you have the keys in hand.

Table of Contents

Why Lenders Perform a Final Credit Check Before Closing

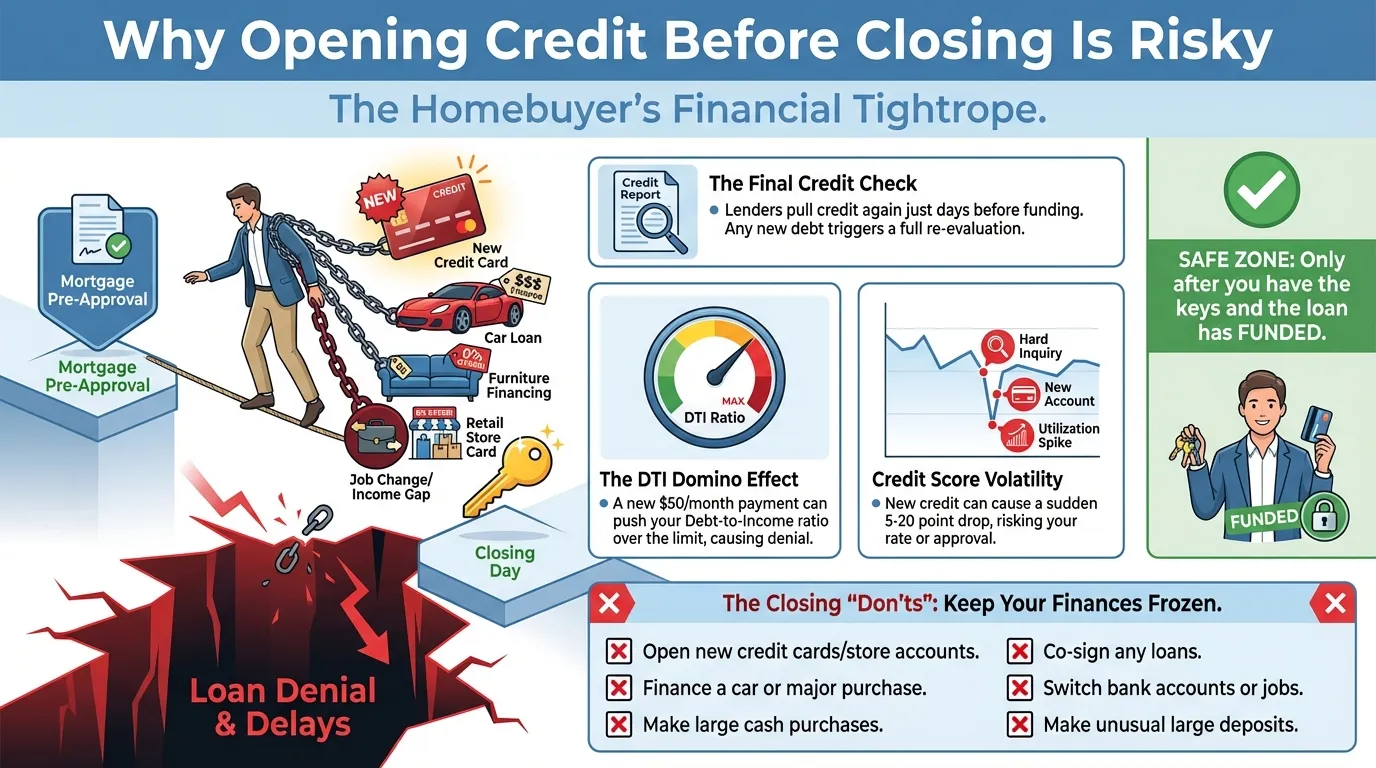

A common and costly misconception is that a mortgage pre-approval is a final guarantee. Many homebuyers believe that once they receive a “clear to close,” the hard part is over. In reality, the underwriting process is dynamic. Almost all lenders perform a “soft” or “hard” credit pull shortly before the scheduled closing date, sometimes just 24 hours in advance. This final verification serves one critical purpose: to confirm that your financial risk profile is identical to what was originally approved.

Lenders are fundamentally risk-averse. When they issue a loan, they model your ability to repay based on a specific set of data: your credit score, your debt-to-income ratio, and your assets. Opening credit before closing introduces a new, unmodeled variable: a new debt obligation. This signals increased risk, prompting the lender to halt and reassess. They must now answer a new question: “Can the borrower still afford the mortgage payment with this added monthly burden?”

The Domino Effect on Your Debt-to-Income (DTI) Ratio

The most direct and damaging impact of new credit is on your debt-to-income (DTI) ratio, the key metric lenders use to gauge affordability. There are two components:

-

Front-end DTI: This is your future monthly housing payment (principal, interest, taxes, and insurance) divided by your gross monthly income.

-

Back-end DTI: This is the sum of all your monthly debt payments (housing, auto loans, student loans, credit card minimums, etc.) divided by your gross monthly income.

