Your credit score is the master key to homeownership; we all know that. A 740+ score opens the door to the best mortgage rates, but the good news is that many loan programs still work with lower scores. The minimum score depends on the loan type, but no matter which path you take, if you’re thinking about repairing your credit to buy a home, there’s one important question you need to ask: How long does credit repair take for a mortgage approval?

The answer depends on where you’re starting and what steps you take. Credit repair timelines can look very different from one person to another. In this guide, we break it all down with clear, realistic timelines so you know exactly what to expect. Let’s get things moving.

Table of Contents

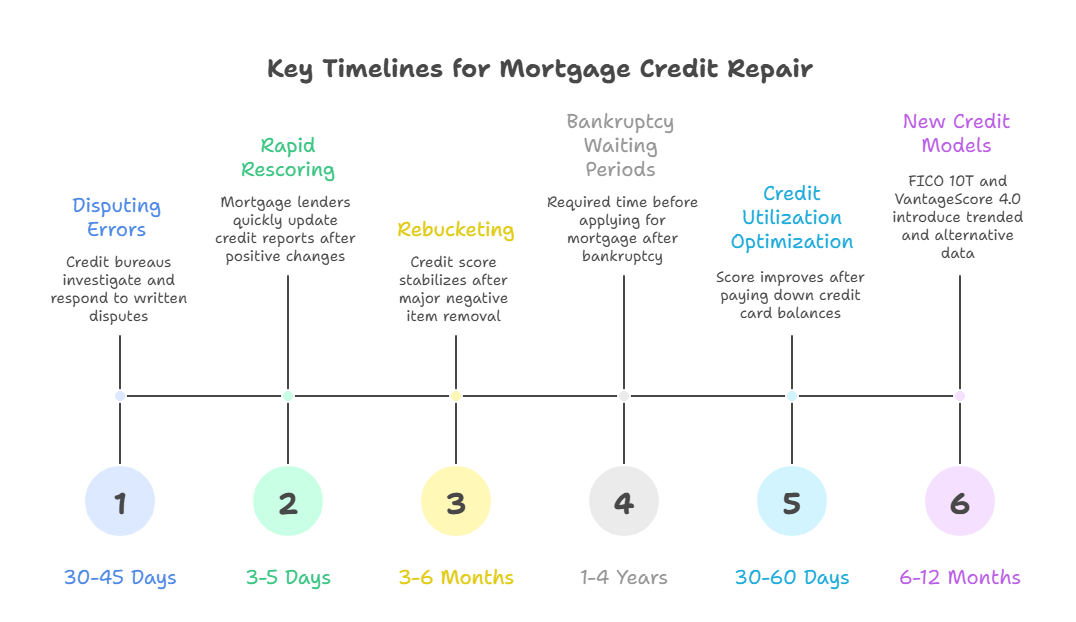

The 6 Key Timelines for Mortgage Credit Repair

1. Disputing Errors: 30-45 Days

Fixing inaccurate information is a critical part of the credit repair process. If you find an error on your credit report, the first step is to dispute it with the credit bureau reporting it: Experian, Equifax, or TransUnion. Do this in writing and clearly explain what’s wrong and why. Always include copies of any documents that support your claim. The clearer you are, the faster things usually move. Under the Fair Credit Reporting Act (FCRA):

-

30-day investigation is standard after filing a dispute.

-

45-day window if you provide extra info during the 30-day window or if you filed after your free annual report.

-

5 business days for bureaus to deliver results post-investigation.

Critical Insight: Beware of “account suppression.” If a creditor doesn’t respond within 30 days, the item may be removed temporarily but could reappear in 60–90 days if the creditor later reports it. Always follow up!

2. Rapid Rescoring: Three to Five Days

Rapid credit rescoring is a fast-track process to update your credit report after a recent positive change. In many cases, the results show up within three to five days. Normally, updates like paying down a credit card or fixing a reporting error can take 30 to 60 days to hit your credit report. Rapid rescore skips that waiting period and pushes the new information to Experian, Equifax, and TransUnion much faster. If you’re already in the mortgage process and need quick score updates, consider:

-

Exclusive access: Only mortgage lenders/brokers can initiate this.

-

Cost: $25–$50 per corrected item (Paid by the lender).

-

Use case: Ideal for updating paid-off balances or correcting errors when you’re days from closing.

3. The “Rebucketing” Phenomenon: 3–6 Months

Rebucketing is one of the most misunderstood parts of credit repair. When a major negative item (like a collection) is removed from your credit report, your score might temporarily drop. This happens because the scoring model no longer places you in the same comparison group. The system “rebuckets” you into a different category, comparing your report against a new set of similar profiles. This change in comparison can cause an initial, often temporary, drop in your score because the historical data used for evaluation has fundamentally changed.

-

Why? You’re moved from a “high-risk” scoring group to a “lower-risk” group, where your credit history may initially compare poorly.

-

Recovery: Within 3–6 months, your score can jump 60–100+ points as your profile stabilizes in the new bucket.