Lenders typically have strict maximums for the back-end DTI, often capping it at 43% to 50%, depending on the loan program. If you were approved at a 48% DTI, you have virtually no wiggle room. Opening credit before closing, even for a “small” monthly payment of $50 on a furniture store card, can push your ratio to 49% or 50%. This technical breach of the underwriting guidelines can be grounds for an immediate loan denial, forcing you to either scramble to pay off the new debt or lose the house.

Credit Score Volatility: The Silent Killer

Your credit score is not a static number; it fluctuates based on recent activity. Introducing new credit during the mortgage process can cause a sudden and significant drop through several mechanisms:

-

The Hard Inquiry Impact: Each credit application triggers a “hard pull,” which can lower your score by 5-10 points. While one inquiry might be minor, multiple inquiries for new credit cards or auto loans are a major red flag.

-

Reduction in Average Credit Age: Your average account age contributes to 15% of your FICO score. Adding a brand-new account lowers this average, potentially shaving points off your score.

-

Increased Credit Utilization: If you immediately use the new credit line, you increase your overall credit utilization ratio (balances divided by limits). High utilization, especially on a new account, can cause a sharp score decrease.

For borrowers on the threshold between credit score tiers (e.g., 679 vs. 680), a drop of just a few points can mean the difference between qualifying and not qualifying, or result in a significantly higher interest rate, costing tens of thousands over the loan’s life.

The Siren Song of “Limited Time” Offers

Retailers are adept at targeting new homeowners. As closing approaches, you may be bombarded with enticing offers: “15% off your purchase today!” or “0% financing for 24 months!” These promotions are designed to capitalize on your excitement and imminent need for new belongings.

Resist them absolutely. Opening credit before closing for a “limited time” deal is the leading cause of preventable closing delays. The lender will discover this new account and must now:

-

Obtain account statements (which may not even exist yet).

-

Re-calculate your DTI ratio.

-

Possibly requires a letter of explanation.

-

Re-run your credit and potentially re-underwrite the entire loan.

Beyond Credit Cards: The Comprehensive Financial “Don’ts”

While opening credit before closing is a cardinal sin, other financial moves can be equally destructive. To ensure a smooth closing, adhere to this broader list of prohibitions:

-

Do Not Make Large Cash Purchases: Buying a car, boat, or expensive electronics, even with cash, depletes the assets you may need to prove you have sufficient reserves for closing costs and emergencies.

-

Do Not Change Jobs or Income Structure: Moving to a new company or transitioning from salary to commission-based pay introduces uncertainty. Lenders crave stability and verified income.

-

Do Not Move Money Unnecessarily: Large, non-payroll deposits into your accounts will need to be sourced and documented. Shuffling money between accounts or opening new ones creates a paper trail that must be meticulously explained.

-

Do Not Co-Sign Loans: Co-signing for someone else’s loan makes you 100% responsible for that debt in the eyes of your mortgage lender, drastically inflating your DTI ratio.

-

Do Not Miss Payments or Max Out Cards: Even your existing credit management is crucial. A late payment reported during this period can be catastrophic.

The Homebuyer’s “Ten Commandments” of Closing

This is the quiet period, the stretch between approval and closing where discipline matters more than excitement. If you want your loan to make it to the finish line, treat these rules as non-negotiable. You must not:

-

Change jobs, become self-employed, or quit your job.

-

Buy, lease, or finance an automobile.

-

Use credit cards excessively or let payments become late.

-

Spend the money earmarked for closing costs.

-

Omit debts or liabilities from your loan application.

-

Buy furniture, appliances, or other big-ticket items on a payment plan.

-

Originate any inquiries into your credit.

-

Make large, undocumented deposits into your bank accounts.

-

Switch bank accounts.

-

Co-sign a loan for anyone.

When Is It Finally Safe to Use Credit?

The absolute safest timeline is to wait until after the loan has fully funded and you have officially taken possession of the home. Note that there is a legal distinction between “closing” (signing the documents) and “funding” (the lender disbursing the money to the seller). In some cases, a lender may run a final check on the morning of funding. Therefore, your celebration shopping spree should only begin once you have the keys firmly in hand and the sale is recorded with the county.

Conclusion

Opening credit before closing is one of those mistakes that feels small but carries massive consequences. At this stage, your loan is built on trust and consistency. Any new credit, no matter how minor it seems, can crack that trust and force lenders to take a second, harder look at your file. And sometimes, that second look is all it takes to derail the deal.

The smartest move during this window is financial stillness. No new accounts. No new debt. No surprises. Think of your finances as frozen in time from application to funding. A few weeks of discipline protect the biggest purchase you’ll likely ever make.

If you want to avoid last-minute mistakes and know exactly how to prepare (and what not to touch), start with our Mortgage Readiness Guide. It walks you through every stage so nothing catches you off guard:

Sign up for MRP today and protect your path to homeownership.

0 Comments