-

Analogy: You go from being the best player on a minor-league team (lower credit group) to a rookie in the majors (higher group). It takes time to establish your standing.

4. Bankruptcy Waiting Periods: 1–4 Years

If you’ve had bankruptcy or a disclosure, you have to wait a specific time to apply again. The waiting period you’ll face depends on the type of bankruptcy and the loan program you plan to use.

A. Bankruptcy Waiting Periods

| Loan Type | Chapter 7 Bankruptcy | Chapter 13 Bankruptcy |

| FHA Loan | Usually 2 years from the discharge date. | You may qualify with 12 months of on-time payments into your plan, plus court approval. |

| Fannie Mae | Typically 4 years from discharge date. | Often 2 years from discharge date if discharged, or 4 years if dismissed. |

| VA Loan | Often 2 years from discharge date. | May qualify after 12 months of plan payments from filing date with court/trustee approval. |

Important: The “clock” usually starts at the discharge date, not the filing date

Some shorter waiting periods are possible if you can document “extenuating circumstances” (job loss, medical emergencies, etc.).

B. Foreclosure, Short Sale, Deed-in-Lieu Waiting Periods

| Loan Type | Foreclosure Waiting Period | Short Sale / Deed-in-Lieu Waiting Period |

| FHA | About 3 years from the date the foreclosure was completed. | Also ~3 years, though if you were current on payments before sale, the wait may be less. |

| Fanni Mae | Normally 7 years, but may be reduced to 3–4 years with extenuating circumstances. | Often 4 years from short sale date if no foreclosure. |

| VA | Often as short as 2 years after foreclosure for qualified borrowers. | Often 2 years from the completion date |

Key point: Staying current on your housing payments, repairing credit, stabilizing finances, and documenting hardship help shorten the timeline.

5. Credit Utilization Optimization: 30–60 Days

Credit utilization simply means how much of your available credit you’re using. If your credit card limit is $10,000 and you’re carrying a $5,000 balance, your utilization is 50%. Lenders don’t like that. This is the fastest thing you can fix on your own, and it has a big impact. Credit utilization makes up about 30% of your FICO score, which is huge.

-

Immediate step: Pay down balances to below 30% of your limit.

-

Optimal: Aim for 1–10% for the best scoring.

-

Timeline: Once reported (usually next billing cycle), score impacts can be seen in under 60 days.

6. New 2026 Credit Models: A Game-Changer

Starting in 2026, new credit scoring models, FICO 10T and VantageScore 4.0, will play a much bigger role in mortgage lending. And honestly, this is good news for a lot of buyers. These changes include:

-

Trended Data: Lenders will review 24 months of payment behavior, not just current balances.

-

Alternative Data: Another big change is alternative data. Rent payments, utility bills, and even phone bills can now count toward your credit profile, if they’re reported. For people who don’t use credit cards much, this is huge.

-

Impact: Under older systems, people with limited credit history often had to wait a long time to qualify. With these new models, consistent rent and bill payments can help prove creditworthiness much faster. In some cases, this could shave months off the timeline to mortgage readiness.

How Long Does Credit Repair Take for a Mortgage Approval?

Critical Warnings for Homebuyers

-

The Collection Trap: Paying an old collection can lower your score by updating the “Date of Last Activity,” making old debt appear recent.

-

Never Close Old Accounts: Closing cards shortens your credit history and reduces available credit, potentially dropping scores 40+ points.

-

Avoid Hard Inquiries: Each credit application can lower your score by ~5 points and remains for 2 years.

Your Action Plan: Timeline Summary

| Scenario | Typical Timeline | Priority Level |

|---|---|---|

| Disputing errors | 30–45 days | High |

| Rapid rescoring (near closing) | 3–5 days | Urgent |

| Recovering from rebucketing | 3–6 months | Medium |

| Post-bankruptcy waiting period | 1–4 years | Planning |

| Optimizing credit utilization | 30–60 days | High |

| Building credit via rent (2026+) | 6–12 months | Future-ready |

Bottom Line

Credit repair for a mortgage can take anywhere from 30 days to 4+ years. It all depends on your credit history. And if you don’t fully understand the process, one small mistake can easily slow things down even more.

That’s why we don’t recommend trying to handle credit repair on your own. Getting expert help can save you time, stress, and costly delays. At MortgageReadyProgram.com, we guide you from start to finish, helping you qualify for a mortgage and actually buy your home.

Don’t guess your way through it. Start today and Sign Up.

Frequently Asked Questions

Can I repair my credit in 30 days for a mortgage?

Yes, if the issue is reporting errors or high utilization. Structural issues (bankruptcy, late payments) take longer.

Should I pay off collections before applying?

Consult a credit specialist. Sometimes, pay-for-delete agreements help, but often paid collections remain on reports for 7 years.

Do credit repair companies speed up the process?

They can streamline disputes, but no one can legally remove accurate negative items faster than the FCRA allows.

How long should I wait after credit repair to apply?

Monitor your score for 60–90 days after major changes to ensure stability before a mortgage application.

0 Comments